Main Points :

- The Australian Securities & Investments Commission (ASIC) is clarifying licensing and regulatory obligations for crypto-asset service providers under the existing Australian Financial Services (AFS) regime.

- The regulator’s updated guidance emphasises that stablecoins and tokenised assets may fall within the definition of “financial products” and trigger licensing, disclosure and conduct obligations.

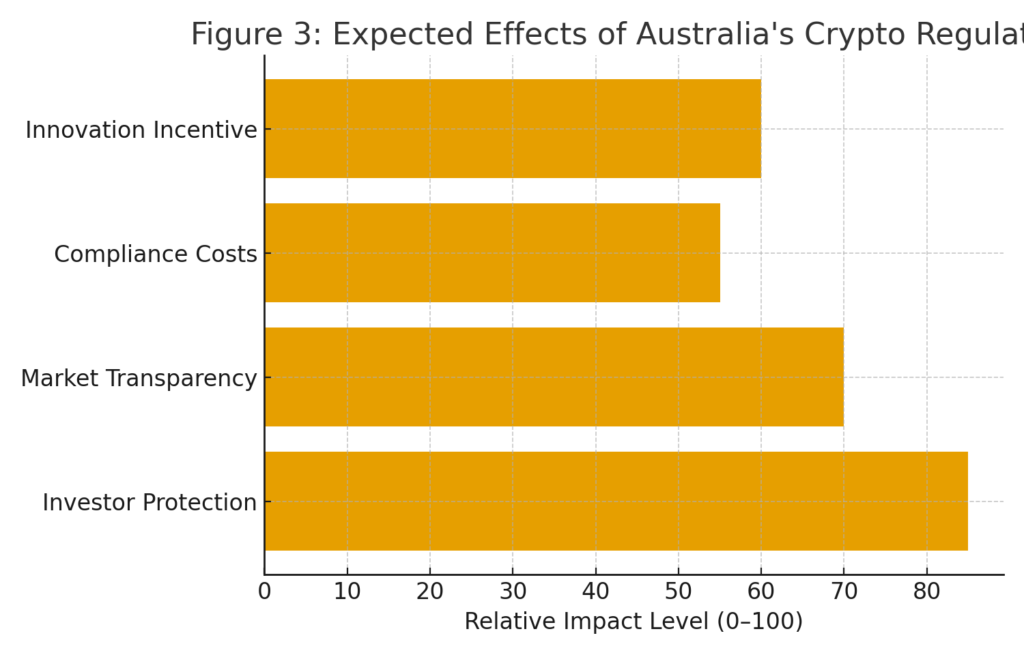

- Industry welcomes the increased clarity but warns that practical compliance costs, limited specialist resources and banking access issues could create bottlenecks.

- The Australian Government Treasury is proceeding with draft legislation for digital-asset platforms (DAPs) and payment stablecoins, aiming to strike a balance between innovation and investor protection.

- For blockchain practitioners and asset-seekers, Australia’s shift offers both a roadmap for regulated issuance/operations and signals that tokenisation, stablecoins and digital-payments infrastructure are gaining regulatory legitimacy.

1. Regulatory Clarification by ASIC

In recent months, ASIC has taken firm steps to articulate how the existing financial-services laws in Australia apply to crypto assets and related services. The regulator’s information page on “Crypto-assets” explains that entities issuing tokens, providing intermediary services (such as dealing, advising, custody) or operating platforms may trigger obligations under the AFS regime, the Corporations Act and other laws.

