Main Points :

- JPMorgan has deployed JPM Coin (JPMD) on Coinbase’s Base network, marking one of the first major moves by a global bank onto a public blockchain.

- JPM Coin is a tokenized bank deposit, different from stablecoins because it directly represents customer dollar deposits and can accrue interest.

- The launch bridges regulated banking infrastructure and permissionless DeFi, enabling both to operate on the same settlement rails.

- Base has already handled more than $1 billion in BTC-backed on-chain loans, and the addition of JPM Coin signals deeper convergence between TradFi and DeFi.

- Global banks—including Citi, Deutsche Bank, Santander, and PayPal—are moving toward blockchain-based settlement networks, driven by regulatory clarity and institutional demand.

- Deposit tokens may soon become a core financial primitive for collateral, liquidity management, and cross-border payments.

Introduction: A Historic Convergence of Banking and Blockchain

The financial industry has entered a defining moment. JPMorgan, one of the world’s largest and most influential banks, has launched its blockchain-based deposit token, JPM Coin, directly on Base, Coinbase’s Ethereum Layer-2 network.

This development is more than a simple technical integration—it signals a structural shift. For the first time, a globally-systemic bank is operating tokenized deposits on a public, permissionless network that also hosts DeFi lending protocols, BTC-backed loans, and open-source financial applications.

The implications are vast: instant payments, programmable settlement, new collateral models, and the dissolution of barriers between traditional finance (TradFi) and decentralized finance (DeFi).

And crucially, deposit tokens like JPM Coin represent actual bank deposits, not reserves held by issuers—making this an entirely different category from stablecoins.

Part 1 — What JPM Coin on Base Means

A New Rail for Tokenized Bank Deposits

JPM Coin (ticker: JPMD on Base) directly represents USD deposits held at JPMorgan.

It is issued by JPMorgan’s blockchain division, Kinexys, and backed 1:1 with customer deposits.

Unlike USDC, USDT, or other stablecoins, JPM Coin:

- Represents real customer deposits

- Is fully integrated into the banking system

- Can legally accrue interest

- Is regulated under existing banking frameworks

This means a corporate client or institutional investor can hold tokenized deposits, earn interest, and use them for instant settlement on a public chain.

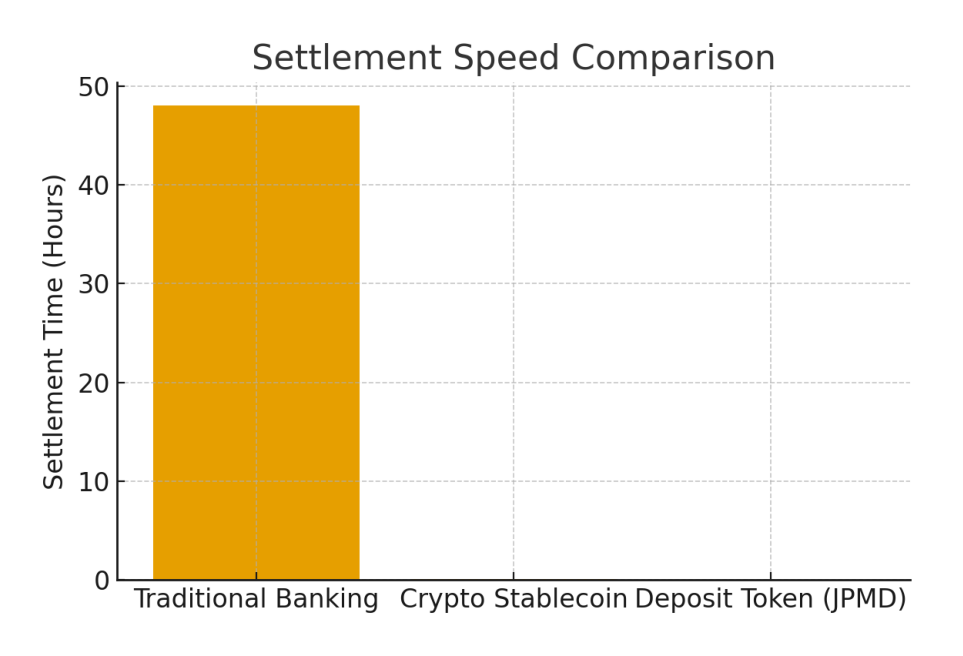

Instant Settlement, 24/7/365

JPMorgan executive Naveen Mallela emphasized that transactions can settle “in seconds, at any time of day.”

This eliminates limits imposed by banking hours, holidays, and cross-border cut-off cycles.

The shift resembles how email replaced postal mail—settlement becomes continuous, not episodic.

Part 2 — Base as the Bridge Between TradFi and DeFi

Why Base?

Base, built by Coinbase, is a fast and cheap Ethereum Layer-2 designed for mass-scale financial applications.

It already hosts:

- BTC-backed lending protocols

- USDC lending markets

- Morpho lending vaults

- High-volume on-chain liquidity systems

With more than $1 billion in BTC-backed loans already processed, Base is rapidly becoming a center of gravity for DeFi credit markets.

The addition of JPM Coin marks the first time a regulated bank token and permissionless DeFi apps coexist on the same chain.

TradFi and DeFi Are Now Sharing Settlement Rails

Before now, banking systems and DeFi protocols lived in separate universes.

That separation is dissolving.

With JPM Coin on Base:

- A bank deposit token can move through automated smart contracts

- Institutions can use tokenized deposits as collateral

- Real-world bank funds can interact with on-chain liquidity primitives

This also means future yield markets could directly involve bank-issued assets, not only crypto-native tokens.

