Main Points :

- The European Union will enforce DAC8 from January 1, 2026, formally integrating crypto assets into its cross-border tax transparency regime.

- Crypto service providers will be required to collect and report detailed user and transaction data to national tax authorities, which will then be shared across EU member states.

- DAC8 complements—but is legally independent from—MiCA, creating a dual oversight structure: operational regulation plus fiscal surveillance.

- The new framework significantly raises compliance costs while reducing jurisdictional arbitrage opportunities that previously benefited offshore or lightly regulated crypto activity.

- For investors and builders, the shift signals a maturation phase of the crypto economy—reducing anonymity, but increasing institutional legitimacy and long-term capital inflows.

1. DAC8 Comes into Force: Crypto Fully Enters the EU Tax System

The European Union is entering a decisive phase in its treatment of digital assets. From January 1, 2026, the EU’s latest tax transparency directive—commonly referred to as DAC8—will come into force, fundamentally altering how cryptocurrencies are monitored, reported, and taxed across the bloc.

Until now, crypto assets occupied a grey zone. While banks and securities accounts have long been subject to automatic exchange of information between EU tax authorities, crypto transactions often escaped equivalent scrutiny. DAC8 is designed to close this gap decisively. Under the new rules, crypto-asset service providers (CASPs)—including exchanges, brokers, and custodial platforms—must systematically report user and transaction data to their national tax authorities.

What makes DAC8 particularly consequential is its cross-border architecture. Once data is collected at the national level, it is shared among EU member states through existing cooperation mechanisms. In practice, this means that crypto holdings and transactions will become as visible to tax authorities as traditional financial accounts, regardless of where in the EU the user or platform is based.

The directive applies with very limited transition time, placing immediate pressure on platforms to adjust internal systems, data schemas, and compliance workflows before enforcement begins.

2. Making Crypto Visible: What DAC8 Requires in Practice

Under DAC8, tax authorities gain access to comprehensive information covering the entire lifecycle of crypto ownership and activity. This includes acquisition, holding, transfers, and disposals, all mapped to identifiable users.

For crypto service providers, tax reporting can no longer be treated as a secondary compliance issue. Instead, it becomes a core operational requirement, comparable to KYC, AML, or transaction monitoring.

Key data points required under DAC8 include:

- Verified user identification details

- Transaction histories (buys, sells, swaps, transfers)

- Wallet balances and asset holdings

- Counterparty and transfer destination information where applicable

These requirements align crypto reporting more closely with existing frameworks used for banks and securities firms. The implication is clear: crypto platforms operating in or targeting the EU must invest in robust data infrastructure, audit trails, and regulatory reporting pipelines.

Failure to comply may result in financial penalties, reputational damage, or even loss of operational permission within EU jurisdictions.

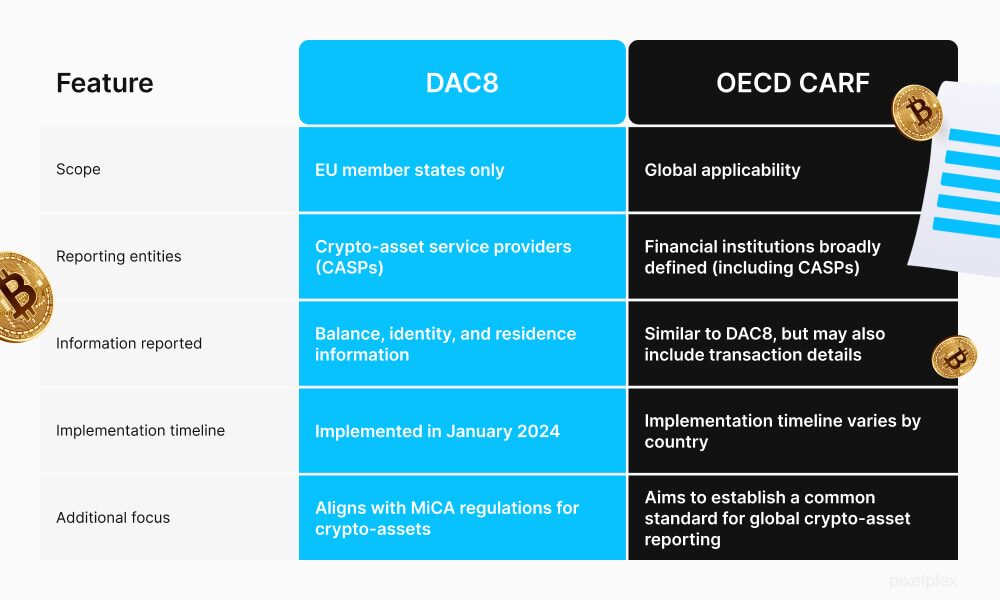

3. DAC8 and MiCA: Parallel Rules, Different Purposes

A common point of confusion is the relationship between DAC8 and MiCA. While both are pillars of the EU’s digital asset strategy, they address fundamentally different regulatory questions.