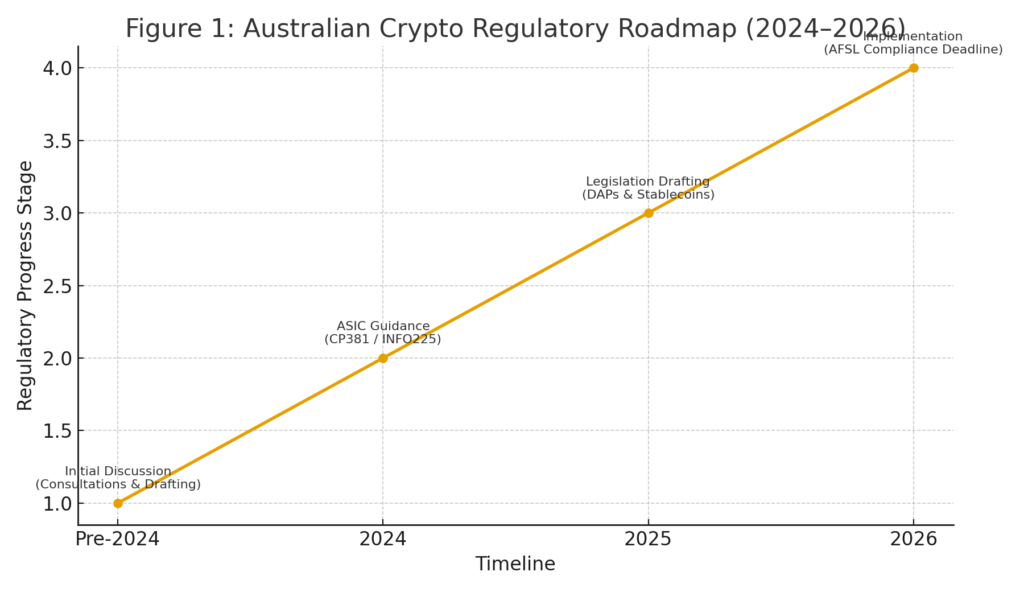

Moreover, in December 2024 ASIC published Consultation Paper 381 (CP 381) proposing updates to Information Sheet 225 (INFO 225) to expand guidance on token issuance, custody, staking, exchange and wallet operations.

The significance for crypto-businesses and token issuers is that the “label” of the asset (e.g., “token”, “coin”, “NFT”) is less important than its functional rights: does it give an interest in a managed-investment scheme, security, derivative or non-cash payment facility? If yes, it may be a financial product requiring an AFS licence.

For practitioners designing or distributing tokens (particularly EVM/ERC20 or other chain-based), this means you cannot assume “because it is a token” you are outside regulation. The rights embedded, marketing, target investor class (retail vs wholesale), custody arrangements and platform operations all matter.

2. Stablecoins & Tokenised Assets under Focus

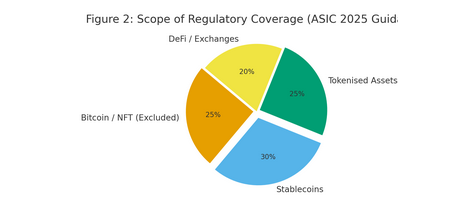

One of the major regulatory developments is ASIC’s explicit focus on stablecoins and tokenised assets as potentially regulated financial products. In CP 381, ASIC signals that fiat-backed stablecoins that are redeemable for fiat (or offer non-cash payment facilities) may fall under the financial-product regime.

Complementing this, in July 2025 ASIC granted a class-exemption (the “Stablecoin Distribution Exemption Instrument 2025/631”) for intermediaries distributing licenced stablecoins (issued by an AFS-licenced entity) from having to hold a separate AFS licence or market/clearing licence.

For token-issuers, wallet providers or platforms offering tokenised real-world assets (RWA), this is a clear signal: tokenisation is not a regulatory-free zone. If tokens represent property, rights or derivative value, they may be caught. As the Treasury’s reform statement put it: Australia’s approach will “extend existing financial services laws to key digital asset platforms, but not to all of the digital-asset ecosystem.”

For your interests—seeking new crypto assets and practical blockchain use—this means stablecoins and tokenised assets (for instance fractionalised real-estate, commodities, or revenue-sharing tokens) are increasingly legitimate targets—but they bring licensing and disclosure responsibilities.

3. Industry Reaction and Practical Challenges

The industry has broadly welcomed the clarity of ASIC’s guidance—knowing the regulatory perimeter helps in planning—but many caution that implementation will be non-trivial. For example, Blockchain APAC CEO Steve Vallas noted that while short-term certainty improves, the process of interpretation ahead of formal legislation reveals structural bottlenecks: limited regional expertise, banking/access issues, insurance constraints.

These practical issues matter: obtaining an AFS licence is time-consuming and resource-intensive, and for smaller token projects or start-ups the cost and complexity may become a barrier to entry. Similarly, banks may remain cautious about servicing crypto-businesses, even if regulated, which in turn raises operational risk.

From an investor or token-launch perspective, the takeaway is: regulatory clarity is positive, but you may see delays, higher cost-of-entry and increased oversight. For those preparing token issuance (like your ICO/presale), embedding regulatory compliance (license applicability, disclosure, custody standards) into your planning is now essential.

4. Government Reform Agenda: DAPs, Payment-Stablecoins & Sandbox

Beyond ASIC’s guidance, the Australian Government via Treasury has set out a broad 4-pillar reform agenda to position Australia as an “innovative digital-asset industry”. That includes: digital asset platforms (DAPs) regulation, payment stablecoins (treated as stored-value facilities), enhanced regulatory sandbox and tokenisation initiatives.

