Key Takeaways :

- The CLARITY Act is emerging as the cornerstone of U.S. digital asset regulation, with bipartisan momentum but rising political friction.

- The definition and scope of DeFi remain the single largest obstacle, potentially delaying passage despite broad agreement elsewhere.

- Stablecoin reward mechanisms appear closer to compromise, signaling incremental progress rather than outright gridlock.

- Tokenized equities may move forward through hybrid regulatory models, pilot programs, or stricter securities classification.

- For investors, builders, and institutions, regulatory clarity could unlock new crypto assets, yield opportunities, and real-world blockchain adoption.

1. The CLARITY Act: A Long-Awaited Regulatory Backbone

The U.S. digital asset market has long suffered from regulatory ambiguity. While innovation surged across cryptocurrencies, DeFi protocols, stablecoins, and tokenized assets, the legal framework lagged behind, leaving market participants exposed to enforcement-driven policymaking. Against this backdrop, the CLARITY Act—short for the Crypto Legal Accountability, Responsibility, and Transparency for Innovation Act—has emerged as a central legislative effort to define the rules of the game.

According to a recent analysis by Citigroup, the CLARITY Act represents the most credible attempt yet to establish digital assets as a legitimate, regulated financial sector in the United States. Lawmakers are reportedly targeting spring 2026 for passage, reflecting growing bipartisan recognition that regulatory uncertainty is driving innovation offshore.

However, Citi cautions that while momentum exists, the path forward is far from smooth. Political disagreements—particularly around decentralized finance—could slow deliberations or lead to a watered-down outcome.

2. Why DeFi Is the Core Point of Contention

Decentralized finance is both the most innovative and the most controversial segment of the crypto ecosystem. By removing centralized intermediaries, DeFi protocols enable lending, trading, derivatives, and asset management through smart contracts. Yet this very decentralization challenges traditional regulatory assumptions.

At the heart of the CLARITY debate lies a deceptively simple question: What exactly qualifies as DeFi?

Some lawmakers argue that any protocol enabling financial activity should be subject to similar oversight as banks or broker-dealers, regardless of decentralization claims. Others counter that imposing centralized compliance obligations on decentralized systems is technically infeasible and philosophically contradictory.

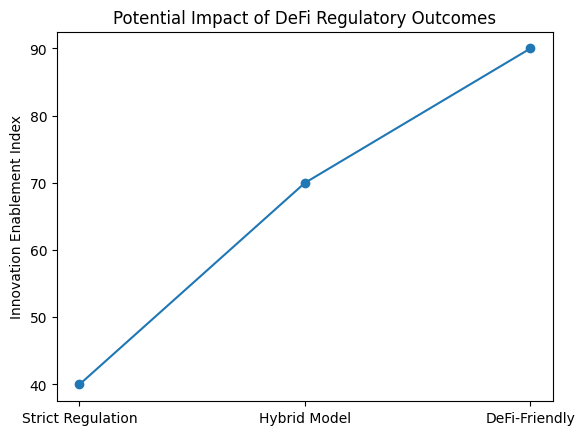

Citi identifies this definitional struggle as the single largest risk to the bill’s timeline. If Congress cannot agree on whether developers, DAO participants, front-end operators, or liquidity providers bear regulatory responsibility, negotiations could stall entirely.

For builders and investors, this uncertainty matters. A narrow DeFi definition could push innovation toward permissioned or semi-centralized models, while a broader exemption might accelerate open, global protocols—but at the cost of regulatory backlash later.

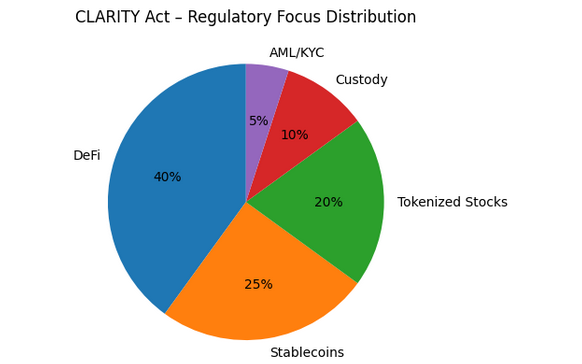

3. Stablecoin Rewards: A Path Toward Pragmatic Compromise

In contrast to DeFi, stablecoins appear to be an area where compromise is more achievable. The CLARITY Act addresses not only issuance and reserves, but also stablecoin rewards—such as yield, cashback, or incentive programs paid to users.

