Main Points :

- The SEC’s Investor Advisory Committee will meet on December 4 to examine how tokenized equities should function within the existing regulatory environment.

- Nasdaq, BlackRock, and Coinbase will participate, signaling industry-wide momentum toward blockchain-based settlement infrastructure.

- Nasdaq has submitted a proposal advocating that tokenized equities trade on the same order books as traditional equities within the National Market System (NMS).

- The U.S. debate centers on native tokenization with full shareholder rights, not synthetic “wrapped” tokens.

- Tokenization is positioned as a settlement technology, not a new asset class.

- The discussion will test issues like custody, short selling, transparency, and 24/7 markets.

- Industry consensus could influence eventual SEC approval of tokenized securities.

- Recent developments indicate growing institutional adoption of blockchain settlement, including moves by DTCC, BlackRock, JPMorgan, and Hong Kong regulators.

I. Introduction — Why Tokenized Equities Matter Now

For years, blockchain advocates have argued that modern capital markets—still dependent on fragmented ledgers, settlement delays, and heavy intermediaries—could be drastically improved through distributed ledger technology (DLT). Until recently, the idea remained largely theoretical, constrained by regulatory uncertainty. But in 2025, the momentum has shifted.

The U.S. Securities and Exchange Commission (SEC) has scheduled a December 4 meeting to examine how publicly traded stocks might be represented and settled on blockchain networks. Importantly, the panel includes some of the most influential actors in global finance: Nasdaq, BlackRock, Coinbase, and other market infrastructure specialists.

This signals more than a technical discussion. It represents a pivotal moment where tokenization—long discussed as a future innovation—may soon be incorporated into mainstream equity markets. For investors searching for new digital assets, income opportunities, or practical applications of blockchain technology, this development marks a significant inflection point.

II. What Triggered the SEC Meeting: Nasdaq’s Proposal

Nasdaq’s Core Argument

Nasdaq recently submitted a formal proposal urging regulators to allow tokenized equities to be traded on the same order books as traditional stocks, and settled within the existing National Market System (NMS).

The key position is clear:

- Tokenization should not create a new category of financial instrument.

- Instead, it should act as a settlement layer upgrade—a replacement for legacy back-end systems.

In this model, the stock itself remains the same regulated security. The innovation lies in how ownership is recorded and transferred.

Blockchain becomes an alternative to the DTCC’s traditional ledger, potentially providing:

- Instant settlement

- Reduced counterparty risk

- Lower administrative overhead

- Greater transparency

- Programmable compliance and reporting

Why It Matters

If approved, this structure would allow Wall Street to modernize without rewriting securities laws. It becomes a technological evolution rather than a regulatory revolution.

III. Tokenization Models: Native vs Wrapped

A major theme in the SEC’s upcoming discussion is the difference between native tokenization and wrapped-like synthetic instruments.

Wrapped Tokens (Price-Pegged Synthetic Assets)

Seen in some international markets, these tokens:

- Mirror the price of a stock

- Do not grant shareholder rights

- Often exist outside regulated venues

- Enable 24/7 speculative trading

These instruments raise investor protection concerns because they provide economic exposure without legal ownership.

Native Tokenized Equities (Full Shareholder Rights)

The U.S. is focused on this model:

- Blockchain token = the actual regulated share

- Investor retains legal and beneficial ownership

- Voting, dividends, disclosures, and rights remain intact

- Recorded on chain but governed by U.S. securities law

Nasdaq and industry groups warn that failing to standardize native tokenization could push investors toward opaque offshore products lacking oversight. Their goal is to ensure that any tokenized equity maintains complete legal integrity.

IV. Stress-Testing Key Issues: What the SEC Wants to Examine

The Investor Advisory Committee does not propose rules directly, but its recommendations often shape future SEC priorities. The December 4 session is described as a “stress test” for several systemic questions:

1. Custody (Asset Safekeeping)

- How should broker-dealers and custodians secure blockchain-based shares?

- Should regulated custodians hold private keys?

- How do you mitigate risks of key loss, compromise, or operational errors?

2. Short Selling

Short selling relies on lending and locating shares. Tokenized shares may:

- Enable instantaneous proof of borrow

- Remove the opacity that contributed to past market failures

But the SEC must determine how these mechanics adapt to blockchain.

3. 24-Hour Trading

Blockchain makes round-the-clock markets technically feasible. But:

- U.S. equity markets have regulatory protections built around trading hours.

