Main Points :

- The U.S. SEC has effectively blocked new 3x–5x leveraged ETFs on stocks, commodities, and cryptocurrencies by sending warning letters to nine major issuers, including Direxion, ProShares, Tidal, and Volatility Shares.

- The regulator says these products breach a 200% (2x) value-at-risk limit, raising concerns that risk at the fund level can exceed the fund’s assets and confuse retail investors.

- Leveraged ETFs have exploded in popularity since the pandemic, with assets climbing to roughly $162 billion and some estimates putting U.S. leveraged ETF AUM at around $239 billion by Q3 2025.

- Recent blow-ups, including a 3x short AMD ETF in Europe that went to zero in one day and 2x MicroStrategy-linked ETFs that lost around 85% in 2025, show how quickly leveraged products can destroy capital when volatility spikes.

- For crypto traders, the SEC decision shifts extreme leverage back to offshore venues and on-chain perps, while U.S. markets will likely focus on spot ETFs, modest leverage (≤2x), options overlays, and structured yield products.

- Builders who understand this regulatory turn can monetize safer leverage, create compliant products for institutions, and design infrastructure that treats leverage as a controlled feature, not a marketing gimmick.

1. What Just Happened: The SEC Slams the Brakes on Ultra-Leveraged ETFs

On 3 December 2025, the U.S. Securities and Exchange Commission (SEC) quietly did something that could reshape the entire leverage business in ETFs — including those linked to cryptocurrencies.

The SEC’s investment-management staff issued nine nearly identical warning letters to some of the most aggressive ETF issuers in the U.S. market, including Direxion, ProShares, Tidal Financial, and Volatility Shares.

Those filings aimed to launch products offering three to five times the daily performance of underlying indexes and assets — not just equity benchmarks like the S&P 500, but also single stocks such as Tesla and Nvidia, and crypto assets like Bitcoin and Ether.

In the letters, the SEC stated that it is “concerned regarding the registration of exchange-traded funds that seek to provide more than 200% leveraged exposure” relative to their reference index or security.

That phrase is important: it effectively re-asserts a hard ceiling at 2x leverage for U.S.-listed ETFs, closing the door on the wave of 3x–5x proposals that had been building around both equities and crypto.

In response, some issuers have already withdrawn applications, including ProShares pulling several 3x crypto ETF filings.

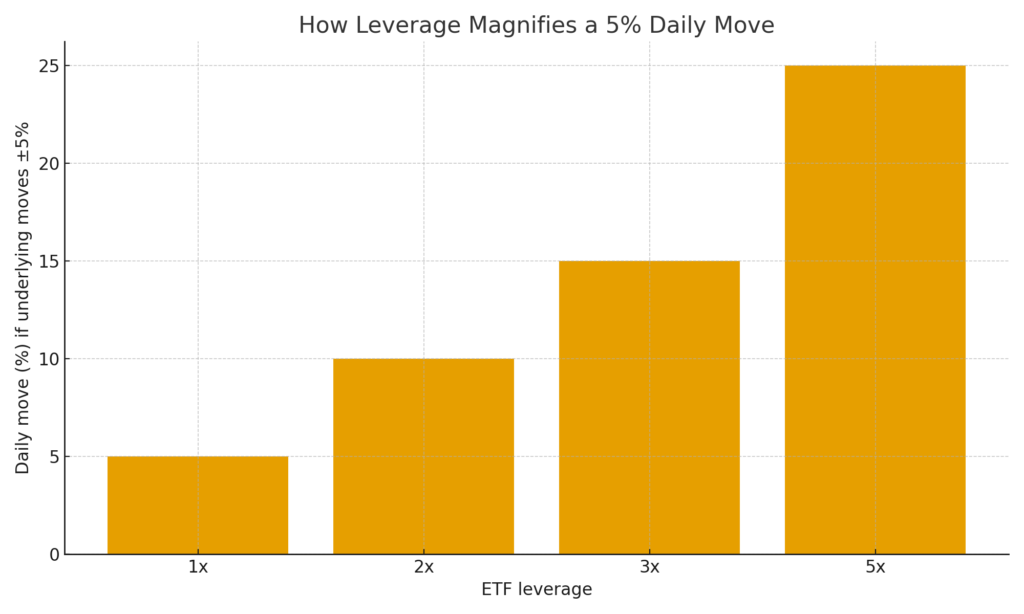

This chart visually explains how a simple 5% move in the underlying asset becomes 10%, 15%, or 25% in a 2x, 3x, or 5x ETF — in both directions.

