Main Points :

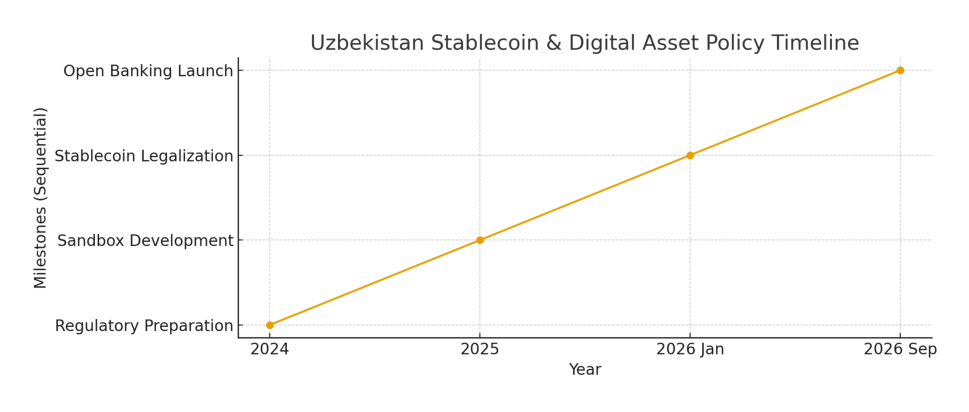

- Uzbekistan will legalize stablecoin payments beginning January 2026, introducing regulated pilot programs and a national sandbox.

- The Central Bank is simultaneously developing a CBDC aimed at interbank settlement, while stablecoins will target retail and commercial users.

- Tokenized securities and RWA (real-world assets) issuance by licensed companies will also be permitted starting 2026.

- The country plans to introduce a full open-banking system by September 2026.

- With global momentum (U.S. GENIUS Act, China’s digital yuan expansion), Uzbekistan aims to position itself among the fastest-growing blockchain-enabled payment economies.

- For crypto users seeking new assets, yield opportunities, and real-world blockchain adoption, Uzbekistan’s regulatory roadmap creates a significant emerging-market catalyst.

1. Introduction — Why Uzbekistan Matters Now

Uzbekistan has announced one of the most ambitious nationwide stablecoin adoption programs in the world, with legalization scheduled for January 2026. For global crypto investors, builders, and fintech operators, this initiative signals a massive shift: a traditionally cash-heavy economy is moving toward blockchain-based payment rails supported directly by regulators.

This article summarizes the developments, expands them with global context, and explores how these changes create new opportunities for crypto users searching for emerging assets, stable revenue models, and practical blockchain utility.

2. Uzbekistan’s Regulatory Vision for Stablecoins

2.1 Launching Stablecoin Payments in 2026

Beginning January 2026, Uzbekistan will legally recognize stablecoin payments, allowing regulated institutions to develop and issue fiat-backed stablecoins under a controlled pilot environment.

The government will adopt a strictly supervised sandbox, similar to frameworks used in Singapore, Hong Kong, and parts of the EU.

Participating financial institutions must issue stablecoins backed 1:1 by fiat currency held in licensed custodians — a model consistent with U.S. regulatory trends.

2.2 Why This Matters for Market Growth

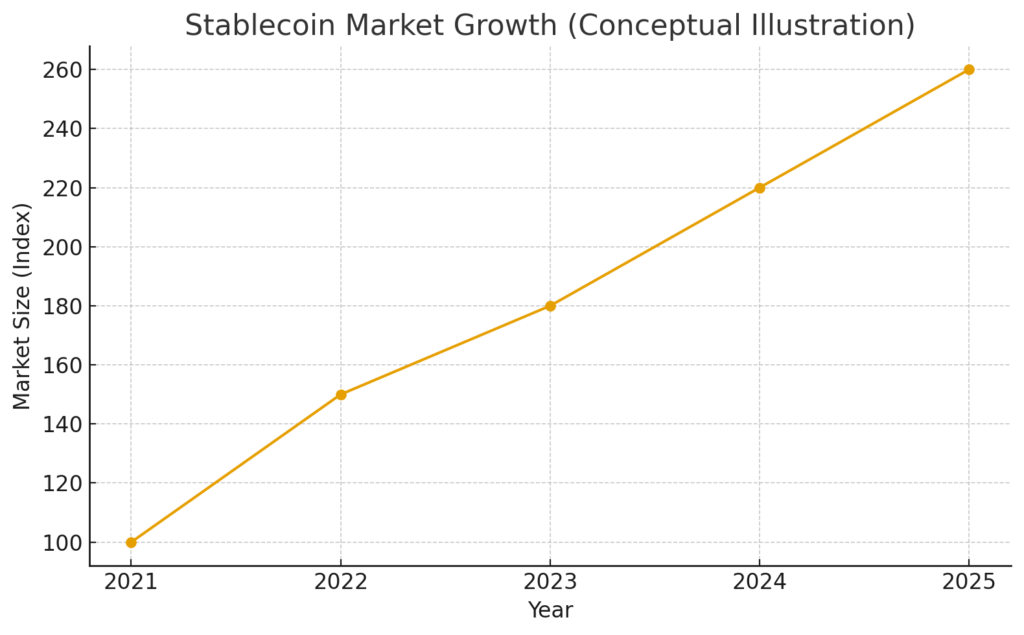

The global stablecoin market has expanded rapidly driven by improved legal clarity, institutional investment, and increasing utility in payments.

