Main Points :

- Japan’s Financial Services Agency (FSA) has released draft Cabinet Orders and Cabinet Office Ordinances to introduce a registration system for crypto-asset and stablecoin intermediaries, including “broker-only” businesses.

- The move expands regulatory oversight beyond exchanges to include platforms, apps, wallets, and payment-facing services that merely intermediate transactions.

- The reform is grounded in amendments to the Payment Services Act, while a broader migration of crypto regulation toward the Financial Instruments and Exchange Act (FIEA) is now officially underway.

- These changes are closely linked to the emergence of Japanese yen–denominated stablecoins, institutional participation, and real-world payment use cases.

- For builders and investors, the new framework reshapes compliance costs, business models, and long-term revenue opportunities in Japan’s Web3 ecosystem.

1. Japan FSA Publishes Draft Ordinances for Crypto Intermediary Regulation

On December 16, 2025, Japan’s Financial Services Agency (FSA) announced a decisive step toward tightening oversight of the crypto-asset and stablecoin market by publishing draft Cabinet Orders and Cabinet Office Ordinances. These drafts propose a mandatory registration regime for businesses that intermediate crypto-asset or stablecoin transactions, even when they do not directly execute trades or custody assets.

Public comments are being accepted until January 19, 2026 (12:00 PM JST), after which the FSA plans to finalize and promulgate the revised regulations.

What makes this announcement particularly significant is its scope. Historically, Japanese regulation focused on crypto-asset exchange operators—entities that directly handle customer funds or execute trades. The new proposal explicitly targets intermediaries: companies that connect users to registered exchanges or electronic payment instrument operators, provide transaction routing, or act as interface layers.

Once implemented, these intermediaries will fall under direct FSA supervision, marking a substantial expansion of Japan’s crypto regulatory perimeter.

2. A New Legal Category Under the Amended Payment Services Act

2.1 Creation of the Intermediary Business Category

The regulatory changes stem from amendments to the Payment Services Act, enacted in June 2025. These amendments introduced a new legal category known collectively as:

Electronic Payment Instruments and Crypto-Asset Service Intermediary Businesses

Under the draft Cabinet Office Ordinance, this category includes entities that, upon委託 (delegation) from registered operators, only mediate transactions involving:

- Crypto-assets (e.g., BTC, ETH), or

- Electronic payment instruments, primarily stablecoins.

Crucially, the law does not require intermediaries to hold customer assets or execute trades directly to fall under regulation. The mere act of mediation—such as referral, transaction initiation, or UI-layer facilitation—is sufficient.

2.2 Registration Obligations and Disclosure Requirements

Intermediaries must:

- Register with the FSA prior to commencing operations.

- Clearly disclose their business scope, operational structure, and partnered registered operators.

- If partnered with multiple operators, explicitly define liability allocation in the event of customer loss or damage.

This reflects the FSA’s intention to eliminate ambiguity around responsibility in increasingly modular Web3 service stacks.

3. Compliance Duties: From Risk Disclosure to Recordkeeping

Once registered, intermediary businesses will be subject to obligations comparable—though not identical—to those imposed on exchanges.

Key duties include:

- Risk explanation and user disclosure obligations.

- Prohibitions against conflicts of interest and misleading conduct.

- Requirements to create and retain transaction-related records.

Although intermediaries may not custody funds, the FSA views their role as critical to consumer decision-making. As such, the regulatory philosophy is clear: influence equals responsibility.

This approach aligns Japan with emerging global standards that treat front-end platforms and aggregators as de facto financial actors.

4. Regulation of “Broker-Only” Businesses: Closing a Longstanding Gap

One of the most consequential aspects of the proposal is its explicit inclusion of broker-only or mediation-only operators.

Until now, many Web3 businesses operated in a gray zone:

- Wallet apps that route trades to exchanges

- Payment apps that initiate stablecoin transfers

- UI platforms that aggregate liquidity or pricing

Under the new framework, these entities can no longer claim to be “unregulated tech providers.” From the FSA’s perspective, user protection demands regulatory inclusion, regardless of whether assets are touched.

This change is expected to significantly affect:

- Startup compliance costs

- App-store approval strategies

- Revenue-sharing arrangements with licensed operators

5. Institutional Participation and the Scope of Permissible Activities

The draft ordinances also clarify what banks, insurance companies, and their subsidiaries may do within the intermediary framework.

By clearly defining permitted activities, the FSA is signaling that:

- Institutional participation in crypto and stablecoins is not only tolerated but anticipated.

- The boundaries of engagement must be legally precise to prevent systemic risk.

This clarity is especially important as traditional financial institutions explore stablecoin issuance, custody-adjacent services, and blockchain-based settlement systems.

