Main Points :

- U.S. lawmakers have proposed targeted tax relief to make stablecoins usable for everyday payments without triggering burdensome capital gains reporting.

- Small stablecoin transactions (up to $200 per transaction) would no longer require gain or loss recognition, provided the coins meet strict regulatory standards.

- Staking and mining rewards could benefit from a tax deferral option of up to five years, addressing the long-standing issue of “phantom income.”

- The proposal seeks to balance consumer adoption, innovation, and anti-abuse safeguards, while keeping Treasury oversight intact.

- Industry groups warn that over-restricting stablecoin rewards could entrench incumbents and undermine fair competition.

- If enacted, the reforms could materially accelerate real-world crypto payments, yield-based strategies, and enterprise blockchain use cases.

Introduction: Why Crypto Tax Reform Is Back on the Agenda

In the United States, digital assets have long existed in a paradoxical regulatory environment. On the one hand, blockchain technology has matured to the point where stablecoins are routinely used for remittances, on-chain settlement, payroll experiments, and merchant payments. On the other hand, the tax code still treats most everyday crypto usage as if it were speculative trading.

This disconnect has created a practical barrier: every coffee bought with a stablecoin is technically a taxable event. Even when the asset is pegged to the U.S. dollar and fluctuates by only fractions of a cent, users are required to calculate gains or losses, record cost basis, and potentially report them to the IRS. For mass adoption, this friction is untenable.

Against this backdrop, U.S. Representatives Max Miller (Ohio) and Steven Horsford (Nevada) have introduced a discussion draft aimed at modernizing the Internal Revenue Code. Their proposal focuses on two areas where tax friction is most acute: small-value stablecoin payments and staking or mining rewards.

What makes this proposal particularly notable is not only the technical detail, but also the philosophy behind it. Rather than attempting a sweeping rewrite of crypto taxation, the draft targets specific pain points that block everyday usage and sustainable yield generation.

Stablecoins as Money, Not as Speculation

The Core Problem with Small Payments

Stablecoins are designed to maintain a value close to $1.00. Yet under current U.S. tax rules, they are treated as property, not currency. This means that even a $5 purchase using a dollar-pegged stablecoin can trigger a taxable event.

In practice, the gains or losses are often negligible—fractions of a dollar—but the compliance burden is disproportionate. For users, merchants, and payment providers, this complexity discourages adoption altogether.

The lawmakers’ draft explicitly acknowledges this mismatch. It argues that regulated payment stablecoins should be treated differently from volatile crypto assets, especially when used for consumer transactions.

The $200 De Minimis Exemption

Under the proposal, gains or losses would not need to be recognized for stablecoin transactions of $200 or less, provided several conditions are met:

- The stablecoin must be issued by an authorized issuer under the framework envisioned by the GENIUS Act.

- It must be pegged to the U.S. dollar and trade within a narrow price band around $1.00.

- The transaction must be a payment, not part of broker-dealer or trading activity.

This structure mirrors existing de minimis exemptions used in other parts of the tax code, such as foreign currency transactions. The intent is clear: using stablecoins to pay for groceries, subscriptions, or transport should not feel like filing a trading ledger.

Anti-Abuse Safeguards

To prevent the exemption from becoming a loophole, the draft includes several guardrails:

- Stablecoins that de-peg materially would be excluded.

- Brokers and dealers cannot use the exemption for business activity.

- The U.S. Treasury retains authority to impose reporting and anti-fraud rules.

In other words, the proposal aims to enable daily use while preserving regulatory control over systemic risks.

Implications for Payments, Merchants, and Fintech Platforms

If enacted, this change could have far-reaching effects beyond individual users.

For merchants, accepting stablecoins would become operationally simpler. No longer would every transaction require complex accounting logic to track micro-gains.

For fintech and payment platforms, especially those building crypto-native wallets or EMI-like services, the exemption lowers one of the biggest barriers to integrating stablecoins as a true payment rail.

For cross-border use cases, such as remittances or B2B settlement, the psychological shift may be just as important as the legal one. Stablecoins would move closer to being treated as digital cash equivalents, not speculative instruments.

