Key Takeaways :

- Crypto markets are transitioning from retail-driven momentum trading to institution-led strategic allocation.

- Approval of spot Bitcoin ETFs in the U.S. marked the beginning of a “second phase” of institutional adoption.

- Morgan Stanley’s ETF registrations signal a shift from distribution to product creation by major banks.

- Macro capital rotation away from mega-cap tech stocks may structurally benefit crypto assets in 2026.

- Digital Asset Treasury (DAT) firms avoided forced selling risk after MSCI’s latest decision.

- Bitcoin’s long-term cycle may still be intact despite short-term volatility.

1. A Market Quietly Undergoing Structural Change

Although the cryptocurrency market ended 2025 on a relatively weak note, beneath the surface a profound structural transformation is underway. According to recent analysis by Binance Research, the market is no longer primarily shaped by retail speculation or short-term momentum trading. Instead, it is increasingly influenced by institutional capital flows, long-term portfolio strategies, and macro-driven asset allocation decisions.

This shift represents a maturation of the crypto market. Retail investors once dominated price discovery through rapid inflows and outflows driven by narratives and social media. Today, the emerging pattern resembles traditional capital markets, where positioning, hedging, and strategic exposure matter more than short-term hype.

Binance Research characterizes this phase as a “structural transition”, underpinned by government-level accumulation in emerging markets, proposed strategic crypto reserves in the United States, and the expanding role of regulated financial institutions.

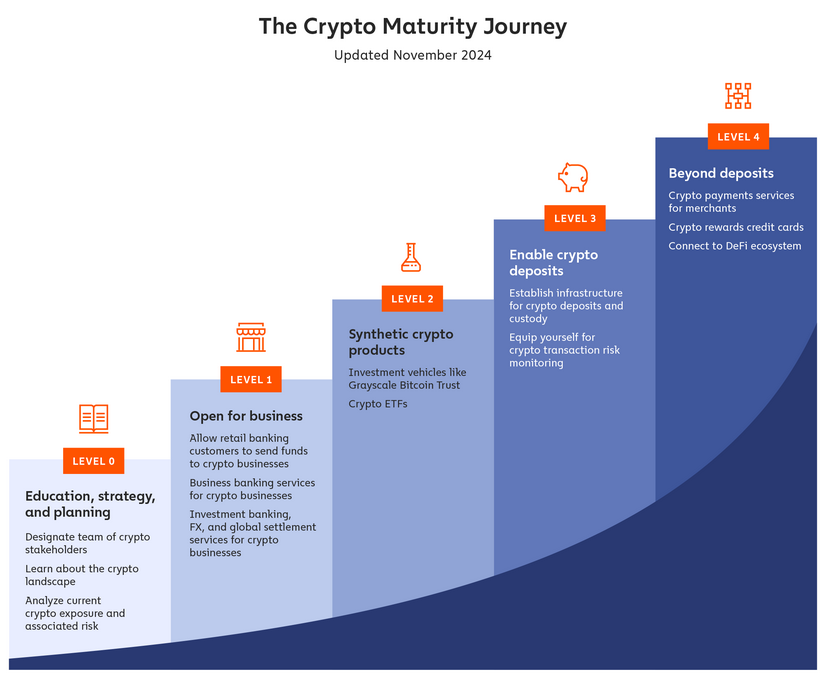

2. From First to Second Phase: Institutional Adoption Evolves

The approval of spot Bitcoin ETFs in the United States in early 2024 marked a historic milestone. That moment represented what Binance calls the first phase of institutional adoption—a phase defined by access.

In that phase:

- Institutions gained regulated exposure to Bitcoin.

- Custody, compliance, and reporting barriers were reduced.

- Bitcoin became investable for pension funds, RIAs, and conservative allocators.

The market has now entered a second phase, characterized not merely by access, but by active participation.

In this new phase:

- Wall Street firms are not just distributing crypto products.

- They are beginning to design, structure, and sponsor them.

- Crypto is treated as a strategic asset class rather than a speculative add-on.

3. Morgan Stanley’s Signal: From Distributor to Product Architect

One of the clearest signals of this second phase is the recent move by Morgan Stanley, which filed S-1 registrations related to Bitcoin and Solana ETF products.

This step is significant for several reasons.

First, it shows that a top-tier global investment bank is willing to place its balance sheet reputation behind crypto-linked investment vehicles. Second, it suggests that Wall Street firms are positioning themselves not just as intermediaries, but as originators of crypto financial products.

This development puts pressure on competitors such as Goldman Sachs and JPMorgan Chase. In emerging asset classes, early positioning often determines long-term dominance. Missing the initial product cycle could mean losing relevance in future portfolio construction frameworks.

【Institutional Crypto Adoption: Phase 1 vs Phase 2】

A comparative diagram showing “Access & Distribution” versus “Product Creation & Strategic Allocation”.

4. The DAT Question and the MSCI Turning Point

Another important theme highlighted by Binance Research is the role of Digital Asset Treasury (DAT) companies. These firms hold significant crypto assets on their balance sheets, often as part of treasury management strategies.

In recent months, DAT firms faced a serious risk: potential exclusion from MSCI indices. Such an exclusion could have triggered up to $10 billion in forced selling, as passive funds and index-linked strategies would be required to divest.

