Main Points :

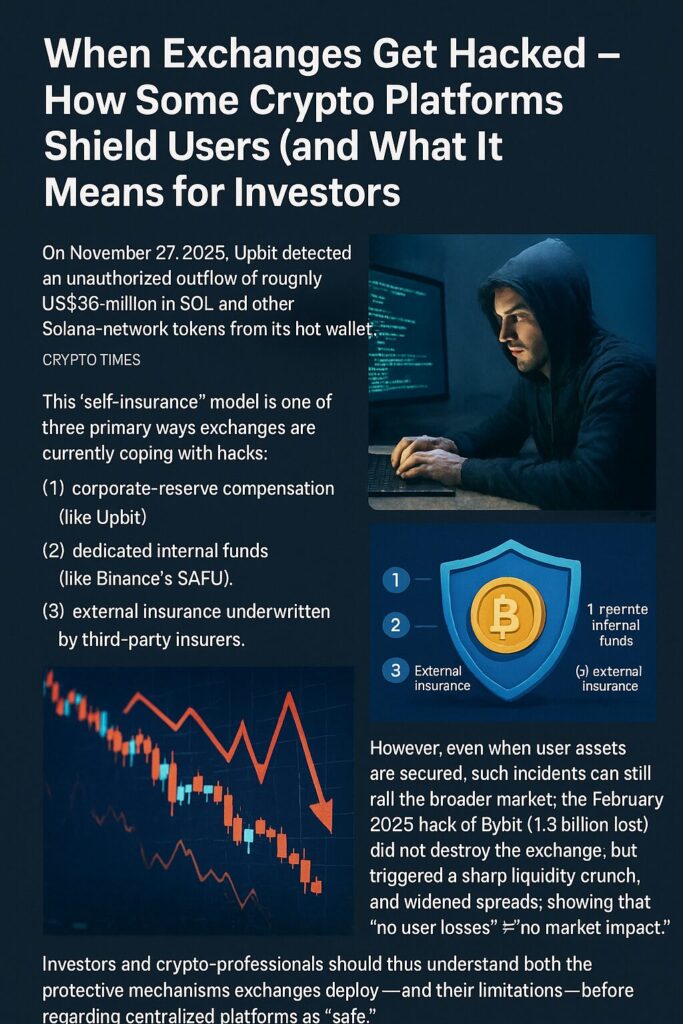

- On November 27, 2025, Upbit detected an unauthorized outflow of roughly US$36 million in SOL and other Solana-network tokens from its hot wallet.

- Within a few hours, Upbit pledged to fully compensate the lost assets from its corporate reserves, assuring that user funds would not be affected.

- This “self-insurance” model is one of three primary ways exchanges are currently coping with hacks: (1) corporate-reserve compensation (like Upbit), (2) dedicated internal funds (like Binance’s SAFU), and (3) external insurance underwritten by third-party insurers.

- However, even when user assets are secured, such incidents can still roil the broader market: the February 2025 hack of Bybit ($1.5 billion lost) did not destroy the exchange, but triggered a sharp liquidity crunch and widened spreads, showing that “no user losses” ≠ “no market impact.”

- Investors and crypto-professionals should thus understand both the protective mechanisms exchanges deploy — and their limitations — before regarding centralized platforms as “safe.”

1. The Upbit Hack — What Happened, What We Know

On November 27, 2025, Upbit, one of South Korea’s largest cryptocurrency exchanges, detected a suspicious outflow of crypto assets from its hot wallet. The assets in question — including SOL, USDC, and several other tokens on the Solana network — were transferred irregularly to external addresses. Estimates of the loss have hovered around US$36–38.5 million.

Responding within hours, Upbit swiftly halted withdrawals and deposits, initiated a full security audit, and moved remaining funds into cold wallets for safekeeping.

Finally, the exchange’s CEO announced that Upbit would absorb the entire loss using its corporate funds — meaning user holdings were unaffected.

This is not the first time Upbit has faced such a situation. In 2019, the exchange covered a hack that saw about US$50 million worth of ETH stolen, again compensating from its own coffers. The 2025 incident reaffirms that Upbit follows a “self-insurance” model of loss absorption.

While the immediate financial damage seems contained — and user trust may remain intact — questions linger about the root vulnerability. According to reports, the breach was tied to a flaw discovered in Upbit’s wallet infrastructure during a post-hack review.

2. Exchange Compensation Models — A Landscape of Three

In the wake of repeated hacks and rising regulatory scrutiny, many leading centralized exchanges have formalized insurance or compensation schemes. Broadly speaking, there are three models in use today.

Self-Insurance via Corporate Reserves

This is the model adopted by Upbit. The exchange uses its own balance sheet to absorb losses in case of hacks. The advantage is simplicity: no reliance on external insurance markets or third-party underwriters. But it also means that if a breach is large or frequent enough, the exchange’s financial stability could be at risk.

