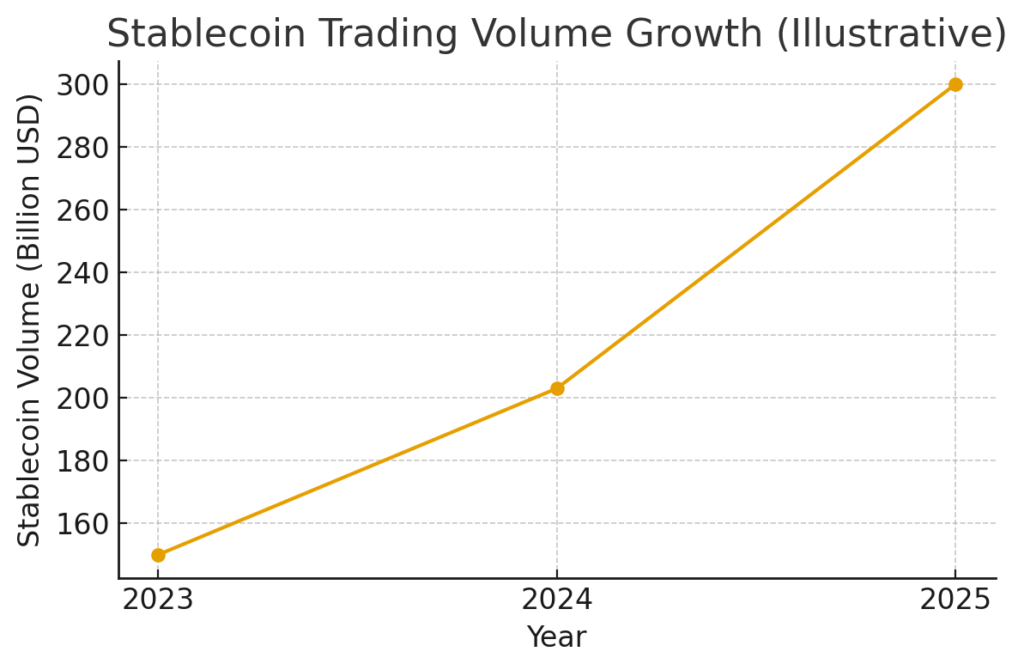

Stablecoins tied to USD have grown rapidly, exceeding $300 billion in trading volume in 2025.

ECB officials warn that a “stablecoin run” could trigger forced liquidation of U.S. Treasuries, destabilizing global markets.

The U.S. has introduced its first federal regulatory framework—the Genius Act, requiring 1:1 reserves and strict audits.

Europe worries that U.S.-denominated stablecoins could weaken the ECB’s monetary control.

For crypto investors, stablecoin expansion signals new yield opportunities—but also systemic risk.

International regulatory divergence (U.S. permissive vs. EU conservative) will shape stablecoin liquidity and adoption.

A large-scale stablecoin crisis could force central banks to reconsider interest rate policy.

Introduction: A Turning Point for Global Finance

In November 2025, a Financial Times report highlighted a significant warning from Olaf Sleijpen, the Dutch central bank president and senior policymaker at the European Central Bank (ECB). His message was straightforward yet alarming: if a bank-run-style event occurs with stablecoins, the ECB may be forced to reconsider its monetary policy stance altogether.

This warning is not theoretical. Stablecoins—crypto tokens backed by fiat currency or highly liquid assets—have grown from a niche payment tool to a systemically important financial instrument. In 2025 alone, the trading volume of stablecoins increased 48%, surpassing $300 billion, driven largely by policy shifts in the United States enabling private-sector stablecoin issuance.

As stablecoins increasingly rely on U.S. Treasury bills as reserve assets, the global financial system finds itself more intertwined with these digital instruments than ever before. The risks, benefits, and macroeconomic implications are now unavoidable topics for policymakers and crypto investors alike.

1. The ECB’s Warning: Stablecoins Could Trigger Policy Reassessment

Sleijpen argued that if stablecoins were to experience a run—similar to historical crises involving money market funds—the liquidation of reserve assets could disrupt not only crypto markets but the broader financial system.

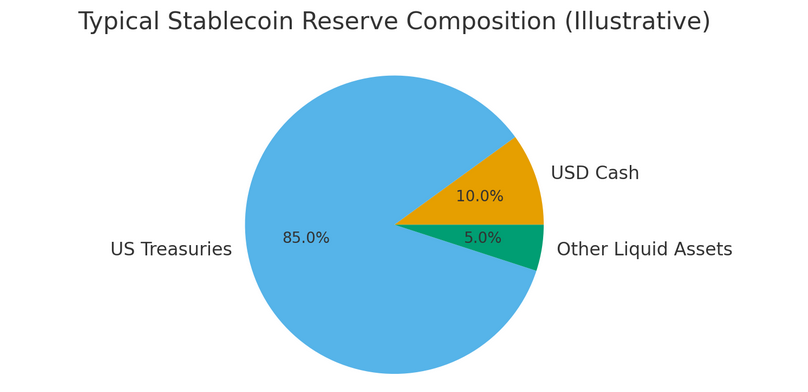

Stablecoins like USDT and USDC typically maintain stability by holding reserves such as:

U.S. dollar cash

Short-term U.S. Treasury bills

Commercial paper (less common now due to regulation)

If billions of dollars’ worth of stablecoins were redeemed suddenly, issuers would be forced to sell these assets rapidly, pushing yields higher and depressing bond prices. This could raise funding costs across the economy and undermine central bank policy transmission.

Sleijpen’s concern is clear:

“If stablecoins are not truly stable, we may face situations where reserve assets must be sold rapidly, threatening financial stability and affecting inflation.”

