Main Points :

- Visa has officially launched USDC-based settlement for U.S. banks using the Solana blockchain, moving stablecoins from pilot projects into full-scale financial infrastructure.

- Banks can access faster, programmable, and 24/7 settlement without changing consumer-facing card experiences.

- Solana’s high throughput and near-instant finality make it suitable for institutional payment volumes.

- Stablecoin settlement volumes have reached an annualized run rate of $3.5 billion, signaling real demand from financial institutions.

- Visa’s strategy bridges traditional finance and blockchain, positioning stablecoins as a core layer of next-generation payment rails.

- Parallel initiatives such as Circle’s upcoming Layer-1 blockchain “Arc” suggest a multi-network future for institutional crypto payments.

1. Visa’s Strategic Shift: From Experimentation to Production-Grade Blockchain Payments

Visa’s decision to roll out USDC settlement for U.S. banks on Solana represents a decisive shift in how global payment networks view blockchain technology. For years, stablecoins were framed as experimental tools or niche instruments primarily used in crypto-native environments. With this move, Visa is effectively declaring that blockchain-based settlement has matured enough to support regulated financial institutions at scale.

Under the new framework, U.S. card issuers and acquiring banks can settle transactions using USDC, the dollar-backed stablecoin issued by Circle. Crucially, this settlement occurs on-chain via Solana, while the consumer-facing experience remains unchanged. Cardholders still swipe, tap, or pay online as usual; the transformation happens entirely in the backend.

This design choice addresses one of the largest barriers to blockchain adoption in traditional finance: disruption. Banks do not need to redesign customer interfaces, retrain users, or abandon existing card workflows. Instead, blockchain becomes an invisible infrastructure layer that enhances speed, flexibility, and operational efficiency.

2. Why Solana? Performance, Cost, and Institutional Suitability

Visa’s selection of Solana is not accidental. Among major public blockchains, Solana stands out for three characteristics that matter deeply to institutional payments:

- High throughput – Solana can process thousands of transactions per second under real-world conditions.

- Fast finality – Transactions typically reach finality in seconds, not minutes.

- Low and predictable fees – Critical for high-volume settlement use cases.

For banks settling large volumes of transactions, unpredictability is unacceptable. Networks with fluctuating fees or congestion risk introduce operational uncertainty. Solana’s architecture, which prioritizes parallel processing and deterministic execution, aligns more closely with institutional requirements than earlier-generation blockchains.

Importantly, Visa is not positioning Solana as a speculative asset play. Solana functions here as payment infrastructure, comparable to high-speed clearing rails rather than an investment vehicle.

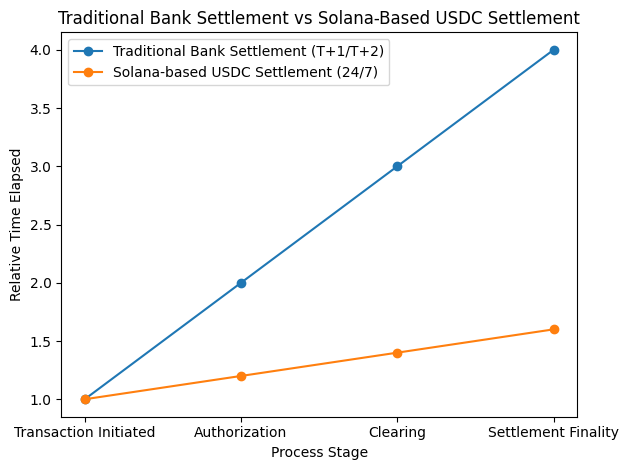

Title: Traditional Bank Settlement vs. Solana-Based USDC Settlement

Description: Diagram comparing T+1/T+2 bank settlement cycles with 24/7 on-chain settlement on Solana

3. 24/7 Settlement: Breaking Free from Banking Hours

One of the most transformative aspects of this initiative is the move to continuous settlement. Traditional interbank settlement systems are constrained by business hours, weekends, and holidays. Even in digital banking, final settlement often pauses outside predefined windows.

With USDC settlement on Solana, Visa enables seven-day-a-week, near-real-time settlement. For banks, this has several implications:

- Reduced liquidity buffers, as funds no longer remain trapped in transit.

- Improved treasury accuracy and cash flow forecasting.

- Faster reconciliation and lower operational risk.

In markets where capital efficiency directly impacts profitability, these improvements are not marginal—they are structural.

4. Early Adoption: Cross River Bank and Lead Bank

Visa confirmed that Cross River Bank and Lead Bank are already live with USDC settlement on Solana. Both institutions are known for their fintech partnerships and willingness to adopt emerging infrastructure earlier than traditional tier-one banks.

Their participation signals two important points:

- The system is operational, not theoretical.

- Regulatory and compliance hurdles have been sufficiently addressed to allow real bank usage.

Visa has stated its intention to expand availability to additional U.S. financial institutions by 2026, suggesting a phased but deliberate rollout strategy.