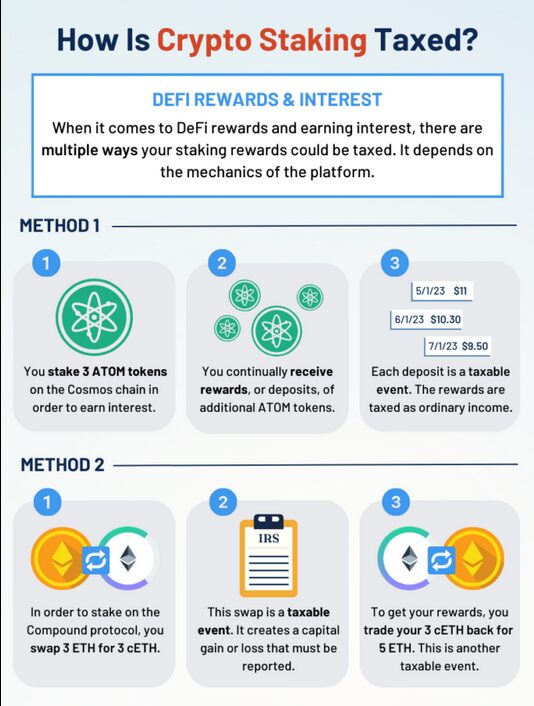

Staking and Mining: Solving the “Phantom Income” Problem

What Is Phantom Income?

One of the most controversial aspects of crypto taxation is the treatment of staking and mining rewards. Under current interpretations, rewards may be taxable at the moment they are received, even if:

- The tokens are illiquid,

- The market price later collapses,

- Or the user never actually sells the asset.

This creates what many in the industry call “phantom income”—tax liability without realized cash flow.

A Five-Year Deferral Option

The proposed bill introduces a pragmatic compromise. Taxpayers would be allowed to defer income recognition on staking or mining rewards for up to five years.

This does not eliminate taxation, nor does it push recognition all the way to the point of sale. Instead, it acknowledges that immediate taxation at receipt is often economically unrealistic.

The draft explicitly frames this as a middle ground between two extremes:

- Immediate taxation upon gaining control of the asset, and

- Full deferral until disposal.

By allowing deferral, the proposal reduces forced selling pressure and aligns tax timing more closely with economic reality.

Why This Matters for Yield-Driven Crypto Strategies

For readers interested in new income sources, this change could be transformative. Staking, validator operations, and even institutional-grade yield strategies become more predictable when tax obligations are not front-loaded.

This is particularly relevant for long-term infrastructure participants—validators, node operators, and protocol contributors—who reinvest rewards into securing networks rather than liquidating them immediately.

Beyond Payments and Staking: Broader Tax Modernization

The discussion draft goes further than just two headline issues. It also proposes:

- Applying existing securities lending tax rules to certain digital asset lending arrangements.

- Extending wash sale rules to actively traded cryptocurrencies, closing perceived loopholes.

- Allowing traders and dealers to elect mark-to-market accounting for digital assets, aligning crypto with traditional financial instruments.

Taken together, these provisions suggest a broader intent: to integrate digital assets into the existing tax architecture, rather than treating them as anomalies.

Industry Pushback: The Stablecoin Rewards Debate

While lawmakers are moving toward tax relief, not all regulatory trends point in the same direction.

Recently, the Blockchain Association, representing more than 125 crypto companies and organizations, sent a letter to the U.S. Senate Banking Committee. The letter urged lawmakers to reconsider efforts to restrict stablecoin rewards, particularly proposals that would extend limitations beyond issuers to third-party platforms.

The association argues that:

- Stablecoin rewards are economically similar to bank rewards or credit card incentives.

- Prohibiting them in the crypto context would distort competition.

- Over-restriction risks entrenching large incumbents while stifling innovation by smaller platforms.

This tension highlights a recurring theme in crypto regulation: how to protect consumers without freezing market structure.

Strategic Outlook: What This Means for the Crypto Ecosystem

From a strategic perspective, the proposed tax reforms signal an important shift in U.S. policymaking.

First, they implicitly recognize that crypto is no longer a fringe investment activity, but a functional component of payment and financial infrastructure.

Second, they suggest a willingness to differentiate between use cases—payments versus speculation, infrastructure participation versus trading.

Third, they align with a global trend. Other jurisdictions, from parts of Europe to Asia, are experimenting with similar de minimis exemptions and staking-friendly frameworks to attract builders and capital.

For entrepreneurs, investors, and operators focused on practical blockchain deployment, these developments reduce uncertainty. They make it easier to model cash flows, design compliant products, and justify long-term participation.

Conclusion: A Small Change with Outsized Impact

At first glance, a $200 exemption or a five-year deferral might seem modest. In reality, these measures address some of the most persistent friction points preventing crypto from functioning as everyday financial infrastructure.

By easing the tax burden on small stablecoin payments, lawmakers open the door to genuine consumer adoption. By offering relief from phantom income, they support sustainable yield generation and network security. And by embedding digital assets more cleanly into existing tax concepts, they move the industry closer to regulatory normalcy.

For those seeking new crypto assets, next-generation revenue models, or real-world blockchain applications, this proposal is more than a tax tweak. It is a signal that the rules of the game are beginning to evolve in favor of utility, not just speculation.