6. The Stablecoin Catalyst: Why This Is Happening Now

6.1 Yen-Denominated Stablecoins Move Toward Reality

Behind the regulatory push lies a powerful catalyst: the real-world deployment of Japanese yen–denominated stablecoins.

Major financial groups are no longer merely experimenting. SBI Holdings, for example, has announced a partnership with blockchain firm Startale Group, aiming to issue a fully compliant yen stablecoin as early as Q1 FY2026.

Startale CEO Sota Watanabe has stated that yen stablecoins will play a core role in an increasingly on-chain global economy, extending far beyond domestic retail payments.

6.2 Regulatory Readiness as a Competitive Strategy

From a global perspective, Japan appears determined to avoid the regulatory lag that has plagued other jurisdictions. By preemptively regulating intermediaries, the FSA is:

- Reducing legal uncertainty for enterprises.

- Creating a predictable environment for long-term investment.

- Positioning Japan as a stable, institution-friendly Web3 hub.

7. Toward the Financial Instruments and Exchange Act (FIEA)

7.1 Formal Decision to Migrate Crypto Regulation

On December 10, 2025, the FSA’s Financial System Council working group published its final report on crypto regulation reform. The report confirms Japan’s intention to migrate crypto-asset regulation from the Payment Services Act to the Financial Instruments and Exchange Act (FIEA).

This transition will introduce:

- Insider trading prohibitions

- Market manipulation rules

- Enhanced investor protection standards

7.2 Conditional Permission for Bank and Insurer Holdings

The report also envisions conditional permission for banks and insurance companies to hold crypto-assets, subject to risk controls.

Taken together, these measures represent a structural reclassification of crypto—from a payment-like instrument to a financial investment product under Japan’s core securities law.

8. Implications for Builders, Investors, and New Revenue Models

For entrepreneurs and investors seeking new opportunities, the message is nuanced but clear:

- Compliance-first models will gain durability and institutional trust.

- Revenue opportunities will shift toward regulated intermediation, infrastructure, and B2B enablement.

- Marginal, regulation-averse projects will face increasing barriers.

At the same time, regulatory clarity unlocks:

- Stablecoin-based payment flows

- Cross-border settlement services

- Tokenized asset platforms aligned with traditional finance

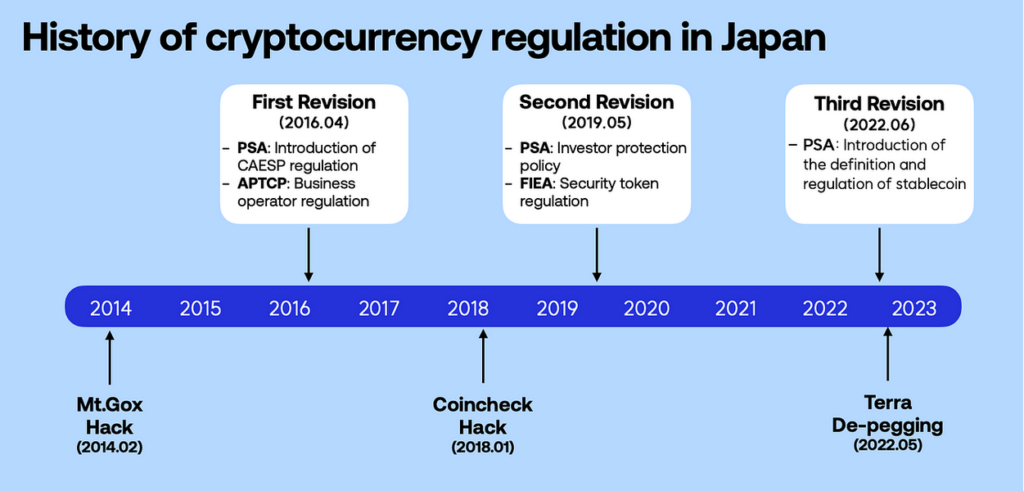

9. Visual Overview of the Regulatory Shift

Evolution of Japan’s crypto regulatory framework—from exchange-centric oversight to intermediary registration and FIEA migration.

Conclusion: Japan’s Quiet but Profound Web3 Reset

Japan’s move to regulate crypto and stablecoin intermediaries is not a headline-grabbing ban or endorsement. Instead, it represents something more enduring: institutional normalization.

By extending oversight to intermediaries, aligning stablecoins with real-world finance, and preparing a transition to the Financial Instruments and Exchange Act, the FSA is laying the groundwork for a mature, compliant, and globally integrated Web3 ecosystem.

For those searching for the next generation of crypto assets, revenue models, and practical blockchain applications, Japan’s evolving framework may prove less restrictive than it is strategically enabling.