That risk receded after MSCI announced that DAT firms would not be removed from indices, at least for now.

This decision had two important effects:

- It stabilized sentiment around publicly listed crypto-adjacent firms.

- It reduced systemic downside risk tied to mechanical rebalancing.

The episode illustrates how deeply crypto is now intertwined with traditional financial infrastructure. Index methodology decisions—once irrelevant to crypto—now have direct market impact.

5. Macro Capital Rotation: Why 2026 Could Favor Crypto

Beyond crypto-specific developments, macroeconomic forces may provide a powerful tailwind. Binance Research points to increasing concern over concentration risk in traditional equity markets.

By 2025:

- The top 10 companies in the S&P 500 accounted for approximately 53% of the index’s total gains.

- Valuations of the so-called “Magnificent Seven” tech stocks reached historically elevated levels.

- AI-driven optimism led to extreme return concentration.

This environment encourages capital rotation. Institutional investors managing diversified portfolios may seek assets that:

- Are structurally uncorrelated with mega-cap tech.

- Offer asymmetric upside.

- Function as long-term hedges against monetary and fiscal risk.

Crypto assets, particularly Bitcoin, increasingly fit this profile.

【Equity Market Concentration vs Crypto Allocation Opportunity】

Bar chart comparing S&P 500 concentration levels with hypothetical diversified portfolio allocations including crypto.

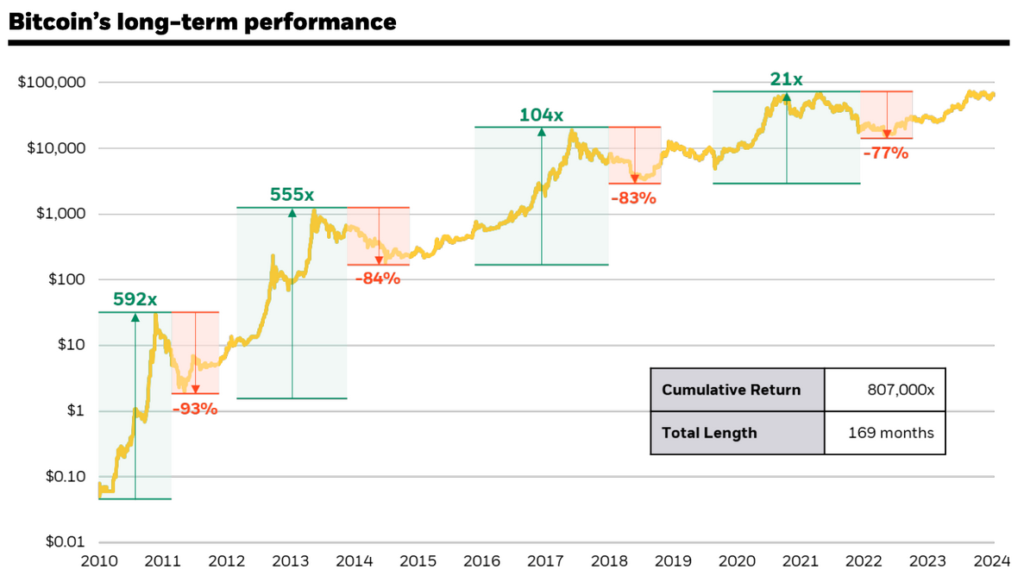

6. Bitcoin Cycles: Is the Market Really Topped?

Despite Bitcoin reaching a peak near $126,000 in October, market participants remain divided on whether the cycle has truly peaked.

Historically, Bitcoin has followed a four-year cycle linked to halving events. While cycles are not deterministic, they have repeatedly shaped long-term price behavior.

Several arguments suggest the cycle may not be over:

- Institutional allocation typically unfolds over years, not months.

- ETF inflows remain structurally sticky.

- Sovereign and quasi-sovereign interest is still in early stages.

Unlike previous cycles dominated by leverage and retail speculation, the current cycle is increasingly defined by balance sheet decisions and strategic reserves.

【Bitcoin Price Cycles and Institutional Entry Points】

Long-term Bitcoin price chart annotated with halving events and ETF approval milestones.

7. Implications for Investors and Builders

For investors, this environment favors:

- Long-term positioning over short-term trading.

- Assets with institutional-grade liquidity and regulatory clarity.

- Exposure aligned with macro diversification themes.

For builders and operators, the message is equally clear:

- Infrastructure, custody, compliance, and treasury tools will matter more than speculative applications.

- Products that integrate seamlessly with traditional finance will capture institutional demand.

- Stablecoins, tokenized assets, and settlement layers may see outsized growth.

Crypto is no longer just an alternative asset—it is becoming a portfolio component.

Conclusion: A Quiet but Profound Transition

The cryptocurrency market is entering a new era. While headlines may focus on price volatility, the deeper story is institutional integration. Morgan Stanley’s actions, MSCI’s decisions, and macro capital rotation all point toward the same conclusion: crypto is moving from the margins to the core of global finance.

This second phase of adoption will likely be slower, more methodical, and less euphoric than earlier cycles—but also more durable. For those seeking new digital assets, sustainable revenue opportunities, and practical blockchain applications, understanding this structural shift is no longer optional. It is essential.