Main Points :

- The EU Council has formally endorsed a digital euro that works both online and offline, positioning it as a complement to cash, not a replacement.

- The offline mode aims to replicate cash-like privacy, while online payments integrate with existing financial infrastructure.

- Holding limits, free basic services, and fee controls are designed to protect financial stability and prevent large-scale bank deposit flight.

- The project signals how CBDCs can coexist with crypto assets, stablecoins, and private payment rails rather than eliminate them.

- For builders and investors, the digital euro offers insight into real-world blockchain-adjacent use cases, regulatory design, and future payment interoperability.

Introduction: A Turning Point for Europe’s Digital Money Vision

The European Union has taken a decisive step toward reshaping its monetary infrastructure. By agreeing to support a digital euro usable both online and offline, EU governments have clarified their collective stance on central bank digital currencies (CBDCs): they are not meant to erase cash, nor to crowd out private innovation, but to reinforce monetary sovereignty in an increasingly digital economy.

This decision, adopted as the official negotiating position of the Council of the European Union, advances discussions with the European Parliament and marks a crucial milestone in the long-running debate over whether—and how—Europe should issue a public digital currency. For readers interested in crypto assets, new revenue models, and practical blockchain applications, this development offers valuable lessons about how governments are translating theory into operational payment systems.

What the EU Actually Agreed On

At its core, the Council’s agreement confirms that the digital euro will launch with two complementary modes:

- Online digital euro – operating through standard digital infrastructure, regulated intermediaries, and account-based or token-based systems.

- Offline digital euro – enabling transactions without internet connectivity, later synchronized once a connection is restored.

This dual approach departs from earlier debates that emphasized offline payments almost exclusively as a digital analog to cash. Instead, EU policymakers now argue that resilience, usability, and inclusion require both modes to work together.

Importantly, the digital euro is explicitly framed as a complement to physical cash, not its replacement. The Council has linked the CBDC proposal to new rules reinforcing the role of euro banknotes and coins across member states, signaling political sensitivity to public concerns about cash disappearing.

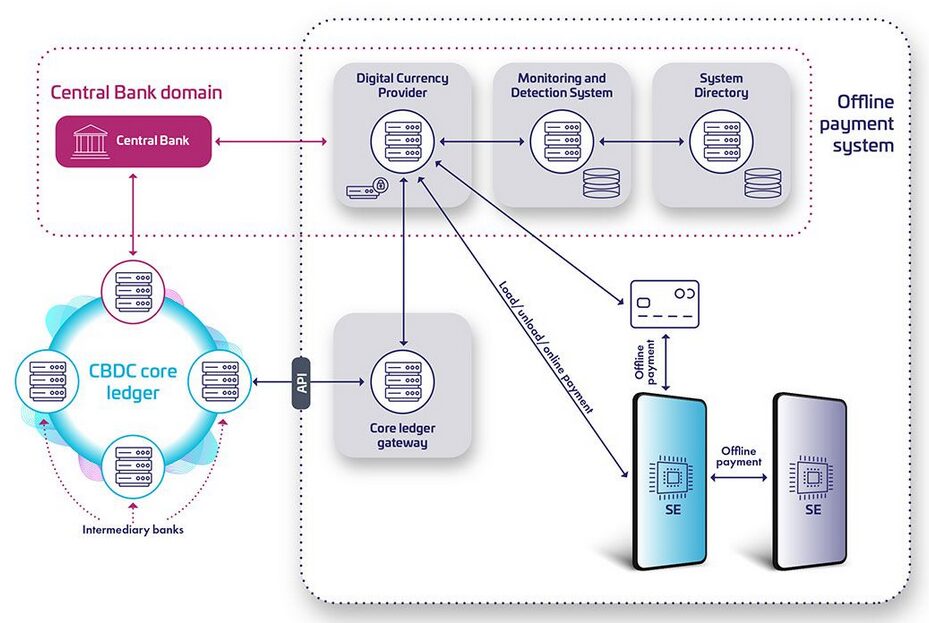

Offline Payments: Why They Matter More Than You Think

Offline functionality has become one of the most closely watched aspects of the digital euro. In practice, it means users can transact without an internet connection, during power outages, in rural areas, or in emergency situations.

From a technical perspective, offline payments raise complex questions:

- How are balances securely stored?

- How is double-spending prevented before synchronization?

- What level of transaction data—if any—is visible to intermediaries or the central bank?

EU officials emphasize that offline digital euro transactions should offer privacy comparable to cash, a claim that experts continue to scrutinize. Unlike public blockchains, where transactions are transparent by default, the offline digital euro is designed to minimize data exposure, with transaction details remaining on users’ devices until reconciliation.

For crypto practitioners, this is notable: it reflects a state-level attempt to recreate privacy-preserving value transfer, a goal long pursued by privacy coins and layer-2 payment channels.

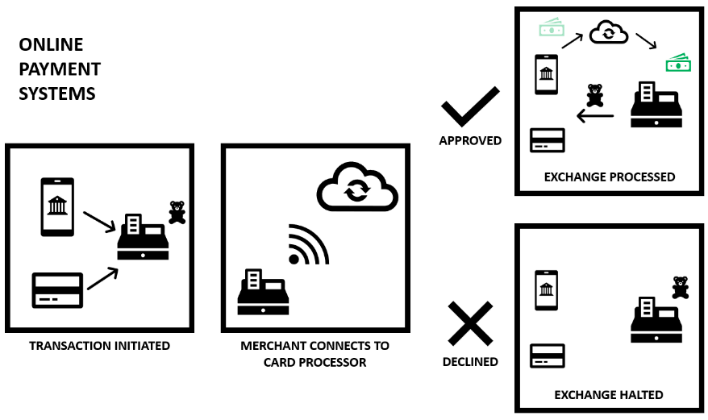

Online Payments: Integration Over Disruption

While offline payments attract attention, the online digital euro will likely handle the majority of transaction volume. These payments rely on:

- Authorized intermediaries (banks, payment institutions, fintechs),

- Existing digital rails,

- Compliance with EU rules on AML, consumer protection, and operational resilience.