2. How High-Leverage ETFs Work – and Why Regulators Are Nervous

Leveraged ETFs use derivatives such as swaps, futures, and options to target a multiple of an index’s daily return — for example, +200% or +300% of the S&P 500’s move, or +300% of Bitcoin’s daily change.

Key characteristics:

- Daily reset: The leverage target is rebalanced every day. Over multiple days, compounding can make performance diverge significantly from “simple” 2x or 3x scenarios.

- Path dependency: In volatile sideways markets, leveraged funds can bleed value even if the underlying asset goes nowhere over time.

- Derivatives-based: They introduce counterparty, margin, and liquidity risk, especially when underlying markets are stressed.

For regulators like the SEC, the problem is not just volatility; it is value-at-risk (VaR) at the fund level. Recent guidance effectively says that a registered ETF should not run VaR substantially above 200% of its reference benchmark, which many 3x–5x filings would likely violate.

At the same time, retail participation has exploded. According to Bloomberg and related analyses, global assets in leveraged ETFs have climbed to around $162 billion, up sharply since the pandemic. Other market data suggests that U.S.-listed leveraged ETFs alone manage roughly $239 billion, an all-time high, underscoring how deeply leverage has penetrated retail portfolios.

From the SEC’s perspective, this is a dangerous cocktail: complex derivative structures, extreme volatility, and massive retail flows into products many investors don’t fully understand.

3. Crypto-Linked Leveraged ETFs: From Growth Story to Regulatory Target

Crypto markets have been a natural home for leverage:

- Crypto spot and futures exchanges routinely offer 5x, 10x, or even 100x leverage.

- On-chain perpetuals and options have made it trivial for DeFi users to construct leveraged views with collateralized positions.

- The arrival of spot Bitcoin and Ether ETFs drew billions of dollars into regulated wrappers, setting the stage for more aggressive products.

On the ETF side, issuers began to file for 3x crypto products:

- 3x long Bitcoin

- 3x long Ether

- In some proposals, 3x Solana, 3x XRP, and others

A separate filing by Volatility Shares even targeted 5x exposure to Tesla, Nvidia, Bitcoin, and Ether — products that would have been among the most leveraged securities ever listed on a U.S. exchange.

The SEC’s new letters directly interrupt this pipeline. The message is clear: in the U.S. there will be no 5x crypto ETFs, and even 3x is now effectively frozen, at least under current rules.

4. When Leverage Blows Up: AMD and MicroStrategy as Case Studies

The SEC’s move is not happening in a vacuum. It comes after several very public blow-ups.

In Europe, GraniteShares launched a 3x short AMD ETF. When AMD shares suddenly surged, the fund’s value was effectively wiped out in a single session, forcing its closure. It was a textbook demonstration of how a single-stock inverse leveraged product can go to zero when the underlying rallies hard.

In the U.S., leveraged ETFs tied to MicroStrategy — the company led by Michael Saylor and known for its massive Bitcoin treasury — have been among the biggest casualties of the 2025 crypto slump. Reuters reports that 2x long MSTR ETFs lost about 85% of their value in 2025, as Bitcoin’s decline dragged the stock down more than 35%.

Figure 2 illustrates a simple scenario: if the underlying asset falls 50%, a 2x leveraged long ETF can essentially suffer a 100% loss in the same period, depending on the path of returns. This is simplified, but it captures the asymmetry regulators worry about.

These episodes give the SEC an easy narrative:

- Leverage amplifies downside,

- Path dependency confuses investors, and

- Retail traders often arrive late, buy high, and endure the worst of the drawdowns.

5. For Crypto Traders: What Does the Crackdown Actually Change?

If you’re a crypto-focused trader or product user, the practical consequences are nuanced:

- Spot crypto ETFs in the U.S. remain untouched.

Bitcoin and Ether spot ETFs are still operating and attracting large flows, even if they have recently seen outflows during market corrections. - Simple 2x ETFs are likely still acceptable.

Products that stay within the 200% VaR limit and use conservative derivatives structures are not the direct target of this new wave of letters. - 3x–5x U.S. products are effectively off the table.

Crypto traders who were hoping for listed 3x Bitcoin or 3x Solana ETFs on U.S. exchanges will need to reconsider: the SEC has signaled that such products simply won’t advance under current rules. - Offshore and on-chain markets will absorb the demand for extreme leverage.