- Surveillance, clearing, and broker obligations may need redesign.

4. Interoperability with the National Market System

- Can blockchain settlement co-exist with DTCC infrastructure?

- Will there be conflicts between on-chain and off-chain records?

5. Market Surveillance

Regulators need visibility across venues.

- Blockchains offer transparency but introduce pseudonymity challenges.

- Integration with FINRA and SEC surveillance systems must be solved.

V. Recent Global Developments: Institutional Momentum Toward Tokenization

To complement the original article, here are some recent developments that further show why tokenized equities are moving to the forefront of global finance:

1. DTCC’s Smart Contract Pilots

The U.S. clearing giant has tested tokenized settlement frameworks with:

- JPMorgan’s Onyx blockchain

- Broadridge’s DLT repos

Early pilots demonstrated significant reductions in settlement friction.

2. BlackRock’s Tokenization Strategy

BlackRock CEO Larry Fink has repeatedly described tokenization as:

- The future of financial markets

- A path toward “perfect record-keeping”

- A mechanism for faster, more transparent global securities settlement

BlackRock’s $100+ billion tokenized fund strategy in 2024–2025 accelerated adoption among institutions.

3. JPMorgan and Citi Expand Tokenized Assets

JPMorgan’s Onyx processes tokenized intraday repo transactions exceeding $1 billion daily, while Citi launched:

- Tokenized cash solutions

- Blockchain-based trade finance instruments

4. Hong Kong and Singapore Introduce Tokenization Frameworks

- Hong Kong’s SFC approved tokenized structured products.

- Singapore’s MAS conducted Project Guardian with global banks.

5. EU’s DLT Pilot Regime

Europe now allows tokenized equities and bonds to trade on licensed DLT market infrastructures, serving as a regulatory sandbox.

The combined effect: Tokenization has moved from theory to practice across global jurisdictions.

VI. Market Potential: Why Tokenized Equities Are a Major Crypto Opportunity

For readers exploring new digital assets and revenue streams, tokenized equities introduce several key opportunities:

1. Demand for New Settlement Tokens and Infrastructure Tokens

Blockchains facilitating regulated tokenized securities (e.g., enterprise chains, interoperability layers) may see increased institutional adoption.

2. Growth in Tokenized Funds, Bonds, and Deposits

Investors may diversify into:

- Tokenized treasuries

- Tokenized money market funds

- Tokenized corporate bonds

This trend already exceeds $1.5 billion globally.

3. Bridging Crypto and Traditional Finance

Platforms that support:

- Tokenized stock trading

- 24/7 fractional global markets

- Automated compliance

are positioned for explosive growth.

4. New Business Models

Including:

