Main Points :

- Traditional banks such as JP Morgan are accelerating “debanking” actions against crypto-related companies due to AML/CFT pressure and regulatory ambiguity.

- The impact is industry-wide, affecting not only startups but mature companies like ShapeShift.

- Banking exclusion threatens the fundamental operability of crypto businesses—salary payments, tax remittance, and treasury operations.

- The trend is pushing the crypto ecosystem toward decentralized infrastructures (DeFi) and regulated digital alternatives (CBDCs).

- Current global regulatory trends show fragmentation: the U.S. increasing enforcement, Europe moving toward MiCA clarity, Asia pushing CBDC pilots.

- The long-term consequence may be the rise of self-sovereign financial rails that operate parallel to or independent from traditional banks.

1. Introduction: A New Wave of Financial Exclusion

Reports that JP Morgan Chase has been mass-closing accounts belonging to crypto industry participants highlight a renewed wave of institutional hostility toward the sector. This “debanking pressure” reflects a persistent structural problem: crypto businesses rely on traditional banking infrastructure for fiat operations, while banks perceive them as disproportionately risky customers.

This article synthesizes the findings from the referenced Japanese report, expands them with updated global developments, and analyzes why the conflict between crypto firms and traditional banks is intensifying. For entrepreneurs exploring new crypto assets, income opportunities, or blockchain utilities, understanding these dynamics is crucial for navigating the next phase of industry evolution.

2. Structural Reasons Behind Debanking: AML and CFT Overweighting

At the core of the debanking trend lies one dominant driver: regulatory pressure. Traditional financial institutions are required to comply with strict Anti-Money Laundering (AML) and Counter-Terrorism Financing (CFT) policies. Because crypto transactions are often pseudonymous and borderless, banks perceive even compliant crypto companies as high-risk clients.

This risk-weighted calculus drives institutions like JP Morgan to choose the least-risky path: eliminating exposure entirely.

Even well-established firms such as ShapeShift have been affected, demonstrating that banks are not differentiating between small startups and large reputable operators. For many banks, the “crypto category” itself is the risk.

This widening exclusion reflects systemic uncertainty. In environments where regulation remains ambiguous—such as the United States—banks have stronger incentives to avoid liabilities than to support the industry.

3. Industry-Wide Impact: From Daily Operations to Market Growth

The consequences of debanking extend beyond operational inconvenience. When a crypto company loses access to fiat banking, its core functions are immediately compromised, including:

- salary payments

- corporate tax remittance

- vendor and partner payments

- fiat liquidity management

- treasury settlement

This disruption affects not only business owners but also employees, investors, and users who depend on the stability of the service provider.

Widespread banking exclusion also reduces competition, raises service costs, and increases market consolidation. Ironically, the more banks de-risk by cutting ties with crypto, the more crypto businesses cluster around fewer friendly institutions—those that then take on disproportionately concentrated compliance risk.

In aggregate, debanking acts as a friction tax on innovation.

4. Global Trends: The Regulatory Landscape in 2024–2025

Recent geopolitical and regulatory developments further contextualize JP Morgan’s actions:

United States: Enforcement Dominance

- The U.S. has intensified enforcement actions against crypto platforms.

- Banks face unclear expectations due to inconsistent federal and state rules.

- The lack of explicit guidance encourages pre-emptive risk avoidance.

European Union: MiCA Clarity

- The EU’s MiCA framework (Markets in Crypto-Assets) offers more predictable compliance, reducing the likelihood of blanket debanking.

- European banks have begun exploring structured crypto services rather than outright avoidance.

Asia: CBDC Acceleration

- China, Singapore, and Japan are accelerating central bank digital currency (CBDC) pilots.

- These pilots are intended partly to create safe, trackable digital infrastructure that can reduce AML/CFT uncertainty.

Latin America: High Adoption + Weak Banking Integration

- Crypto adoption is high due to inflation and currency instability.

- However, banks remain conservative, pushing users toward peer-to-peer alternatives.

Together, these trends suggest a divided world: one side builds clarity, while the other delays regulation and relies on debanking to manage uncertainty.

5. The Strategic Pivot: Why DeFi and CBDCs Are Becoming Critical Infrastructure

The article highlights a crucial insight: debanking pressure does not weaken crypto—it accelerates its evolution.

DeFi as a Shield Against Exclusion

Decentralized Finance provides financial services—swaps, lending, liquidity pools—without banks. If traditional institutions shut their doors, DeFi becomes the default infrastructure for:

- treasury management

- trading

- liquidity operations

- cross-border settlement

DeFi cannot currently replace all fiat-related operations, but its share is growing quickly.

CBDCs as a Middle Path

CBDCs could allow crypto firms to access regulated digital cash rails without depending on commercial banks.

If CBDCs integrate with blockchain-friendly APIs, they may become the compliance-first alternative to conventional fiat accounts.

The Long-Term Outcome

Debanking may unintentionally speed up the migration from centralized banking toward:

- decentralized liquidity (DeFi)

- state-backed digital currency (CBDC)

- tokenized real-world assets

- programmable and auditable financial flows

Traditional finance is pushing crypto toward autonomy.

6. Recent Market Signals Supporting This Trend

Outside the JP Morgan news, several developments in 2024–2025 reinforce the structural shift:

Institutional Adoption Continues

Despite debanking, BlackRock, Fidelity, and other asset managers continue to expand digital asset portfolios.

On-chain Treasury Operations

Global fintech companies increasingly settle treasury movements on-chain using USDC and other regulated stablecoins.