Dedicated Internal Funds (e.g., SAFU)

Another popular approach is to build a dedicated reserve fund specifically for user compensation. For example, Binance maintains a so-called Secure Asset Fund for Users (SAFU), reportedly holding funds as of 2025 to reimburse users in case of security incidents.

This approach allows exchanges to segregate “insurance capital” from operating funds, potentially making their financial health more resilient, and offering a clearer safety guarantee to users.

Third-Party Insurance by External Insurers

Some exchanges — particularly those operating under stricter regulatory regimes — purchase insurance from external insurers, similar to how traditional financial firms insure assets. This model can provide additional credibility and risk transfer. However, such insurance typically comes with limits (e.g., caps per incident or per user) and varying coverage scope.

3. Why Insurance ≠ Immunity: The Broader Market Impact

Even when exchanges successfully compensate users, the broader crypto market may still suffer. The February 2025 hack of Bybit — which lost an estimated US$1.5 billion in Ethereum — offers a stark example.

Despite the massive scale, Bybit reportedly continued operations, and user withdrawals were not halted. The exchange stressed that funds were protected and replenished quickly.

Nevertheless, the immediate aftermath saw liquidity evaporate, particularly for large trades. Spreads widened, slippage increased, and many participants rushed to other exchanges — highlighting a key truth: even well-capitalized insurance frameworks cannot fully prevent market disruption when confidence falters.

For investors, this means that “your crypto is safe” doesn’t always equate to “your ability to trade or exit positions is unaffected.”

4. What This Means for Crypto Investors and Practitioners

For those actively hunting for new crypto investments, new tokens, or practical blockchain applications — the kind of readers you’re part of — this landscape has several implications:

- Understand the exchange’s insurance model. Don’t just look at reputation: dig into whether the exchange uses corporate reserves, dedicated funds, or third-party insurance. That affects both security and your risk exposure.

- Diversify and keep control over critical assets. For valuable holdings — especially long-term or strategic ones — consider self-custody (hardware wallets, cold wallets) rather than leaving everything on exchanges. Relying on exchange promises alone may be risky.

- Prepare for market instability, not just asset safety. Even if a hack doesn’t cost users a cent, market liquidity shock or volatility can affect your ability to trade, exit, or deploy assets — especially relevant if you’re engaging in DeFi, staking, or cross-chain swaps.

- Advocate for better industry standards. As hacks continue, exchanges that rely on opaque internal funds could face solvency issues; external insurance and transparency (e.g., audits, proof-of-reserves) should become standard.

5. Context: 2025 Crypto-Exchanges Landscape

As centralized exchanges grow in scale and activity through 2025, with high trading volumes and expanding product offerings, the importance of robust security and compensation frameworks has never been greater.

Some firms like Binance — with its SAFU fund, cold-storage strategy, and regular audits — are increasingly regarded as safer for high-volume traders needing deep liquidity and broad crypto access.

Others, like Upbit, demonstrate that even for tokens beyond BTC/ETH — e.g., SOL and Solana-network tokens — exchanges can still uphold strong risk-management and quick response to protect users.

For developers and practitioners (like you, working on wallets, cross-chain swap flows, blockchain-payment integrations), this reinforces the prudence of designing systems assuming that centralized exchanges are not a safe substitute for custody.

6. Infographic: Visualization of Hacks & Insurance Models

Caption: A visual breakdown of recent major exchange hacks (Upbit and Bybit) and a schematic of the three main insurance/compensation models used by centralized exchanges.

Conclusion

The recent 2025 hack of Upbit underscores a shifting paradigm in centralized cryptocurrency exchanges: hacks and breaches may still occur, but a growing number of platforms are equipped to absorb losses, compensate users, and avoid bankruptcy. The “self-insurance” approach taken by Upbit — following earlier precedents — shows that corporate responsibility and timely action can safeguard user assets.

Yet, this does not equate to a risk-free ecosystem. As evidenced by the massive hack at Bybit earlier in 2025, even when user funds are preserved, the ripple effects on liquidity, market stability, and investor confidence can be profound. For crypto investors, developers, and practitioners seeking to build on blockchain technology — whether through token investments, wallet development, DeFi protocols, or payments infrastructure — this landscape demands vigilance.

Users should treat exchange-held assets as what they are: exposure to counterparty risk, market risk, and operational risk. For critical holdings or long-term strategic assets, self-custody — or at least diversification across custody types — remains a cornerstone of prudent asset management. Meanwhile, the industry needs stronger standards: transparent audits, external insurance coverage, and regulatory frameworks to elevate trust.

For those looking to discover new assets, build real-world blockchain applications, or ride the next wave of crypto innovation, understanding the mechanisms — and limitations — of exchange insurance is as essential as picking promising tokens or protocols.