Main Points :

- Visa has begun using USDC, a dollar-denominated stablecoin, for settlement with U.S. issuing banks and acquiring banks.

- The settlement layer—not the user-facing card experience—is being rebuilt on blockchain infrastructure.

- Initial settlement uses Solana, with a planned future migration to Circle’s proprietary Layer-1 blockchain, Arc.

- This move represents a structural shift from legacy fiat-based clearing systems to 24/7 on-chain settlement.

- Stablecoins are emerging as a new financial “operating layer” rather than merely crypto trading instruments.

- The initiative signals acceleration in tokenization, treasury automation, and TradFi–DeFi convergence heading into 2026.

Introduction: A Quiet but Structural Shift in Global Payments

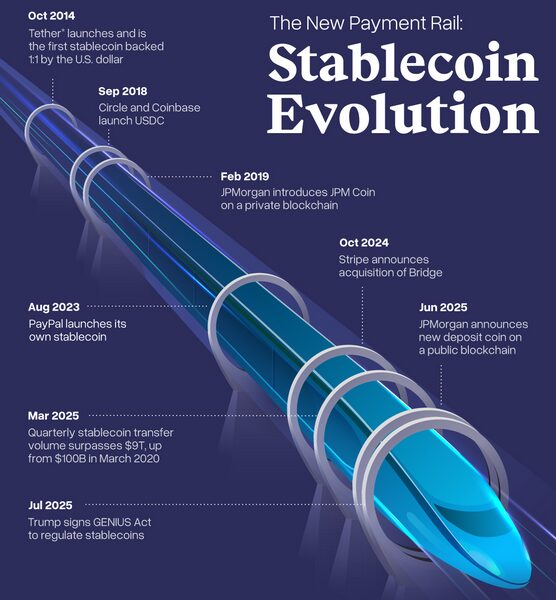

On December 16, Visa announced that it has officially begun USDC-based settlement in the United States. At first glance, this may sound like yet another experiment by a traditional financial institution dipping its toes into blockchain. In reality, this move is far more consequential.

Visa is not changing how consumers swipe cards, tap phones, or check out online. What is changing—fundamentally—is how money moves behind the scenes, at the settlement layer of the world’s largest payment network.

By allowing issuing banks and acquiring banks to settle obligations directly with Visa using USDC, Visa is effectively rebuilding its clearing infrastructure on blockchain rails. This is not a pilot limited to fringe use cases; it is the early stage of a system-wide migration that could redefine how global payments work.

Visa Is Not a “Card Company”—It Is a Global Settlement Network

When people hear the name Visa, they typically think of plastic cards, logos on checkout pages, and consumer payments. That perception misses the core of Visa’s business.

Visa operates one of the most extensive global settlement and messaging networks in existence. Every day, it coordinates payment instructions, netting, clearing, and settlement among thousands of banks and merchants across borders.

Traditionally, this system relies on:

- Fiat currencies (primarily USD)

- Banking hours (five business days)

- Correspondent banking relationships

- Batch-based reconciliation and treasury operations

By introducing USDC settlement, Visa is redefining this foundation.

What Exactly Has Changed: USDC at the Settlement Layer

Under the new framework:

- Issuing banks (which issue Visa cards)

- Acquiring banks (which serve merchants)

can now settle directly with Visa using USDC, rather than traditional bank transfers in USD.

The stablecoin used is USDC, issued by Circle, and fully backed by dollar-denominated assets.

Crucially:

- The consumer experience remains unchanged

- The blockchain operates entirely in the background

- Settlement becomes 24/7/365, not constrained by banking calendars

This is not a crypto payment feature for end users—it is infrastructure modernization.

Why Blockchain Settlement Matters: Speed, Liquidity, and Automation

Visa highlights three core benefits of its U.S. stablecoin settlement framework:

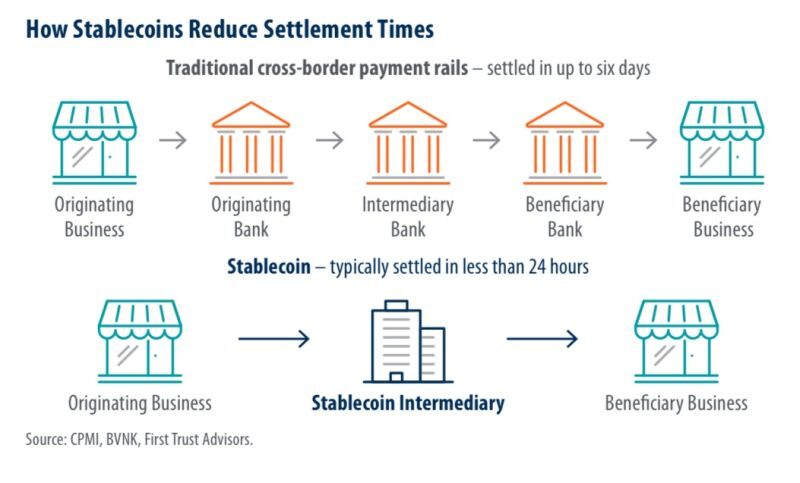

1. Seven-Day Settlement

Traditional settlement operates on a five-business-day cycle. By moving to blockchain-based USDC settlement, Visa enables continuous, seven-day settlement, improving cash flow and reducing idle capital.

For banks and fintechs, this translates into:

- Faster capital recycling

- Lower liquidity buffers

- Improved operational efficiency

2. Advanced Treasury and Liquidity Management

On-chain settlement allows for automated treasury operations, including:

- Real-time balance visibility

- Programmatic fund movement

- Reduced reconciliation overhead

For large institutions managing billions of dollars in daily flows, automation at this level is transformative.

3. Interoperability Between Legacy Rails and Blockchain

Visa is not abandoning existing payment rails. Instead, it is acting as a bridge between traditional financial infrastructure and blockchain networks, enabling gradual migration without disrupting existing ecosystems.

Why Solana Was Chosen for the Initial Phase

For the first phase, Visa selected Solana as the underlying blockchain for USDC settlement.

This choice is significant.

While Ethereum dominates in terms of ecosystem size, and Avalanche has gained traction in institutional finance, Solana offers a unique combination of:

- High transaction throughput

- Extremely low transaction fees

- Proven large-scale USDC circulation

- Fast finality suitable for payment use cases

In settlement infrastructure, speed and cost predictability matter more than decentralization maximalism. Solana fits that operational profile.

From Solana to Arc: Circle’s Vision for a Dedicated Financial Layer

Visa’s blockchain strategy does not stop at Solana.

Visa is also a design partner for Arc, a Layer-1 blockchain currently being developed by Circle. Arc is now in public testnet.

Once Arc becomes fully operational:

- Visa plans to use Arc for internal USDC settlement

- Visa intends to operate validator nodes on the network

- Settlement infrastructure becomes purpose-built for regulated financial institutions

This marks a critical evolution: instead of relying solely on general-purpose public blockchains, financial institutions may converge on specialized, compliance-aware Layer-1 networks.

Stablecoins as Financial Infrastructure, Not Speculative Assets

This development underscores a broader trend: stablecoins are becoming financial plumbing.

As of November 30, Visa reported that its monthly stablecoin settlement volume had surpassed $3.5 billion (annualized). This is not retail speculation—it is institutional money movement.

Stablecoins now serve as:

- Settlement assets

- Liquidity management tools

- Treasury instruments

- Bridges between banking systems and blockchains

They are increasingly comparable to central bank reserves, but with programmability and global reach.

Tokenization and On-Chain Finance: Why 2026 Matters

Looking ahead to 2026, several forces are converging:

- Tokenization of financial assets

- On-chain treasury management

- Integration of TradFi and DeFi systems

- Regulatory clarity for stablecoins and digital assets

Visa’s move should be seen as preparatory infrastructure work for this next phase of finance.

Once settlement is on-chain, extending tokenization to:

- Bonds

- Funds

- Trade finance instruments

- Cross-border remittances

becomes far easier.

Conclusion: A Blueprint for the Future of Global Payments

Visa’s adoption of USDC for settlement is not a headline-grabbing consumer feature—but it may be one of the most important financial infrastructure shifts of this decade.

By quietly rebuilding its settlement layer on blockchain technology, Visa is signaling that the future of money movement will be:

- Always-on

- Programmable

- Token-based

- Interoperable with traditional finance

For those seeking new crypto assets, revenue opportunities, or practical blockchain use cases, this development offers a clear message: the real value is moving to the infrastructure layer.

Japan and other markets are likely to follow. The rails are being laid now.