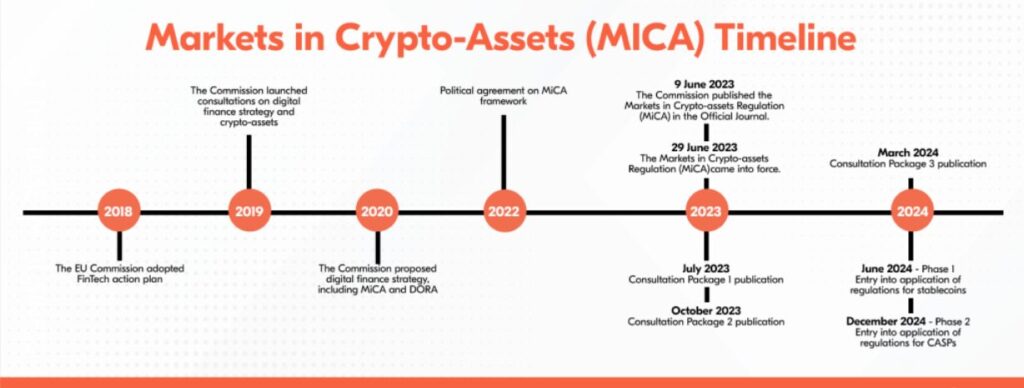

MiCA, approved in 2023, focuses on how crypto businesses operate. It sets rules for licensing, consumer protection, market conduct, reserve requirements for stablecoins, and operational governance within the EU single market.

DAC8, by contrast, focuses on what governments are allowed—and required—to see. Its purpose is fiscal: ensuring that individuals and companies pay the correct amount of tax on crypto-related income and gains.

In simple terms:

- MiCA tells companies how to run their business.

- DAC8 tells governments what financial data they are entitled to access.

Together, they establish a dual oversight regime. Crypto firms must now satisfy both operational compliance (MiCA) and fiscal transparency (DAC8), leaving little room for regulatory ambiguity.

4. Cross-Border Impact: The End of Jurisdictional Arbitrage

One of the most transformative aspects of DAC8 is its treatment of cross-border activity. Historically, many crypto users relied on jurisdictional complexity—using offshore platforms or cross-border accounts—to obscure taxable activity.

DAC8 significantly alters this risk calculus. Because tax data is shared automatically among EU member states, exploiting national differences becomes far more difficult. A user residing in one country but transacting through a platform registered in another will still be visible to both tax authorities.

This development effectively closes long-standing loopholes and aligns crypto taxation with the EU’s broader efforts to combat tax evasion in traditional finance.

For users, this means:

- Increased likelihood of detection for undeclared crypto gains

- Greater importance of accurate record-keeping and tax reporting

For platforms, it means:

- Heightened responsibility for data accuracy

- Exposure to regulatory action if reporting is incomplete or inconsistent

5. Market Implications: From Anonymity to Legitimacy

While DAC8 undoubtedly increases compliance burdens, it also marks a maturation milestone for the crypto sector. Regulatory clarity—especially in taxation—has long been a prerequisite for institutional adoption.

As transparency increases, crypto assets become more compatible with:

- Institutional portfolio allocation

- Regulated investment products

- Cross-border financial integration

For entrepreneurs and builders, the message is nuanced. Privacy-first narratives may lose appeal in regulated markets, but compliant infrastructure providers—especially those offering reporting-ready wallets, exchanges, and analytics—stand to benefit.

Investors seeking new digital assets and revenue opportunities should view DAC8 not merely as a constraint, but as a signal that crypto is transitioning from a speculative frontier to an integrated component of the global financial system.

Conclusion: A Turning Point for Crypto in Europe

DAC8 represents more than just another regulatory update—it is a structural shift in how crypto assets are perceived and governed within the European Union. By embedding digital assets into the same tax transparency framework as traditional finance, the EU is signaling that crypto is no longer an exception, but a permanent part of the economic system.

For market participants, the era of regulatory ambiguity is ending. In its place emerges a landscape defined by transparency, accountability, and—paradoxically—greater long-term opportunity for those prepared to operate within clear rules.