Main Points :

- China is considering a limited stablecoin pilot program inside designated Free Trade Zones (FTZs), not as deregulation but as a controlled policy experiment.

- The focus is cross-border trade settlement, auditing, and compliance, not domestic retail circulation.

- Qianhai FTZ and Hainan FTZ are identified as primary testbeds due to their existing offshore financial links.

- Hong Kong’s new stablecoin licensing regime (effective August 1, 2025) plays a crucial complementary role.

- A potential RMB-linked stablecoin could strengthen China’s external trade settlement options without relaxing capital controls.

- For global businesses and blockchain practitioners, this signals a new institutional use case rather than speculative crypto adoption.

1. Why China Is Reconsidering Stablecoins—Carefully

For years, China has maintained one of the world’s strictest stances on cryptocurrencies. Public trading, mining, and open circulation have been systematically restricted, primarily due to concerns over capital flight, illicit finance, and monetary sovereignty.

Yet in 2025, amid accelerating global adoption of regulated stablecoins, a different narrative has begun to emerge: not whether stablecoins should exist, but where and how they can be used safely.

According to a policy proposal reported by Caijing, China is examining the possibility of pilot stablecoin usage within specific Free Trade Zones, strictly limited to cross-border transactions and institutional participants. Importantly, this proposal does not originate from financial regulators as binding policy, but from academic and policy research circles aiming to explore practical solutions under existing capital controls.

The core logic is simple but powerful:

If stablecoins can be used in a closed, auditable, and geographically limited environment, they may enhance trade efficiency without undermining financial stability.

This represents a shift from outright prohibition toward regulatory experimentation, a pattern China has historically used in areas such as special economic zones, offshore finance, and digital infrastructure.

2. Free Trade Zones as Regulatory Sandboxes

Why FTZs Matter

China’s Free Trade Zones already function as policy laboratories. Within these zones, regulators test reforms related to foreign exchange, cross-border financing, and trade settlement before deciding whether they can be scaled nationally.

The proposal identifies two prime candidates:

- Qianhai Free Trade Zone (Shenzhen)

- Hainan Free Trade Port

Qianhai Free Trade Zone and Hainan Free Trade Port both already host:

- Cross-border RMB settlement pilots

- Offshore financing mechanisms

- Close regulatory coordination with customs and FX authorities

Under the proposal, any stablecoin activity would occur inside a closed-loop regulatory sandbox, supervised jointly by local financial bureaus and foreign exchange regulators. Domestic individual users would be explicitly excluded, and no open circulation within mainland China would be allowed.

3. The Hong Kong Connection: A Parallel Track, Not a Loophole

A critical external factor is Hong Kong’s stablecoin legislation.

Hong Kong passed its Stablecoin Ordinance on May 21, 2025, with full implementation scheduled for August 1, 2025. This makes Hong Kong one of the few major financial centers with a formal licensing regime for fiat-referenced stablecoins.

From Beijing’s perspective, Hong Kong offers:

- A legally distinct jurisdiction

- Deep international financial connectivity

- A compliant framework aligned with global standards

Rather than bypassing mainland controls, the FTZ proposal envisions regulatory alignment with Hong Kong’s licensing system. Stablecoin issuers operating in Hong Kong could potentially interface with FTZ-based pilots under tightly defined rules.

This approach allows China to:

- Observe stablecoin operations in a mature legal environment

- Avoid domestic retail exposure

- Support trade settlement without liberalizing the capital account

4. Stablecoins as Trade Infrastructure, Not Consumer Money

Practical Use Cases Already Emerging

Despite domestic bans, stablecoins are already informally used in international trade, especially in regions where:

- USD liquidity is limited

- Local currencies are volatile

- Traditional correspondent banking is slow or expensive

Blockchain-based settlement offers:

- Near-instant finality

- Lower transaction costs

- Peer-to-peer efficiency

- Transparent audit trails

For exporters and importers dealing with politically or economically unstable regions, stablecoins have become a functional settlement layer, not an investment vehicle.

Why This Matters for China

China is the world’s largest trading nation. Even marginal efficiency gains in cross-border settlement can translate into billions of dollars in cost savings annually.

Allowing stablecoins inside FTZs could:

- Reduce FX friction in trade settlement

- Improve auditability and compliance

- Complement existing RMB cross-border payment systems

5. The Strategic Case for an RMB-Linked Stablecoin

Perhaps the most consequential implication is the possibility—still theoretical—of a RMB-referenced stablecoin used exclusively for external trade settlement.

