Main Points :

- The U.S. House Financial Services Committee has concluded that the Biden administration coordinated an informal yet systemic effort to cut crypto companies off from banking services—now labeled Operation Choke Point 2.0.

- Regulatory actions by the Federal Reserve, FDIC, OCC, and SEC collectively discouraged banks from serving crypto companies, despite the lack of explicit legal prohibitions.

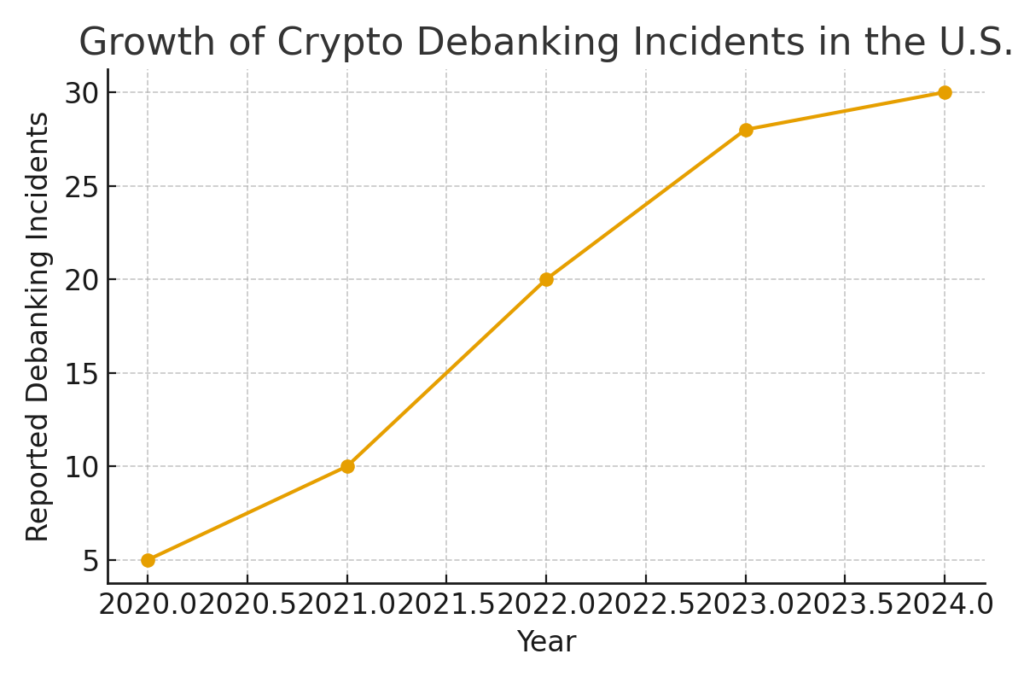

- At least 30 entities faced account closures, frozen funds, or refusal of services—impacting both corporations and individual founders.

- SEC enforcement-driven regulation and SAB 121 accounting rules significantly increased operational costs for crypto custodians.

- The debanking climate forced mining firms, exchanges, and blockchain developers to seek overseas banking or exit U.S. markets entirely.

- Congress is now drafting legislation guaranteeing fair access to banking, while U.S. policy shifts toward pro-innovation following Trump’s August 2025 executive order.

- For investors and builders searching for new crypto assets and real blockchain use cases, this shift may signal the start of a renewed growth phase, especially as global jurisdictions, from the EU to Asia, accelerate pro-crypto frameworks.

1. The Return of Political De-Risking: Why the U.S. House Declared “Operation Choke Point 2.0”

In its final investigative report titled “Operation Choke Point 2.0: President Biden’s Unbanking of Crypto”, the U.S. House Financial Services Committee concluded that federal regulators engaged in a coordinated—though unofficial—effort to deny crypto firms access to banking services.

While no formal law prohibited banks from servicing crypto clients, supervisors allegedly used ambiguous guidelines, heightened scrutiny, and informal communications to pressure financial institutions to avoid the sector entirely.

The committee documented at least 30 corporate and personal accounts closed without warning, with losses of operational continuity, delayed payroll, frozen tax payments, and disrupted energy contracts for mining operators.

This type of regulatory chokehold resembles the original Operation Choke Point (2013–2017) under the Obama administration, which targeted firearms dealers and payday lenders by labeling them “high-risk.” Although officially terminated in 2017, the committee argues that the playbook was revived and expanded, now aimed at digital assets.

2. Choke Point 1.0 vs. 2.0: What Has Changed?

The earlier version of Operation Choke Point pressured banks to sever ties with industries considered politically or socially undesirable. The new iteration differs mainly in scale and target:

| Aspect | Choke Point 1.0 | Choke Point 2.0 |

|---|---|---|

| Target Sectors | Guns, payday lending | Crypto exchanges, miners, DeFi developers |

| Regulatory Tools Used | Risk categorization | Multi-agency pre-approval, informal “pause letters,” accounting burdens |

| Impact | Account closures | Market-wide access freeze, migration of companies offshore |

Crypto, unlike past targets, is intertwined with global capital markets, making the banking restrictions significantly more disruptive.