Uzbekistan’s adoption comes at a time when many developing nations are exploring blockchain payment systems to accelerate commerce, reduce remittance costs, and combat shadow-economy inefficiencies.

3. Stablecoin and CBDC Roles: A Dual-Layer Strategy

Uzbekistan is taking a two-tier approach to digital money:

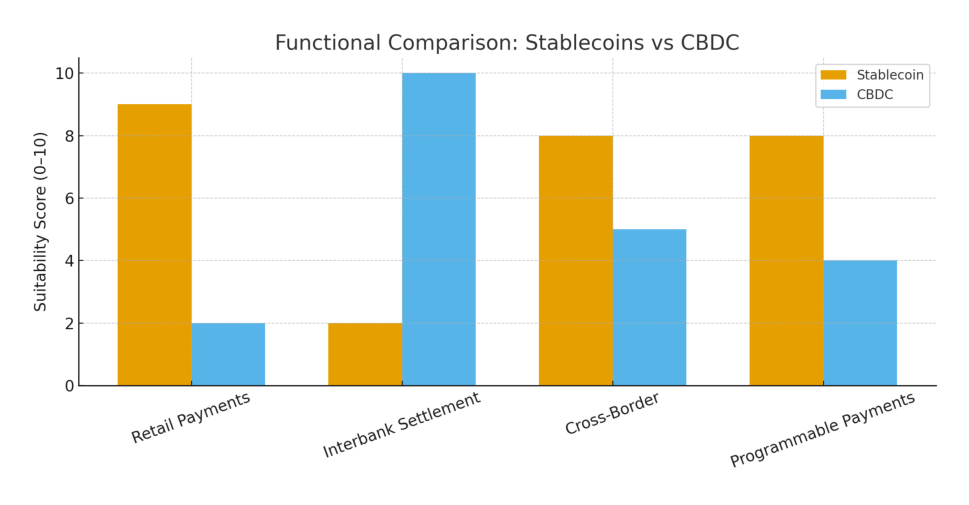

3.1 CBDC for Banks; Stablecoins for Consumers

According to Central Bank Governor Tukur Ishmetov:

- The CBDC will not be a retail currency.

- Instead, it will be used for commercial bank settlements, improving liquidity, finality, and interoperability.

- Meanwhile, stablecoins will serve retail and enterprise payments, enabling:

- e-commerce settlement

- cross-border payments

- mobile wallet integrations

- fintech-bank interoperability

This separation mirrors China’s e-CNY interbank experiments and the U.S. discussions around separating stablecoin functions from wholesale CBDC pilots.

3.2 Why This Architecture Supports Innovation

By allowing private fintech firms to issue stablecoins while the central bank manages interbank settlement via CBDC, Uzbekistan avoids the political and privacy concerns that often hinder full-retail CBDCs.

This creates an “innovation sandbox” where:

- Retail payments remain competitive

- Businesses can create programmable money features

- Fintech-driven stablecoins expand faster than CBDC deployment

It is one of the most future-proofed models currently in development globally.

4. Tokenized Assets and RWA Market Opening (2026)

4.1 License-Based Tokenization of Real-World Assets

From January 2026, legally registered companies will be allowed to issue tokenized assets, including:

- Equity

- Corporate bonds

- RWA investment instruments

This builds on a policy permitting authorized exchanges to develop trading platforms for tokenized securities beginning January 2025.