Bank-Grade Blockchain Networks

Some banks now explore permissioned blockchains for interbank settlement—indicating that crypto rails are useful even to institutions that reject crypto clients.

Growth in Layer-2 and Cross-Chain Protocols

The reduction of gas costs and the rise of interoperability solutions make DeFi more viable for corporate flows.

Together, these signals indicate that crypto’s financial infrastructure is maturing faster than banks can adjust.

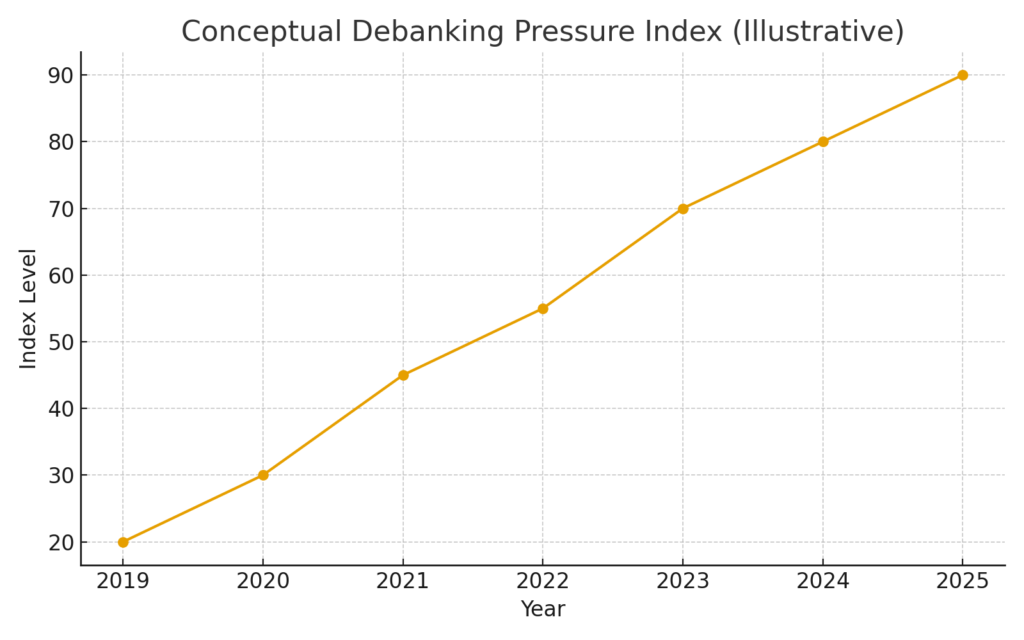

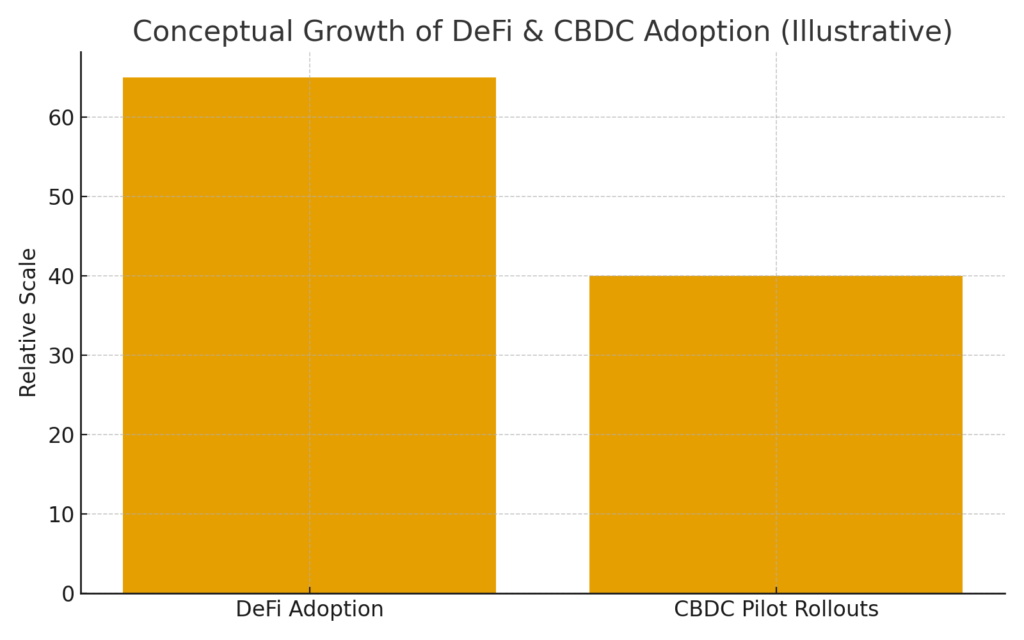

7. Chart Insertions

Debanking Pressure Index

Growth of DeFi & CBDC Adoption

8. Conclusion: Debanking as a Catalyst for a New Financial Era

JP Morgan’s debanking wave is not merely a story of corporate policy—it is a symptom of a deeper structural mismatch between traditional finance and digital-asset ecosystems.

Banks want AML/CFT certainty.

Crypto offers transparency, speed, and autonomy.

Regulators lag behind both.

As long as regulatory clarity remains fragmented, debanking will continue.

But the long-term effect is the opposite of what banks may intend:

- Crypto becomes more decentralized.

- DeFi becomes more essential.

- CBDCs become more urgent.

- Entrepreneurs accelerate innovation outside traditional rails.

Debanking is not the end—it is the beginning of a more resilient, autonomous financial architecture.