3. Federal Reserve Actions: The “New Activity” Framework That Froze Crypto Banking

In 2022 and 2023, the Federal Reserve issued supervisory letters SR 22-6, SR 23-7, and SR 23-8, each adding compliance friction for banks interacting with digital assets:

- Banks must pre-notify regulators before engaging in any crypto activity.

- Stablecoin activities require advance supervisory approval.

- Crypto operations were classified broadly as “new activities,” subject to enhanced continual review.

Simultaneously, the Fed introduced a New Activities Supervision Program, placing crypto-serving banks under deeper scrutiny than any other sector.

Banks, fearing reputation risk and supervisory downgrades, began mass de-risking—cutting ties with crypto firms regardless of their compliance posture.

4. FDIC Pressure: The “Pause Letters” That Stopped Entire Product Lines

The FDIC reportedly sent informal “pause letters” to member banks beginning in 2023. These letters:

- Required banks to halt crypto-related business plans.

- Demanded large-scale submission of internal documents.

- Implied adverse supervisory consequences if institutions proceeded.

Because the instructions were non-public and non-binding on paper yet treated as authoritative in practice, they effectively froze banking innovation.

Former FDIC Acting Chair Martin Gruenberg confirmed that banks attempting to work with crypto clients “almost universally met resistance.”

5. OCC’s Administrative Overlays: Requiring Unusual Pre-Approvals

The Office of the Comptroller of the Currency (OCC) added another layer of difficulty by requiring individual supervisory “non-objection letters” for:

- Crypto custody services

- Stablecoin issuance/tethering

- Blockchain validation (node operations)

This reversed earlier Trump-era guidance that had permitted banks to experiment in these areas.

As a result, major national banks abandoned plans for digital asset divisions or significantly scaled back ambitions.

6. SEC Enforcement Dominance and SAB 121: Accounting as a Regulatory Weapon

Rather than proposing a transparent regulatory framework, the SEC relied heavily on enforcement actions. It filed major suits against:

- Coinbase

- Binance

- Kraken

- Ripple executives

- Multiple token issuers

SAB 121—an unexpected accounting bulletin—required crypto custodians to list customer assets on their balance sheets, drastically increasing capital requirements. Traditional banks immediately viewed crypto custody as economically unattractive.

This effectively shut the door for bank-grade crypto custodianship in the U.S.

7. Consequences: Sudden Account Closures Across the Ecosystem

Companies such as Marathon Digital, Strike, and multiple mining firms lost access to banking with 24–72 hours’ notice, even with $70M+ in balances.

Crypto founders—including Hayden Adams (Uniswap) and Brad Garlinghouse (Ripple)—reported personal account closures without explanation.

These disruptions:

- Interrupted payroll

- Blocked tax remittance

- Jeopardized power contracts

- Forced emergency asset relocation

Many companies relocated engineering teams abroad or established offshore banking relationships.

8. Market Impact: Short-Term Damage but Long-Term Growth Potential

The debanking wave created short-term liquidity risks but also reshaped global competitive dynamics:

Where Crypto Banking Flourished During U.S. Restrictions

- Europe (MiCA framework) — predictable licensing, stablecoin clarity

- Hong Kong — official banking channels for licensed virtual asset providers

- Singapore — strong institutional custody market

- UAE — zero-tax Web3 hubs attracting U.S. engineering talent

As U.S. federal pressure grew, more capital and projects flowed to these jurisdictions.

9. The Policy Reversal: Congress and the Trump Administration Move Toward Fair Access

The investigative report prompted bipartisan discussions about a Fair Banking Services Guarantee Act, which would prohibit politically motivated debanking.

In August 2025, President Trump signed an executive order ensuring that crypto firms and lawful industries cannot be denied banking services solely for political reasons.

This marks a significant pivot toward financial innovation, reversing years of regulatory hostility.

10. What This Means for Investors Seeking New Crypto Assets & Income Opportunities

For market participants evaluating new assets or blockchain applications, the policy shift may unlock:

- More U.S.-based stablecoin infrastructure (backed by compliant banks)

- Regulated crypto custody offerings from major financial institutions

- Growth in tokenized U.S. treasury markets (already surpassing $1.5B globally)

- Increased institutional adoption of Bitcoin and Ether through ETF structures

- Re-entry of U.S. banks into liquidity provision for exchanges

Projects previously hindered by banking limitations—such as real-world asset tokenization (RWA), high-volume payment rails, and enterprise-grade DeFi—may accelerate rapidly.

Conclusion: The Choke Point Era Is Ending—And a New Growth Cycle May Begin

Operation Choke Point 2.0 illustrates how regulatory ambiguity—not legislation—can reshape entire industries. By indirectly pressuring banks, U.S. regulators temporarily slowed crypto innovation, pushing capital offshore and undermining domestic competitiveness.

However, as Congress pursues fair-access rules and the executive branch signals pro-innovation support, the outlook is shifting decisively.

For investors and builders searching for new crypto assets, revenue opportunities, and real-world blockchain utility, the renewed banking openness may mark the beginning of a major expansion phase—with clearer regulations, stronger institutions, and more stable infrastructure than ever before.