Main Points :

- The Marshall Islands has become the first country in the world to complete a national, on-chain Universal Basic Income (UBI) payment using blockchain technology.

- Quarterly UBI payments of approximately $200 per citizen are distributed through multiple channels, including a government-backed digital wallet on the Stellar blockchain.

- The program modernizes a long-standing welfare system funded by a $1.3 billion sovereign trust, originally established as compensation for U.S. nuclear testing.

- Despite the technical success, actual adoption of blockchain wallets remains extremely low, highlighting real-world frictions in digital transformation.

- This initiative provides a practical, government-scale use case for blockchain, offering lessons for CBDCs, stablecoins, and digital public infrastructure worldwide.

1. Introduction: A Small Nation, a Global First

In the global debate over Universal Basic Income (UBI), discussions often remain theoretical—centered on fiscal sustainability, labor incentives, or political feasibility. The Marshall Islands, a Pacific island nation with a population of approximately 42,000, has quietly moved beyond theory. It has implemented and completed the world’s first nationwide, blockchain-based UBI distribution, marking a historic milestone in both social policy and digital finance.

Unlike pilot programs or city-level experiments seen elsewhere, this initiative operates at the sovereign state level. The Marshall Islands government has not merely tested blockchain payments but has integrated them directly into an existing national welfare system. This makes the program a rare convergence of public finance, distributed ledger technology, and social safety policy.

For readers interested in new crypto assets, alternative revenue models, and practical blockchain applications, this case provides a uniquely grounded example—one rooted not in speculation, but in governance.

2. From Physical Cash to On-Chain Payments

2.1 The Legacy UBI Framework

The Marshall Islands’ UBI program is not new in concept. For decades, citizens have received periodic payments under an initiative known as Economic Net Resource Allocation (ENRA). These payments are funded by a sovereign trust established through agreements with the United States as compensation for nuclear testing conducted during the mid-20th century.

Historically, these distributions were cumbersome. Physical cash deliveries and manual processes posed logistical challenges, especially given the country’s geography: dozens of remote islands spread across vast ocean distances. Payments were slow, costly, and vulnerable to inefficiencies.

2.2 Digital Transformation via Blockchain

In collaboration with the Stellar Development Foundation and Crossmint, the Ministry of Finance redesigned the system. The result is a hybrid distribution model that allows citizens to receive their quarterly UBI via:

- Bank transfer

- Paper check

- A government-supported digital wallet operating on the Stellar blockchain

The blockchain component uses a U.S. Treasury-backed sovereign digital instrument, commonly referred to as USDM1, issued and managed on-chain. This marks the first time a national government has executed recurring welfare payments directly on a public blockchain.

3. The Financial Structure Behind the Program

3.1 Funding and Sustainability

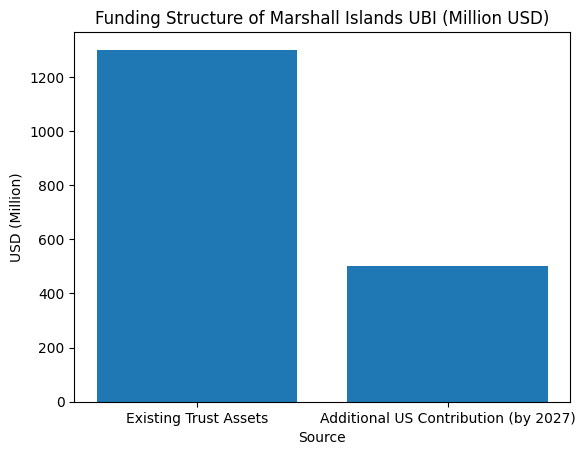

The UBI payments—approximately $200 per citizen per quarter—are backed by a sovereign trust valued at over $1.3 billion. Furthermore, an additional $500 million in U.S. contributions is scheduled to be injected into the fund by 2027.

This means the Marshall Islands’ UBI is not deficit-financed nor inflationary by design. Instead, it functions more like a dividend from a national endowment, making it structurally different from many UBI proposals discussed in larger economies.

3.2 Transparency and Auditability

By introducing blockchain settlement, the government gains:

- Immutable transaction records

- Real-time auditability

- Reduced reconciliation and distribution costs

From a public-sector accounting perspective, this represents a meaningful step toward verifiable, tamper-resistant welfare administration—a concept increasingly relevant as governments explore CBDCs and tokenized treasuries.

