Main Points :

- More than 125 crypto companies have jointly opposed an expanded interpretation of the GENIUS Act that could restrict stablecoin reward programs.

- The dispute centers on whether stablecoin rewards offered by platforms or applications should be treated the same as interest paid by issuers, which is already prohibited.

- The crypto industry argues that banning platform-level rewards would harm competition, innovation, and consumer choice, pushing payments back toward traditional banks.

- Banks counter that platform rewards resemble interest-bearing deposits and pose similar systemic risks.

- This debate reflects a broader struggle over the future of digital payments, stablecoin economics, and bank–fintech competition in the United States.

Introduction: A Regulatory Fault Line in the Stablecoin Era

Stablecoins have rapidly evolved from a niche crypto instrument into a core component of global digital payments, remittances, and decentralized finance. Pegged to fiat currencies such as the U.S. dollar, they offer speed, programmability, and global accessibility—features increasingly attractive to both consumers and businesses.

Yet as stablecoins gain traction, they inevitably collide with the interests of traditional banking institutions. That collision is now playing out in Washington, D.C., where more than 125 crypto companies have united to oppose what they see as an overreach in the interpretation of the GENIUS Act, a foundational piece of U.S. stablecoin legislation.

At the heart of the dispute lies a deceptively simple question:

Should platforms and applications be allowed to offer rewards or incentives for holding or using stablecoins, even if issuers themselves are prohibited from paying interest?

What Is the GENIUS Act and Why It Matters

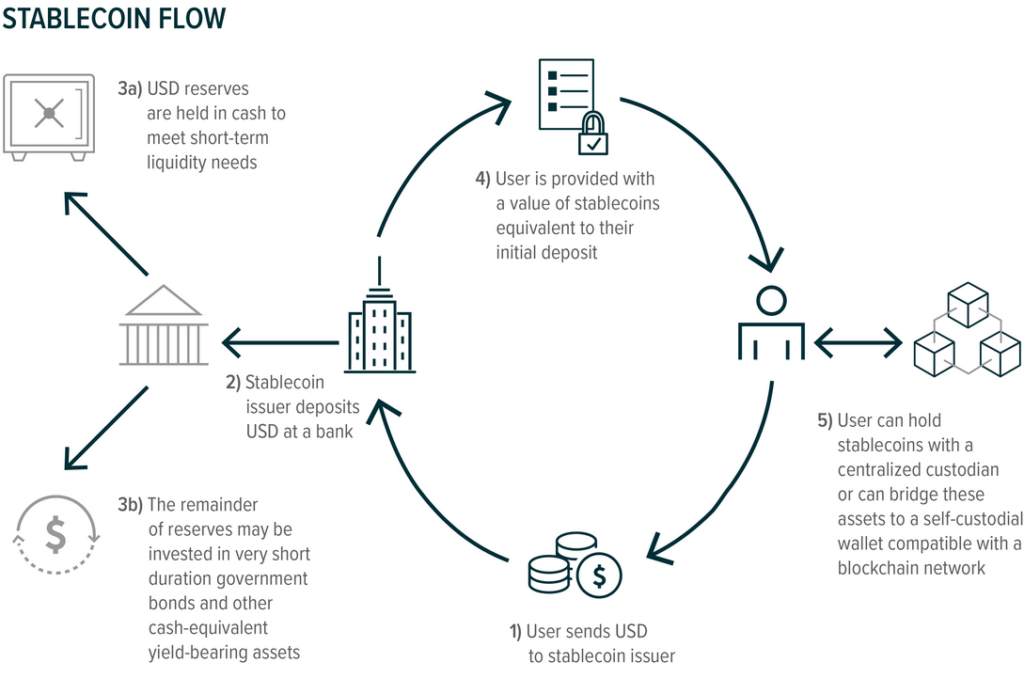

The GENIUS Act was designed to create a clear regulatory framework for stablecoins in the United States. One of its core principles is the separation of roles:

- Issuers: Entities that mint stablecoins and manage reserves.

- Platforms and intermediaries: Exchanges, wallets, and applications that distribute, custody, or enable usage of those stablecoins.

Under the law, issuers are explicitly prohibited from paying interest or yield directly to token holders. This restriction was intended to avoid bank-like risk profiles, such as maturity transformation or implicit guarantees that could threaten financial stability.

However, lawmakers intentionally left room for non-issuer platforms to design lawful incentive programs, such as cashback, loyalty points, or usage-based rewards. According to the crypto industry, this distinction was not an oversight but a deliberate policy choice.