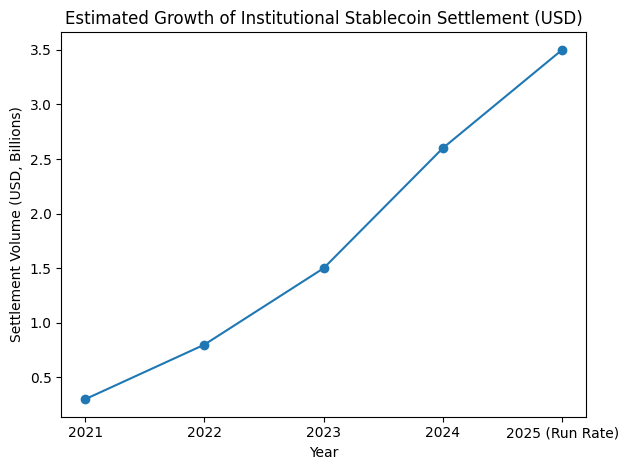

5. Market Context: Stablecoins Reach $3.5 Billion Annual Run Rate

Visa disclosed that stablecoin settlement volumes across its network have reached an annualized run rate of $3.5 billion. While this figure is modest compared to Visa’s overall transaction volume, its significance lies elsewhere.

Stablecoin payments are growing without consumer incentives or speculative hype. Growth is driven by operational demand from businesses and financial institutions seeking:

- Faster settlement

- Lower cross-border friction

- Programmable payment logic

This aligns with broader global trends. Across Latin America, Europe, Asia-Pacific, and CEMEA regions, stablecoins are increasingly used for treasury management, remittances, and B2B settlement.

Title: Estimated Growth of Institutional Stablecoin Settlement (USD)

Description: Line chart showing growth from pilot phase to $3.5B annualized run rate

6. Visa’s Broader Vision: Programmable Money for Banks

Rubail Birwadker, Visa’s Global Head of Growth Products and Strategic Partnerships, emphasized that banks are no longer interested in experimentation. What they want are production-ready tools that integrate with existing financial operations.

Stablecoins enable features that traditional payment rails struggle to support:

- Atomic settlement

- Conditional payments

- Automated reconciliation

- On-chain auditability

When combined with Visa’s global acceptance network, these features turn stablecoins into programmable money for regulated finance, not a parallel system competing with banks.

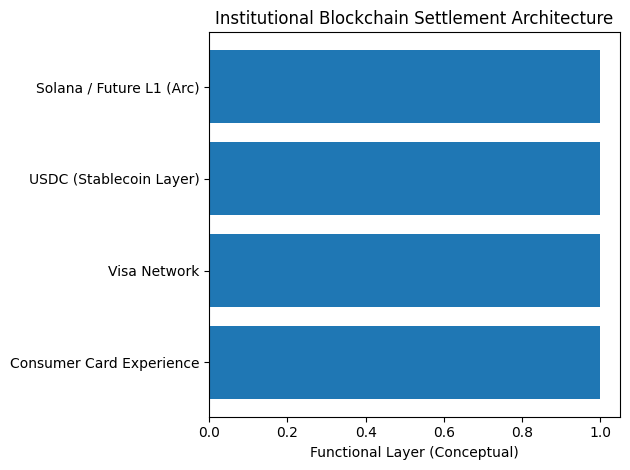

7. Beyond Solana: The Emerging Role of “Arc”

While Solana currently serves as Visa’s primary network for U.S. stablecoin settlement, Visa is also closely watching Arc, a new Layer-1 blockchain being designed in collaboration with Circle.

Arc’s public testnet already includes over 100 partners, including Visa, Mastercard, Goldman Sachs, and BlackRock. Its stated goal is to support large-scale commercial activity with compliance, performance, and reliability as first-class priorities.

This signals an important strategic insight: the future of institutional crypto payments is likely multi-network, with different blockchains optimized for different settlement and compliance requirements.

Title: Institutional Blockchain Stack: Visa, Stablecoins, and Settlement Networks

Description: Layered architecture diagram showing Visa network, USDC, Solana, and future L1s like Arc

8. Implications for Crypto Investors and Builders

For readers seeking new crypto assets, revenue opportunities, or practical blockchain applications, Visa’s move carries several implications:

- Infrastructure tokens matter: Blockchains used for real settlement gain long-term relevance beyond speculation.

- Stablecoins are not “boring”: They are becoming core financial primitives.

- Enterprise adoption follows reliability, not hype.

- Interoperability and compliance will define winners in institutional crypto.

Solana’s role here is especially notable. While often associated with DeFi and consumer apps, this use case positions Solana as serious financial infrastructure.

Conclusion: Stablecoins as the Missing Link Between Banks and Blockchain

Visa’s launch of USDC settlement on Solana marks a pivotal moment in the evolution of digital payments. It demonstrates that stablecoins are no longer peripheral tools but are becoming embedded in the core operations of regulated financial institutions.

By preserving the familiar card experience while transforming the settlement layer, Visa has created a model that banks can adopt without friction. Continuous settlement, programmable money, and blockchain-native efficiency are no longer theoretical advantages—they are live, measurable, and expanding.

As Visa continues to scale this system and explore new networks like Arc, the boundary between traditional finance and blockchain will continue to blur. For investors, builders, and institutions alike, this shift signals that the next phase of crypto adoption will be driven not by speculation, but by infrastructure.