4. Blockchain as a Social Safety Net Infrastructure

Finance Minister David Paul has described the program as a modern “social safety net”, explicitly designed to protect citizens amid rising living costs and population decline. Unlike traditional welfare systems that require means testing or behavioral compliance, this UBI is unconditional and universal, reinforcing its role as a stabilizing economic baseline.

Academic observers have taken note. Dr. Huy Pham, head of the crypto-fintech unit at RMIT University, has described the initiative as the first full national deployment of a UBI program on blockchain infrastructure, rather than a limited pilot.

This distinction is critical. Many blockchain welfare experiments elsewhere rely on NGOs, municipal governments, or donor funding. The Marshall Islands program, by contrast, is state-backed, sovereign, and recurring.

5. Adoption Reality: Technology vs. Human Behavior

5.1 The Adoption Gap

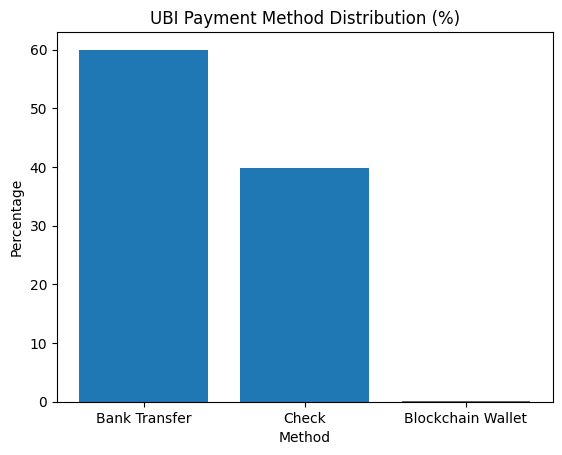

Despite the technical success, early data reveals a striking gap between availability and usage. In the first round of payments:

- Nearly 60% of funds were distributed via bank transfers

- Most of the remainder was paid through paper checks

- Only two individuals chose to receive funds through the blockchain-based digital wallet

This outcome underscores a recurring theme in fintech and crypto adoption: infrastructure alone does not guarantee behavioral change.

5.2 Structural and Cultural Constraints

Several factors explain this low uptake:

- Limited banking and internet infrastructure across remote islands

- Strong familiarity and trust in traditional payment methods

- Low smartphone penetration in certain regions

- Minimal perceived advantage for citizens who already receive funds reliably through banks or checks

Rather than a failure, this reality provides valuable insight. Blockchain can coexist with legacy systems, but forced digitalization risks exclusion—a lesson highly relevant for emerging-market fintech deployments.

6. Broader Implications for Crypto and Digital Assets

6.1 Beyond Speculation: A Sovereign Use Case

For crypto-native readers, the Marshall Islands case reframes blockchain as public infrastructure, not merely a speculative asset class. It demonstrates how distributed ledgers can:

- Reduce administrative friction

- Improve fiscal transparency

- Enable programmable public finance

This aligns with broader trends, including:

- Stablecoin-based remittances

- Tokenized government bonds

- Blockchain-powered aid disbursement

6.2 Lessons for CBDCs and Digital Fiat

While many central banks remain cautious about retail CBDCs, this initiative offers a pragmatic alternative path: deploying blockchain rails for specific use cases (such as welfare payments) without fully replacing fiat systems.

In that sense, the Marshall Islands model may be more immediately replicable than nationwide CBDCs—particularly in smaller economies or special-purpose public programs.

7. Where This Model Could Go Next

Future iterations of the program could include:

- Gradual incentives for digital wallet adoption

- Integration with mobile payments and merchant acceptance

- Smart-contract-based reporting and compliance automation

- Cross-border aid and remittance interoperability

However, the government’s cautious, opt-in approach suggests a key philosophical stance: technology should serve citizens, not coerce them.

8. Conclusion: A Quiet but Profound Precedent

The Marshall Islands’ blockchain-based UBI may not have captured global headlines, but its significance is profound. It is the first demonstration that blockchain can operate as a sovereign-grade payment system for social welfare, not in theory, but in production.

For policymakers, it offers a blueprint. For crypto builders, it provides validation. And for investors and practitioners seeking real-world blockchain utility, it stands as a reminder that the most transformative use cases often emerge far from major financial centers.

This is not the end of the UBI debate—but it may well be the beginning of a new chapter in digital public finance.