Historically, regulators have been wary of stablecoin yields, viewing them as potential unregistered securities. However, market realities have softened this stance. Dollar-pegged stablecoins now underpin global crypto liquidity, cross-border payments, and on-chain settlement, often offering modest rewards to encourage adoption.

Citi suggests lawmakers may accept a framework that permits stablecoin rewards under clear disclosure and reserve requirements. This would align with parallel regulatory efforts in Europe and parts of Asia, where stablecoins are treated as payment instruments rather than speculative assets.

For financial institutions and fintech operators, this represents a tangible opportunity. Regulated stablecoin reward structures could enable compliant yield products, treasury management tools, and cross-border remittance services—bridging traditional finance and blockchain rails.

4. Tokenized Stocks: Between Innovation and Securities Law

Another critical area addressed by the CLARITY Act is tokenized equities—blockchain-based representations of publicly traded stocks. While tokenization promises 24/7 trading, fractional ownership, and instant settlement, it also collides directly with existing securities law.

Citi’s analysis points to several possible regulatory pathways. One is a hybrid framework, where tokenized stocks are recognized as securities but traded on blockchain-native platforms under modified rules. Another is the use of pilot programs or regulatory sandboxes, allowing controlled experimentation without full-scale legalization.

A stricter alternative would classify tokenized stocks squarely as securities, subjecting them to the same disclosure, custody, and reporting requirements as traditional equities. While this approach limits innovation, it offers legal certainty and institutional comfort.

For crypto-native investors, tokenized equities may not be the next speculative frontier—but for asset managers, exchanges, and infrastructure providers, they represent a convergence of capital markets and blockchain technology with long-term revenue potential.

5. Market Implications for Investors and Builders

Regulatory clarity does not merely reduce risk—it reshapes opportunity. If the CLARITY Act passes in a meaningful form, the U.S. could reassert itself as a global hub for compliant digital asset innovation.

For investors seeking new crypto assets, clearer rules could legitimize entire categories previously deemed too risky, including regulated DeFi protocols, yield-bearing stablecoins, and tokenized real-world assets. For entrepreneurs, it could unlock institutional partnerships, banking access, and scalable business models.

However, Citi’s warning remains salient: delays or compromises around DeFi could fragment the market. Builders may design around regulatory uncertainty, favoring jurisdictions with clearer frameworks, while U.S.-based firms adopt conservative, compliance-heavy architectures.

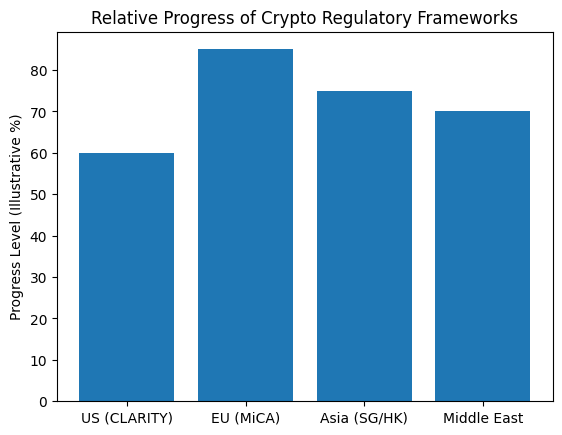

6. Global Context: The Cost of Delay

While U.S. lawmakers debate, other regions are moving forward. The European Union’s MiCA framework, parts of the Middle East, and several Asian financial hubs are actively courting crypto businesses with clearer rules. Each month of delay risks capital flight, talent migration, and lost technological leadership.

Citi frames the CLARITY Act not just as a domestic issue, but as a strategic imperative. The question is no longer whether crypto will integrate into the global financial system, but where that integration will be centered.

Conclusion: Clarity Is Coming—But at a Price

The CLARITY Act represents a pivotal moment for U.S. crypto regulation. Its progress signals growing acceptance of digital assets as a permanent fixture of modern finance. Yet its fate hinges on resolving deep disagreements over decentralization, responsibility, and control.

For readers seeking the next crypto opportunity, the message is nuanced. Regulatory clarity will unlock new assets, yields, and use cases—but only for those who understand the legal architecture shaping them. Whether DeFi emerges as a regulated pillar or a constrained niche will define the next chapter of blockchain innovation in America.