- On-chain brokerage infrastructure

- Automated KYC/KYT systems

- Digital asset custody

- Cross-border tokenized settlements

VII. Graphs and Diagrams

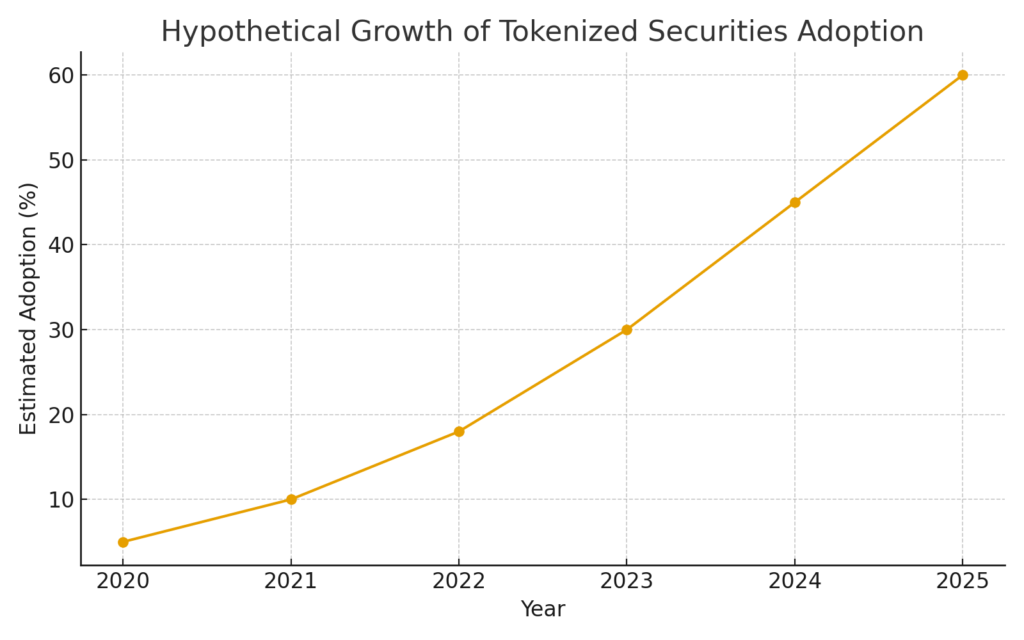

Tokenized Securities Adoption Growth

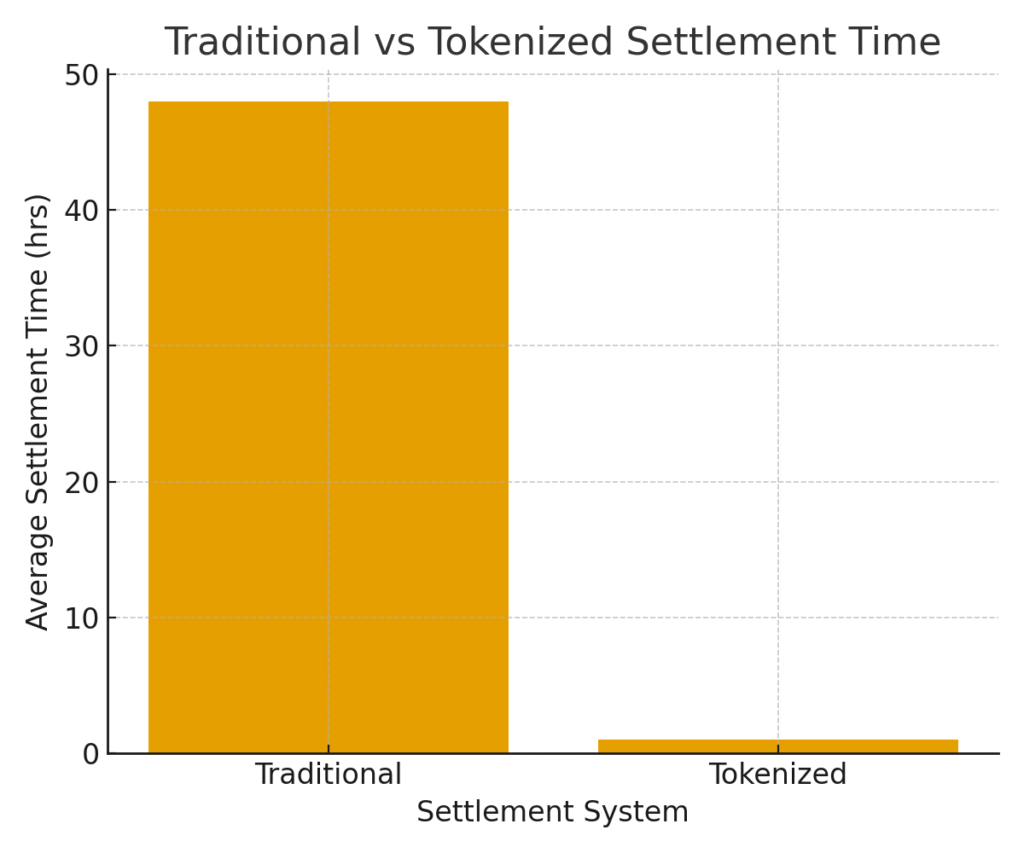

Traditional vs Tokenized Settlement Time

VIII. Conclusion — Toward a Tokenized Market Structure

The SEC’s December 4 meeting represents a critical turning point in the modernization of U.S. capital markets. Whether tokenized equities are adopted quickly or cautiously, the direction is unmistakable:

Blockchain-based settlement is becoming an institutional priority.

If the U.S. aligns with global markets and endorses native tokenization:

- Trading becomes faster and more transparent

- Settlement risks shrink

- Broker-dealer operations become more efficient

- Cross-border securities distribution becomes seamless

- A completely new layer of digital asset infrastructure emerges

For investors exploring the next wave of crypto opportunities, tokenized securities may become one of the largest growth categories of the next decade—not as speculative instruments, but as the backbone of modern finance.