Part 3 — How Deposit Tokens Differ From Stablecoins

Stablecoins vs Deposit Tokens: A Structural Comparison

Deposit tokens and stablecoins may look similar, but they differ at a deeper level:

| Feature | Stablecoin (e.g., USDC, USDT) | Deposit Token (e.g., JPM Coin) |

|---|---|---|

| Backed by | Reserve assets held by issuer | Actual deposits at a regulated bank |

| Regulatory framework | Money transmitter or trust charter | Full banking regulation |

| Can pay interest? | No | Yes |

| Settlement access | Limited to crypto rails | Fully integrated in global banking |

Deposit tokens are not a replacement for stablecoins—but institutions may prefer them because of clarity, safety, and interest accrual.

This could challenge existing stablecoin issuers, particularly in B2B and institutional markets.

Part 4 — Global Banks Are Moving Toward Blockchain Settlement

A Broader Trend in Banking

JPMorgan is not alone.

Major banks exploring blockchain-based settlement include:

- Citi – studying tokenization for collateral and ETFs

- Deutsche Bank – building a compliance-friendly Layer-2

- Santander – expanding blockchain custody and settlement pilots

- PayPal – launching PYUSD and related blockchain initiatives

Institutions are aligning with emerging regulatory frameworks such as the U.S. Genius Act and Europe’s MiCA.

Demand is rising for assets that combine:

- Interest earnings

- Regulatory clarity

- Instant settlement

- On-chain programmability

Deposit tokens meet this demand.

Part 5 — Why This Is a Big Deal for Crypto Investors

New Yield Opportunities

Because deposit tokens can accrue interest, DeFi protocols may eventually:

- Use them as collateral

- Create tokenized money-market vaults

- Build real-world yield strategies without relying solely on crypto volatility

- Enable institutional-safe lending markets

This could introduce bank-grade yield into the DeFi world.

More Liquidity, More Reliability

Institutions trust bank deposits.

If bank-issued assets enter on-chain liquidity pools, the DeFi ecosystem could see:

- Lower volatility

- More liquidity depth

- Higher stability

- New institutional user flows

This may attract a new class of investors looking for safer income-generating blockchain assets.

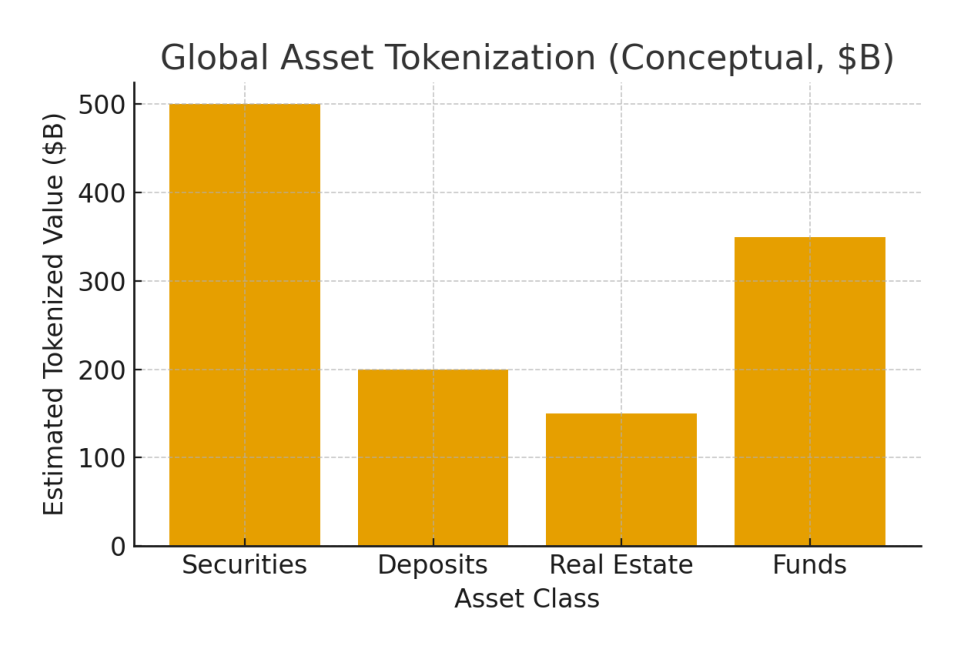

Part 6 — Multi-Currency Tokenized Deposits Are Coming

JPMorgan has already confirmed that it is preparing EUR-based JPME tokens, pending regulatory approval.

Future developments may include:

- Multi-currency deposit tokens

- Cross-bank interoperability

- Cross-border, real-time institutional settlement

- On-chain FX markets backed by bank deposits

The long-term vision resembles a global settlement grid where banks issue programmable money interoperable across public blockchains.

Conclusion — The First Step Toward a Tokenized Banking System

The deployment of JPM Coin on Base is more than a pilot—it is a symbol of where financial infrastructure is heading.

This moment marks:

- The beginning of bank deposits as programmable digital assets

- The merging of traditional financial rails with open DeFi infrastructure

- The emergence of deposit tokens as a new institutional financial primitive

- The acceleration of 24/7, real-time global settlement

As banks, DeFi protocols, regulators, and institutions align, blockchain is transitioning from a speculative frontier into a unified financial network.

For investors seeking new revenue opportunities and practical blockchain applications, this is one of the clearest signals yet:

The future of global finance is tokenized—and it is arriving faster than expected.