Main Points :

- S&P Global Ratings has downgraded Tether (USDT) stability rating to the lowest level — “5 (Weak)”.

- The downgrade reflects increased exposure in USDT reserves to high-risk assets (e.g. Bitcoin, gold, secured loans, corporate bonds), along with persistent transparency gaps.

- Bitcoin alone now represents around 5.6% of Tether’s reserves — exceeding the 3.9% over-collateralization margin, raising the risk of under-collateralization upon a price drop.

- Tether management strongly rejects the downgrade, arguing that the methodology applies outdated traditional finance models and fails to capture USDT’s real-world utility, resilience, and transparency.

- The downgrade comes at a pivotal moment: regulation of stablecoins is accelerating globally, and the stablecoin market just exceeded a total market cap of around US$300 billion.

Why S&P Downgraded USDT: Reserve Risk and Transparency Concerns

Shift from “Constrained” to “Weak”

On November 26, 2025, S&P Global Ratings formally lowered USDT’s Stablecoin Stability Assessment from “4 (Constrained)” to “5 (Weak).” The move signals that S&P now regards USDT as the least stable among assessed stablecoins in terms of maintaining its peg to the U.S. dollar.

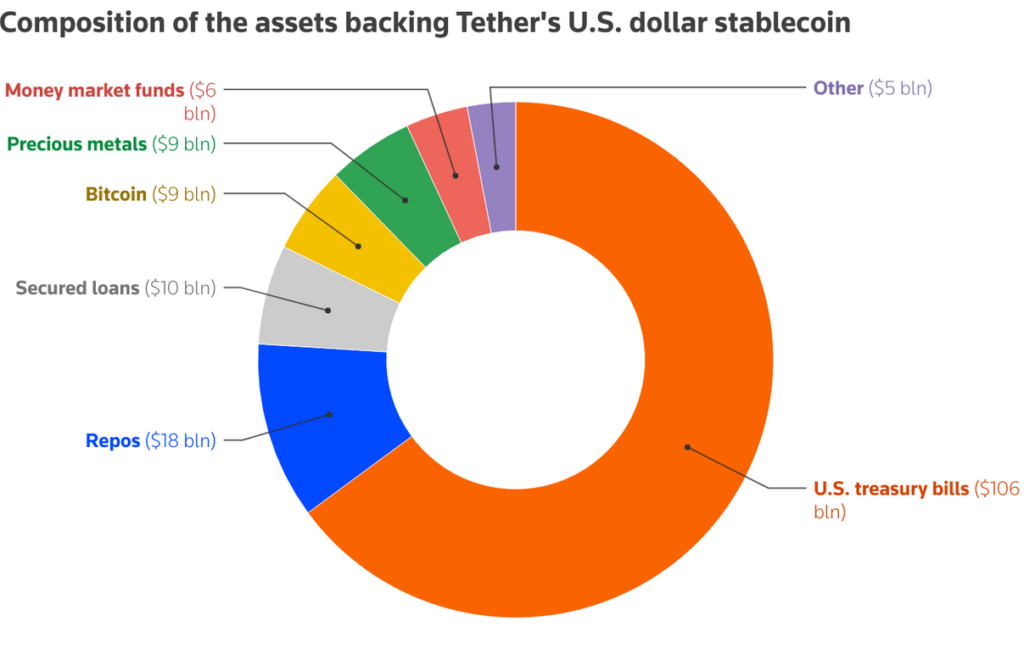

S&P explained the downgrade by pointing to a significant increase over the past year in the share of “higher-risk” assets backing USDT. These assets include volatile or credit-sensitive holdings such as Bitcoin, gold, secured loans, and corporate bonds — asset classes that are subject to market, credit, interest-rate, and foreign-exchange risks.

Moreover, S&P flagged “persistent gaps in disclosure” from Tether: limited transparency about custodians, counterparties, and bank account providers, insufficient asset segregation protections (which would matter if the issuer becomes insolvent), and restricted redeemability (i.e., not all USDT holders may be able to redeem directly with Tether in all circumstances).

The Bitcoin Problem: Exceeding Over-Collateralization Margin

One of the most striking facts cited in the downgrade is that Bitcoin — with all its volatility — now makes up about 5.6% of USDT’s total reserve backing. That alone exceeds the over-collateralization buffer of 3.9%. In other words, if Bitcoin’s price drops sharply, the reserve could no longer guarantee full backing of USDT.

S&P warns that a simultaneous decline in Bitcoin and other high-risk assets could significantly reduce collateral coverage, potentially leading to under-collateralization. In practical terms, that means USDT might fail to maintain a hard 1:1 peg with USD under stress — undermining one of the core assumptions users place in stablecoins.

Reaction from Tether: Defense, Critique, and Market Strategy

Unsurprisingly, Tether management reacted harshly to the downgrade. The company argues that S&P’s downgrade is based on a “legacy framework” — a risk-assessment methodology originally designed for traditional financial institutions. According to Tether’s leadership, such framework fails to take into account the “nature, scale, and macroeconomic importance of digitally native money” — effectively, stablecoins.