Such an instrument would:

- Not circulate domestically

- Not replace the digital RMB (e-CNY)

- Operate only in approved cross-border scenarios

If implemented, it could:

- Expand RMB usage in international trade

- Reduce dependency on USD-denominated stablecoins

- Strengthen China’s monetary influence without opening capital accounts

This would position stablecoins as infrastructure for trade, not as competing money.

6. Global Context: Stablecoin Regulation Is Converging

China’s cautious exploration mirrors a broader global trend:

- The EU’s MiCA framework

- Hong Kong’s licensing regime

- US legislative proposals around payment stablecoins

Across jurisdictions, regulators are converging on a model where stablecoins are:

- Fully reserved

- Audited

- Institutionally issued

- Restricted in use

China’s FTZ experiment would fit squarely within this emerging global norm—highly regulated, purpose-specific digital settlement assets.

7. Implications for Blockchain Practitioners and Investors

For readers interested in new crypto assets, revenue models, and practical blockchain applications, this development signals a clear message:

- The next growth phase is institutional and infrastructural, not retail speculation.

- Compliance-first design will dominate future adoption.

- Cross-border settlement, trade finance, and auditing are primary use cases.

Projects aligned with:

- Regulated stablecoin infrastructure

- Cross-border compliance tooling

- On-chain audit and reporting systems

are likely to see increasing demand.

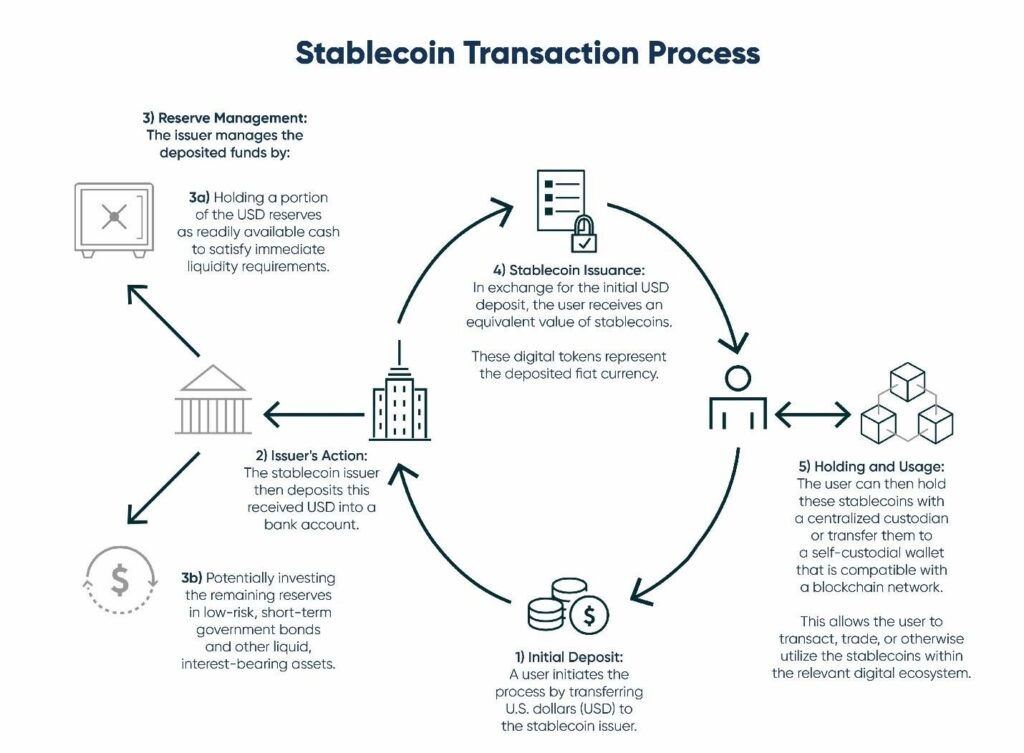

8. Visual Explanation (Insert Here)

“Closed-Loop Stablecoin Flow in China FTZs”

Description:

This diagram illustrates how a licensed stablecoin issuer (aligned with Hong Kong regulation) interacts with FTZ-based enterprises, regulators, and overseas counterparties within a closed, auditable loop.

9. Conclusion: A Distinctly Chinese Path Forward

China’s consideration of stablecoin pilots in Free Trade Zones does not signal a return to open crypto markets. Instead, it reflects a pragmatic, state-led approach to harnessing blockchain efficiency while preserving financial control.

By limiting scope, geography, and participants, China is testing whether stablecoins can function as neutral trade infrastructure, not speculative assets. If successful, this model could redefine how digital money is integrated into global commerce—quietly, carefully, and at scale.

For the global blockchain industry, this is not a story of deregulation, but of institutionalization.