Traders who insist on 5x and above will likely resort to:- Offshore ETFs and ETPs listed in jurisdictions with looser rules

- Perpetual futures on centralized exchanges

- DeFi protocols with synthetic leverage

From a risk officer’s perspective, that is a double-edged outcome. On one hand, U.S.-regulated exchanges become safer for retail. On the other hand, the riskiest behavior simply migrates to less transparent venues.

6. Opportunities: Where the Next Revenue Streams Can Emerge

For readers who are looking for new crypto assets, next revenue sources, and practical blockchain use cases, the crackdown does not mean “no more leverage.” Instead, it suggests a shift in where and how leverage will be packaged.

(1) Smarter, regulated leverage ≤2x

Issuers and product builders can still design:

- 2x long and short ETFs on Bitcoin, Ether, and large-cap crypto baskets.

- Options-overlay strategies (e.g., collars, covered calls) that enhance yield or shape payoff profiles without breaching VaR caps.

- Capital-efficient structured notes that reference spot ETFs but embed moderate leverage synthetically.

These can appeal not only to retail, but also to institutions and hedge funds that must operate under strict risk and reporting frameworks. Surveys already show that over half of hedge funds now hold some crypto exposure, typically small but growing, which suggests a fertile market for compliant leveraged beta.

(2) On-chain “controlled leverage” protocols

In DeFi, leverage is often provided by perpetual DEXs, lending markets, and structured vaults. The SEC’s stance may actually increase the attractiveness of:

- Vaults that cap effective leverage (for example, using delta-hedged options strategies or automated de-risking triggers).

- Tokenized risk tranches where junior tranches absorb losses and senior tranches collect more stable yield — a concept that can be implemented with transparent smart contracts and on-chain proof of reserves.

These structures can transform “leverage” into configurable, auditable risk rather than opaque derivatives plumbing.

(3) Infrastructure for regulatory-friendly leverage

For entrepreneurs and infrastructure builders, there is demand for:

- Reg-aware margin and risk engines that embed hard leverage caps, stress tests, and VaR calculations that mirror regulators’ expectations.

- Data and analytics platforms that help issuers, custodians, and brokers monitor leveraged exposure across on-chain and off-chain positions.

- Compliance-ready tokenization of ETF shares, collateral baskets, and structured products, allowing controlled leverage inside permissioned blockchain networks.

This is where “practical blockchain use” becomes real: blockchains can serve as audit rails for leverage, not just venues for speculation.

7. Strategic Takeaways for Builders and Long-Term Investors

From a macro perspective, several longer-term themes are emerging:

- Regulators are drawing a harder line between “beta with a twist” and “casino leverage.”

Spot ETFs, modest 2x products, and hedging overlays remain acceptable. Yet, 3x–5x daily leverage on volatile assets crosses a threshold the SEC is no longer comfortable with. - The boom in leveraged ETFs was a symptom of a broader risk-on regime.

With AUM in leveraged funds surging to the $162–239 billion range, the latest crackdown can be read as a policy response to years of aggressive retail risk-taking. - Crypto is no longer marginal — it is integrated into mainstream risk debates.

The fact that Bitcoin and Ether are explicitly mentioned in high-level regulatory letters about ETF risk shows how deeply digital assets are now embedded in the traditional financial system.

For long-term allocators, the key is to separate structural alpha from pure leverage. Spot ETFs, staking yields, basis trades, tokenization of real-world assets, and payment-rail use cases can all generate returns without 5x daily leverage. For builders, the opportunity is to monetize risk management, not just risk appetite.

8. Conclusion: Leverage Isn’t Dead — It’s Moving and Maturing

The SEC’s decision to block 3x–5x leveraged ETFs on stocks, commodities, and cryptocurrencies is not the end of leverage. It is a re-routing of where leverage lives:

- U.S.-listed ETFs will likely converge on spot, 1x, and 2x products, plus options and overlays.

- Extreme leverage will concentrate in offshore exchanges and on-chain derivatives, where sophisticated traders will continue to seek 5x–20x exposure.

- New business models will grow around reg-friendly leverage, risk analytics, and infrastructure that let institutions touch crypto beta with controlled downside.

For investors searching for new crypto assets and revenue streams, the message is simple:

- Don’t chase the most explosive leverage just because it disappears from U.S. ETFs.

- Instead, look at how leverage is structured, governed, and audited — that’s where sustainable opportunities will emerge.

And for builders working on exchanges, wallets, and tokenization platforms, this is a signal: the future belongs to transparent, controlled, and regulator-compatible leverage, not to ever-larger multipliers.