This scenario mirrors historical liquidity crises such as:

the 2008 money market fund collapse

the March 2020 Treasury market dislocation

The ECB’s fear is not speculative—it is grounded in known vulnerabilities.

2. U.S. Policies Fuel the Rise of Dollar-Based Stablecoins

The Financial Times report attributes much of the rapid stablecoin growth to President Trump’s regulatory reform, which enabled private companies to issue stablecoins under a federal framework. This policy shift included:

Legalization of private stablecoin issuance

Broader access to financial infrastructure

Market clarity that boosted institutional involvement

As a result, stablecoins became deeply integrated into:

U.S. Treasury markets

Money market investment flows

Global crypto-trading liquidity

The trend has reinforced the dollar’s dominance, even in digital financial ecosystems. Many stablecoins now function as synthetic “digital dollars,” circulating through crypto exchanges, DeFi platforms, and cross-border payment channels.

3. Europe’s Fear: Losing Monetary Sovereignty

From the ECB’s perspective, the danger lies not just in liquidity crises—but in losing control over monetary policy within Europe.

If Europeans increasingly use USD-backed stablecoins for payments, saving, and DeFi activities, then:

ECB policy rates could have weaker impact

Monetary transmission decreases

Eurozone financial stability is affected

Christine Lagarde, President of the ECB, has repeatedly warned the European Parliament that stablecoins may:

“Disrupt monetary policy transmission and introduce risks to both financial stability and economic control.”

This is especially concerning as crypto adoption grows among younger populations in Europe, many of whom prefer USD stablecoins like USDT for trading and savings.

4. Nobel Laureate Jean Tirole: Governments Could Face Billion-Dollar Bailouts

Jean Tirole, one of the world’s most influential economists, warned that if major stablecoins collapse, governments may be forced to bail out impacted investors to prevent systemic contagion—costing potentially tens of billions of dollars.

This is not far-fetched. Stablecoin issuers function much like:

private banks

money market funds

shadow financial institutions

Thus, a coordinated run on multiple stablecoins could lead to:

forced liquidation of U.S. Treasuries

liquidity shortages

higher yields

pressure on currency markets

Governments may intervene—not to save crypto—but to protect national financial stability.

5. The U.S. “Genius Act”: A New Federal Standard

In July 2025, the United States enacted the Genius Act, the first federal stablecoin law. It requires:

1:1 reserve backing

Reserves limited to USD cash and short-term Treasuries

Mandatory monthly disclosures

Independent audits

This law addresses many of the concerns raised by European regulators. It does not eliminate risk, but it pushes stablecoins toward:

higher transparency

improved reserve quality

reduced contagion potential

The regulatory difference between the U.S. and Europe will significantly shape market direction.

6. Global Trend: Stablecoins Are Becoming Systemically Important

Beyond the U.S. and Europe, countries worldwide are reassessing the role of stablecoins:

Japan legalized yen-backed stablecoins with strict oversight.

Singapore introduced a regulatory regime requiring 1:1 reserves.

Hong Kong is building a licensing framework for stablecoin issuers.

The Middle East is exploring stablecoin integration for cross-border trade.

The IMF and BIS have also called for global coordination to prevent regulatory arbitrage—where issuers operate in the most lenient jurisdictions.

Stablecoins are no longer just a crypto tool. They are a pillar of modern digital finance and a growing concern for macroeconomic stability.

7. For Crypto Investors: Opportunity and Risk

For investors seeking new crypto assets, yield opportunities, or blockchain utility, the rise of stablecoins creates several trends worth watching:

1. Treasury-Backed Yields

Treasury yields (currently around 4.2–4.6%) create:

higher stablecoin reserve income

potential revenue for issuers

new staking or yield-sharing models

2. On-Chain Finance Growth

Stablecoins fuel:

decentralized lending

liquidity pools

yield farming

tokenized real-world assets

3. Stablecoin Dominance in Trading

Over 70% of crypto trades now use USD stablecoins as the base pair.

4. Systemic Risk Exposure

Stablecoins importing risks from traditional finance:

Treasury liquidity shocks

redemption waves

depegging events

Investors should prepare for volatility triggered by macro-policy changes.

8. What Happens If a Stablecoin Run Occurs?

A run scenario would unfold like this:

Stablecoin loses peg (e.g., drops to $0.98).

Investors rush to redeem tokens for USD.

Issuers must sell Treasuries to meet redemptions.

Treasury yields rise, prices fall.

Risk spreads across global markets.

Central banks may need to intervene.

In such a case, Sleijpen warns:

The ECB may need to reconsider interest rate policy and activate stabilization tools.

Whether this means raising or lowering rates depends on the type of shock:

If inflation risk rises → interest rate hikes

If liquidity dries up → interest rate cuts

This dual possibility captures the uncertainty stablecoins introduce to monetary systems.

Conclusion: The Future of Stablecoins and Global Monetary Stability

Stablecoins are no longer an experimental technology. They represent a new layer of global finance—one with benefits (efficiency, liquidity, innovation) and significant risks (liquidity contagion, monetary sovereignty erosion).

The ECB’s warning serves as a reminder that crypto is now influencing central bank policy. As stablecoins expand beyond $300 billion toward potentially trillions, their systemic importance will only grow.

For crypto investors, fintech founders, and policymakers, the message is clear: Stablecoins will shape the next era of financial markets—bring both opportunity and risk—and require robust global regulation.

About Us and Media

Blockchain and cryptocurrency media covering and exposing the practical application development on the blockchain industry and undiscovered coins.

Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.