The “Developing an Innovative Australian Digital Asset Industry” statement (March 2025) highlights that draft legislation for the regime will be released in 2025 and transitional arrangements will be provided.

This means token platforms, wallet providers, exchange services and stablecoin issuers should prepare for a regulated regime that aligns digital-asset services with the broader financial-services framework. For practitioners seeking new crypto assets and revenue opportunities, this means: being early in compliance may confer a first-mover advantage; conversely, ignoring regulation introduces risk.

5. Implications for New Asset Launches, Tokenisation & Blockchain Use-Cases

Given the above regulatory evolution, what does this mean for those exploring new crypto assets, blockchain applications and revenue-generating projects?

5.1 Token issuance / ICO / presale projects

For projects like yours (token issuance, presale, viral mechanism, SNS integration, etc.), the Australian regulatory trajectory suggests:

- If the token is purely utility (no rights to profits, no fractionalised ownership) it may avoid financial-product classification—but this is no guarantee. The functional nature of the token matters.

- If the token is backed by real-world assets, stablecoins or offers revenue-sharing, custody, staking, or derivatives-like features, you should assess whether an AFS licence or equivalent obligation applies.

- Launching into the Australian investor base (retail) may trigger additional obligations under the Corporations Act.

- Regulatory-safe mornings (such as exemptions or transitional relief) may exist, but you should build compliance into your architecture: KYC/AML, disclosure, custody standard (see ASIC’s updated RG 133 on crypto-custody).

5.2 Tokenisation of Real-World Assets (RWAs)

Tokenisation is increasingly on regulators’ radar. Australia specifically mentions the tokenisation of assets as part of its digital-asset strategy. For someone building practical blockchain use-cases (asset-backed representation—your “Two-Extremes Model”), this is a positive signal: jurisdictions like Australia are aligning regulatory frameworks to support tokenised assets, albeit with oversight. Structuring tokenised vehicles, custody, disclosures, and investor rights must be aligned with regulation.

5.3 Stablecoins and Payment Use-Cases

Stablecoins and payments-blockchain use-cases are also favored by the regulatory agenda. The ASIC exemption for intermediaries distributing licensed stablecoins signals that regulated stablecoins may enjoy smoother market access. For blockchain applications oriented to payments, micro-transactions, tokenised consumption or value-flows, Australia seems to be making a bet on practical use-cases.

In short: if your project involves a stablecoin, payments token, or tokenised value-flow on-chain, align your design to regulatory requirements early (licensing, disclosure, custody, AML/KYC).

6. Recommendations for Blockchain Practitioners & New Asset Hunters

- Map the regulatory perimeter early: For your token or asset, ask: What rights does it confer? Does it give ownership, revenue, or derivative exposure? If yes → likely financial product. Use ASIC’s INFO 225 and CP 381 as checklists.

- Design for disclosure and custody: Regardless of jurisdiction, designing token mechanisms with transparency, audited disclosures, robust custody (as per RG 133) is best practice.

- Select geographies strategically: Australia signals a mature regulated regime that balances innovation and investor protection—if you plan global rollout, meeting these standards may credibly support other markets.

- Use compliance as market differentiator: Early alignment with regulated frameworks (licensing readiness, stablecoin design, tokenised asset mechanisms) may help attract institutional investors or partners and reduce execution risk.

- Revisit business model for compliance risk: If you rely on “yield-bearing tokens”, staking, loans, wrapped assets—these are under increasing scrutiny. Make sure you design the mechanics, rights and disclosures accordingly.

- Monitor legislation rollout: The draft laws for DAPs and payment stablecoins are forthcoming; timing is important for transitional relief and market entry.

Conclusion

Australia is at a regulatory inflection point in the crypto/digital-asset space. With ASIC clarifying how existing financial-services laws apply to tokens, stablecoins and tokenised assets, and the government moving toward a full-fledged regulatory framework for digital-asset platforms, the environment is shifting from regulatory uncertainty to structured opportunity.

For those seeking new crypto assets, revenue-generating blockchain projects, or practical tokenised use-cases, this provides a compelling signal: jurisdictions are no longer simply ignoring crypto—they are integrating it. That means opportunity—but also responsibilities. Token issuers, platform operators and investors must navigate licensing, disclosure, custody and investor-protection obligations if they wish to scale sustainably.

In your case—preparing for a token ICO/presale, with viral mechanisms, SNS integration, no-code platforms, and a dual “Asset-Backed Representation / Autonomous Trust Tender” model—the time to embed compliance and regulatory design is now. The Australian evolution exemplifies how serious jurisdictions are aligning blockchain innovation with financial-services frameworks—so being early, transparent and compliant may well become a competitive advantage.