The Industry Pushback: A United Front of 125 Companies

Led by the Blockchain Association, a coalition of more than 125 crypto firms sent a formal letter to the U.S. Senate Banking Committee urging lawmakers to reject any attempt to broaden the GENIUS Act’s restrictions.

The letter was addressed to Committee Chair Tim Scott and Ranking Member Elizabeth Warren, both of whom play pivotal roles in shaping U.S. financial legislation.

The coalition warned that reopening or reinterpreting settled provisions of the GENIUS Act would:

- Reintroduce regulatory uncertainty

- Undermine trust in newly enacted financial laws

- Discourage long-term investment in compliant crypto infrastructure

In their view, the timing could not be worse—coming amid rare bipartisan cooperation on broader market structure reforms.

Why Stablecoin Rewards Matter to Crypto Platforms

To outsiders, stablecoin rewards may sound like a minor feature. In reality, they are central to user adoption and platform competition.

1. Consumer Incentives and Adoption

Stablecoin rewards often function like:

- Cashback on payments

- Rebates on transaction fees

- Loyalty incentives for frequent usage

These mechanisms encourage users to actually spend and circulate stablecoins, rather than merely holding them.

2. Competition With Traditional Finance

In traditional finance, banks pay little to no interest on checking accounts, while credit card companies offer points, miles, and cashback funded by interchange fees and partnerships.

Crypto platforms argue that stablecoin rewards are economically closer to credit card rewards than to bank interest—and should be treated accordingly.

3. Innovation at the Application Layer

If platforms are barred from offering rewards, innovation becomes centralized at the issuer level—or worse, disappears entirely. Smaller fintechs and crypto startups would lose a critical tool to compete with large incumbents.

The Banking Industry’s Position: Risk by Another Name

Banking groups have pushed back hard, arguing that platform-level rewards are merely interest in disguise.

Their core claims include:

- Rewards create yield expectations, similar to deposits.

- Users may misunderstand risks, assuming implicit guarantees.

- Platform incentives could incentivize excessive leverage or risk-taking.

From the banks’ perspective, allowing non-issuers to pay rewards undermines the spirit of the GENIUS Act, even if it technically complies with the letter of the law.

Critics within the crypto industry counter that this stance reflects competitive self-interest, especially as U.S. banks prepare to launch their own stablecoin initiatives.

Voices From the Industry: Gemini and Beyond

Prominent industry leaders have spoken out publicly. Gemini co-founder Tyler Winklevoss described the situation as an attempt by banks to reopen a legislative battle they already lost.

According to Winklevoss and others, the GENIUS Act struck a careful balance:

- Limiting issuer risk

- Preserving market-driven innovation

- Preventing stablecoins from becoming shadow banks

Rewriting that balance now, they argue, would chill innovation precisely when the U.S. is trying to remain competitive in global fintech.

Broader Market Implications: Payments, Fintech, and Power

This debate goes far beyond stablecoin rewards.

Impact on Digital Payments

If rewards are banned:

- Stablecoins may become less attractive for everyday payments.

- Merchants may revert to traditional card networks.

- Consumers lose low-cost, borderless payment options.

Competitive Dynamics

Large banks already benefit from:

- Regulatory moats

- Established customer bases

- Control over fiat on-ramps

Restricting platform rewards would disproportionately hurt small fintechs and crypto startups, reinforcing existing market concentration.

Global Competitiveness

Other jurisdictions—such as parts of Asia and the Middle East—are actively encouraging stablecoin innovation. Excessive restrictions in the U.S. could push talent and capital offshore.

Economic Context: Stablecoins as Dollar Infrastructure

Stablecoins increasingly function as digital dollar infrastructure, especially in emerging markets and cross-border commerce. By some estimates, stablecoin transaction volumes already rival major payment networks, all while operating 24/7 at a fraction of the cost.

Rewards help bootstrap this infrastructure by:

- Encouraging liquidity

- Promoting circulation

- Aligning user behavior with network growth

Removing them risks slowing adoption at a critical inflection point.

Conclusion: A Defining Moment for Crypto and Banking

The clash over stablecoin rewards is not merely a technical regulatory dispute—it is a referendum on who gets to shape the future of money.

Crypto companies argue that the GENIUS Act deliberately separated issuers from platforms to balance safety with innovation. Banks argue that any form of yield undermines financial stability.

How lawmakers resolve this tension will determine whether stablecoins evolve into an open, competitive payment layer—or are absorbed back into the traditional banking system.

For investors, builders, and entrepreneurs seeking new crypto assets, revenue models, and practical blockchain applications, this battle is a signal event. The outcome will shape not only stablecoins, but the broader trajectory of digital finance in the coming decade.