4.2 Why This Is a Major Opportunity

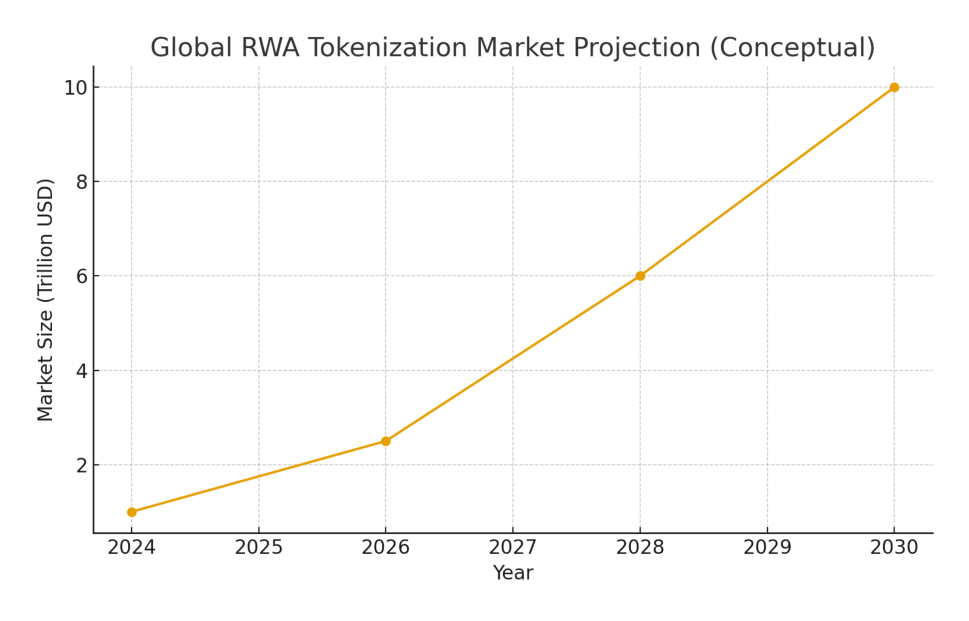

The global RWA tokenization market is projected to exceed $10 trillion by 2030 (various institutional forecasts).

For early-stage crypto investors, tokenized securities provide access to:

- Yield-bearing traditional assets

- Fractionalized investment structures

- Regulated but blockchain-native markets

Uzbekistan entering this space ensures it will become a regional hub for compliant digital financial products.

5. Open Banking by September 2026

Uzbekistan will require financial institutions to adopt open-banking APIs by September 2026.

This enables:

- Secure data sharing between banks and fintechs

- Multi-wallet interoperability

- Faster payment switching

- Embedded finance innovations

Combined with legal stablecoins, this creates a seamless digital asset payment ecosystem.

6. Global Context: How the U.S., China, and EU Are Shaping Stablecoin Adoption

6.1 U.S. GENIUS Act Momentum

After the U.S. introduced the GENIUS Act, stablecoin development accelerated due to:

- Federal acknowledgment of stablecoins as legitimate financial instruments

- Clearer reserve requirements

- Increasing corporate issuer participation

Uzbekistan’s strategy mirrors this approach by tightly regulating issuers while encouraging innovation.

6.2 China’s Digital Yuan Influence

China has pushed CBDC usage across:

- Public transport

- Government payroll

- Cross-border pilot zones

Uzbekistan’s interbank-only CBDC avoids China’s full-retail model but aligns with its infrastructure modernization goals.

6.3 Europe’s MiCA Framework

The EU’s MiCA regulations emphasize transparency, licensing, and stablecoin reserve auditing — principles reflected in Uzbekistan’s 2026 plan.

7. Practical Use Cases for Crypto Investors and Builders

7.1 Payments and Merchant Adoption

Stablecoins will support:

- Low-friction domestic transactions

- P2P payments

- Cross-border trade settlement

Merchants may integrate stablecoin checkout at lower cost than card networks.

7.2 OTC and Treasury Opportunities

Corporate treasuries in emerging markets often lack efficient hedging tools. Fiat-backed stablecoins offer:

- Instant liquidity

- Cross-platform transferability

- Transparent valuation

- Programmable accounting flows

7.3 RWA Investing and Tokenization Yields

With legal tokenization, new investment classes will emerge:

- Tokenized government bonds

- Fractional real estate

- SME debt financing

These markets provide new yield-focused opportunities for crypto-native investors seeking stable returns.

7.4 Fintech Integration and API Development

For developers, the 2026 ecosystem will allow:

- API-driven stablecoin wallets

- Merchant plugins

- Treasury automation tools

- Remittance platforms

Uzbekistan becomes an attractive sandbox for global fintech builders.

8. Risks, Challenges, and What to Watch

8.1 Regulatory Tightening

While innovation is encouraged, stablecoin issuers must meet:

- 1:1 reserve proof

- Periodic audits

- Strict reporting rules

Non-compliant projects will be restricted.

8.2 Infrastructure Readiness

CBDC systems require:

- Real-time settlement layers

- High-availability domestic ledgers

- Secure API gateways

Delays could slow adoption.

8.3 Market Education

Retail users will require:

- Wallet training

- Fraud-awareness programs

- Clear on-/off-ramp procedures

9. Conclusion — A Turning Point for Practical Blockchain Adoption

Uzbekistan’s 2026 roadmap places it among the most forward-leaning blockchain-adopting nations.

For investors seeking new digital assets, RWA markets, or early-stage stablecoin ecosystems, Uzbekistan presents a unique frontier market.

For builders and fintech operators, the combination of:

- Legal stablecoins

- CBDC settlement

- Open banking

- Tokenized assets

creates one of the most comprehensive regulatory environments in Central Asia.

This is more than a payment upgrade — it is the foundation of a next-generation blockchain economy.