Rather than displacing banks, the system deliberately keeps them in the loop, reducing political resistance and operational risk. This architecture contrasts with some crypto-native visions of fully disintermediated finance but aligns closely with real-world constraints.

For fintech operators and blockchain developers, this highlights a recurring pattern: mass adoption favors integration, not abrupt replacement.

Holding Limits and Financial Stability

One of the EU Council’s most consequential decisions concerns holding limits. Individuals will only be allowed to hold a capped amount of digital euros, with the European Central Bank empowered to set and periodically review these thresholds.

The rationale is straightforward:

- Prevent large-scale migration of deposits from commercial banks into risk-free central bank money.

- Preserve banks’ ability to lend to the real economy.

- Ensure the digital euro remains primarily a means of payment, not a store of value.

From an investment perspective, this design choice implicitly leaves room for crypto assets and stablecoins to continue serving as alternative stores of value and yield-generating instruments.

Fees, Costs, and User Experience

The Council also addressed concerns about cost and access. Under the agreed position:

- Basic digital euro services must be free for users.

- Payment service providers may charge fees only for optional or value-added services, subject to regulatory conditions.

This mirrors how cash works today—no fee to hold or spend it—and creates competitive pressure on private payment providers to differentiate through UX, integrations, and ancillary services rather than toll-style fees.

For builders, this suggests that future revenue opportunities will lie on top of payment rails, not in the rails themselves.

Christine Lagarde’s Message: Design Is Ready, Politics Decide

Speaking after the announcement, Christine Lagarde, President of the ECB, underscored that the technical groundwork is largely complete. The remaining question is political:

It is now up to the European Council, and later the European Parliament, to decide whether the European Commission’s proposal is satisfactory and how it should be legislated or amended.

This statement reflects a broader reality: CBDCs are no longer a technical experiment but a governance challenge. Privacy guarantees, resilience standards, and limits on state visibility into transactions will be negotiated as much in parliaments as in code.

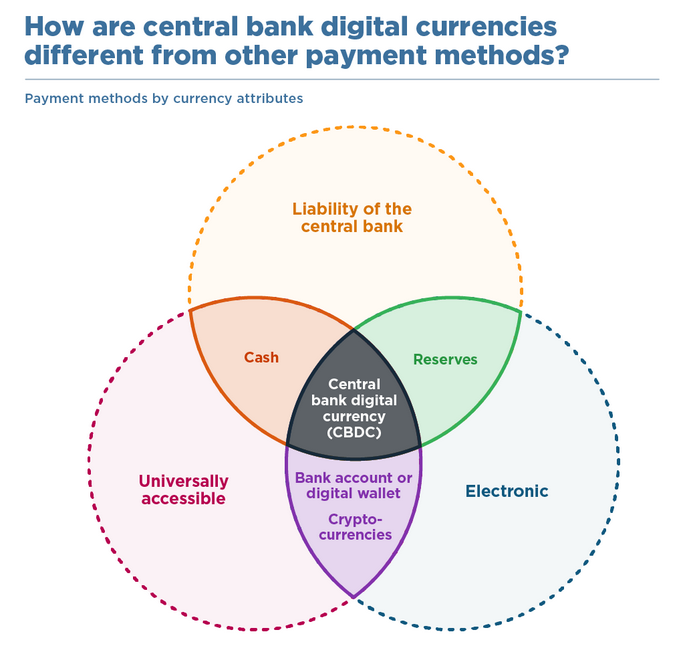

How the Digital Euro Fits Into the Crypto Landscape

For crypto-focused readers, the digital euro should not be viewed as an existential threat. Instead, it reshapes the environment in several ways:

- Legitimization of digital value transfer: CBDCs normalize the idea that money can be natively digital, lowering conceptual barriers for blockchain-based assets.

- Clear separation of roles: The digital euro targets payments, while crypto assets continue to dominate innovation in DeFi, tokenization, and programmable finance.

- Interoperability potential: Over time, regulated bridges between CBDCs, stablecoins, and tokenized assets could unlock new settlement and treasury use cases.

In this sense, the digital euro represents the “asset-backed representation” extreme of future finance—firmly rooted in state authority—coexisting with more autonomous crypto systems on the other end of the spectrum.

Timeline and What Comes Next

Although political agreement is advancing, experts estimate that it may take around two more years before the digital euro is fully launched. The upcoming negotiations with the European Parliament will likely focus on:

- Final privacy safeguards,

- Offline transaction thresholds,

- Governance and oversight mechanisms,

- The balance between resilience and regulatory control.

These debates will shape not only Europe’s payment system but also global norms for CBDC design.

Conclusion: Why This Matters Beyond Europe

The EU Council’s support for an online-and-offline digital euro is more than a regional policy decision. It is a global signal about how advanced economies intend to modernize money without abandoning core principles like privacy, financial stability, and cash accessibility.

For investors, builders, and entrepreneurs exploring new crypto assets and blockchain applications, the lesson is clear: the future will not be purely decentralized or purely centralized. Instead, it will be hybrid, shaped by careful compromises between innovation and institutional trust.

Understanding these dynamics today offers a strategic advantage tomorrow.