Tether claims its reserves remain “over-capitalized” and contain no “toxic” assets. The firm insists that the downgrade ignores data showing USDT’s resilience, transparency improvements, and widespread real-world utility — such as high daily trading volumes, global usage, and liquidity.

They also argue that, historically, many institutions rated “investment grade” using traditional metrics eventually failed — implying that being rated with conventional frameworks does not guarantee safety.

Context: Why This Matters for Crypto Investors and Corporate Uses

A Stablecoin’s Stability Under Scrutiny

For a stablecoin to serve as a dependable medium of exchange, store of value, or unit of account — especially in institutional or corporate use cases — what matters most is stability and certainty. A downgrade of this magnitude from a globally recognized credit rating agency shakes that confidence.

Many traders and institutional actors rely on stablecoins as “cash equivalents” within the crypto ecosystem. They use them for trading, lending, remittance, bridging between on-chain/off-chain assets, or as collateral. If USDT becomes viewed as risky, its utility as a stable base asset could erode — leading to potential shifts in demand toward other stablecoins, or even toward non-crypto alternatives.

Regulatory Pressure and Market Timing

The downgrade comes at a time when global regulators and governments are stepping up scrutiny of stablecoins. The stablecoin market has recently surpassed a total market cap of around US$300 billion.

In such a regulatory atmosphere, agencies like S&P reduce uncertainty for investors and counterparts by flagging potential weaknesses. For projects, funds, or VASP/EMI institutions (such as the kind you’re working on), this downgrade could influence decisions around which stablecoins to accept, hold, or integrate.

What This Means for Alternative Stablecoins and New Assets

If confidence in USDT weakens, this could create opportunities for other stablecoins — especially those with more transparent, low-risk reserve models (e.g., fully backed by cash / short-term treasuries, or with strong public audits). It might also fuel interest in algorithmic stablecoins (though they carry different risks), or stablecoins issued under stricter regulatory frameworks.

Furthermore, projects that leverage stablecoins for payments, remittance, token sales (ICOs/IEOs), or DeFi may need to reassess their choice of stablecoin. Especially for financial institutions, EMIs, or VASPs operating in jurisdictions with compliance requirements (like the Philippines), the downgrade raises compliance and risk-management questions.

Broader Landscape: What Recent Data and Market Dynamics Say

- Despite the downgrade and price volatility in the broader crypto market, the circulating supply of USDT reportedly remained substantial — in some sources noted at roughly US$184 billion.

- Meanwhile, Tether appears to have increased holdings of gold, secured loans, and corporate bonds in addition to Bitcoin — diversifying its reserve portfolio, albeit toward asset classes with higher volatility or credit risk.

- On the macro front, market participants face a crypto environment where risk sentiment remains fragile: Bitcoin and many other crypto assets have experienced sharp declines, which increases the likelihood that high-risk reserve assets lose value — exacerbating the under-collateralization risk flagged by S&P.

- At the same time, demand for stablecoins remains high globally — for trading, remittance, and as liquidity rails. Therefore, even a “weak” rating may not immediately translate to a collapse in usage.

What Should Investors, Projects, and Crypto-Native Businesses Do?

For those searching for new crypto assets, yield opportunities, or practical blockchain-based payment or remittance systems — this downgrade is a strong signal to re-evaluate USDT’s role in portfolios and infrastructures.

- Review reserve backing and transparency criteria — prioritize stablecoins with clearly disclosed, low-risk reserves, frequent third-party audits, and redeemability.

- Diversify stablecoin exposure — rather than relying solely on USDT, spread risk across multiple stablecoins or asset types to reduce exposure to any single issuer.

- Monitor regulation and institutional acceptance — as regulators intensify scrutiny, VASPs/EMIs should consider compliance, custody risks, and counterparty risk when integrating stablecoins.

- Track market conditions — sharp downturns in crypto and macroeconomic stress can materialize the risks highlighted by S&P; plan for stress scenarios.

Finally, for those building blockchain applications — token sales, remittance gateways, wallets, DeFi platforms — this is a reminder to architect systems with flexibility: allow for stablecoin substitution, support multiple reserve-backed tokens, and design for transparency.

Conclusion: A Call for Caution, But Not Panic

The downgrade of USDT by S&P Global Ratings marks a critical inflection point in the stablecoin ecosystem. While it does raise real red flags around reserve composition, asset risk, and transparency, it does not necessarily spell the end for USDT — at least not immediately.

For investors and crypto-native businesses, the key takeaway is not to panic, but to re-assess. The stability and transparency of a stablecoin should matter as much as its convenience or liquidity. Especially in a volatile macroeconomic and regulatory environment, prudent actors will adjust exposure, diversify, and demand higher quality collateral and disclosure standards.

That said, the downgrade could accelerate a shift toward alternative stablecoins or new stablecoin models (e.g., fully collateralized, regulated, or tokenized-asset backed) — possibly reshaping the stablecoin landscape in 2026 and beyond. The era where a single stablecoin reigned supreme may be drawing to a close.