Main Points :

- Tesla booked approximately $80 million in profit from its Bitcoin holdings in Q3.

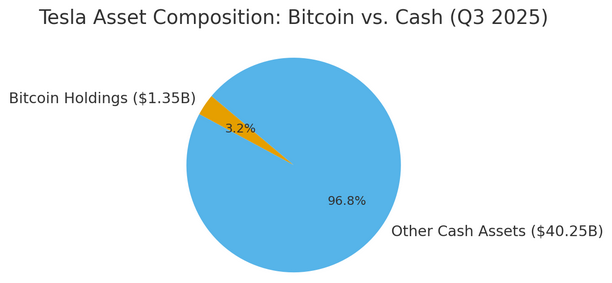

- The company holds about 11,509 BTC, valued at roughly $1.35 billion at quarter-end.

- New accounting rules by the Financial Accounting Standards Board (FASB) require recognition of digital-asset gains and losses each quarter.

- Corporate Bitcoin treasury strategies are increasingly common in 2025: more firms are adopting BTC on their balance sheets.

- Risks remain significant: volatility, accounting and tax implications, regulatory uncertainty.

- For blockchain practitioners and crypto-seekers, corporate behaviour signals maturity and may guide where next-wave opportunities arise.

1. Tesla’s Q3 Bitcoin Gain and Its Implications

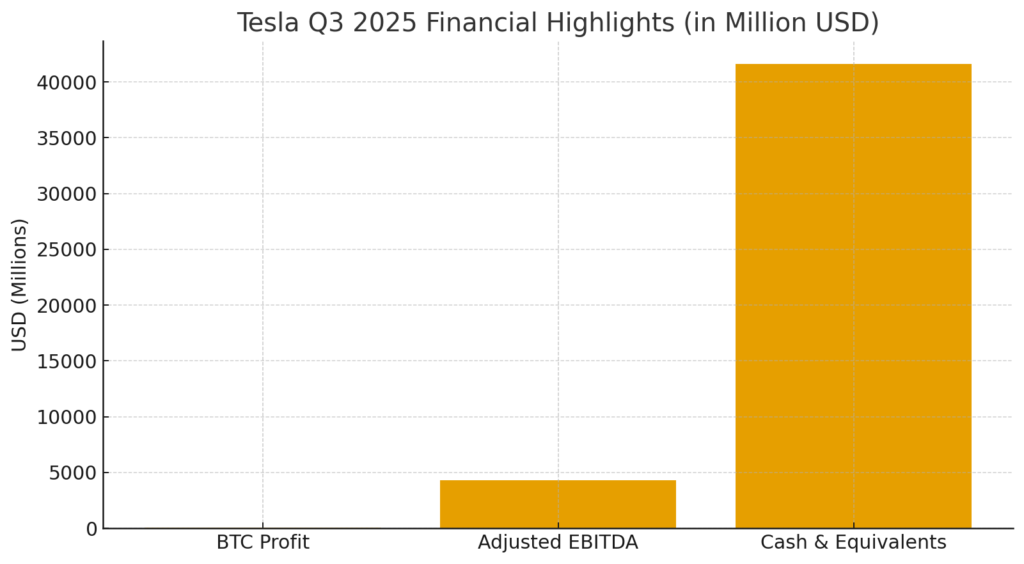

In its third quarter, Tesla, Inc. announced that it recognised about $80 million of profits from its Bitcoin holdings, thanks primarily to Bitcoin’s price appreciation over the period. The firm reports maintaining its holdings at around 11,509 BTC, which at the end of Q3 was valued at about $1.35 billion.

Tesla’s core business results were solid in terms of revenue—its Q3 revenue came in at about $28.1 billion, beating analyst expectations. However, its adjusted EPS (excluding digital-asset gains) was $0.50, slightly below the consensus estimate of $0.54. With the crypto gain, the net results benefit from this extra line item. The fact that Tesla did not alter its Bitcoin holdings during the quarter signals a deliberate decision to hold and recognise upside rather than trade.

From a practical viewpoint for professionals interested in blockchain and crypto-assets, this implies that large corporates view Bitcoin not only as a speculative asset but as a treasury reserve. Tesla’s example may encourage others to consider digital-asset allocations, especially given regulatory and accounting pathways are now clearer.

2. The Accounting Shift That Enables Recognition

A key enabler of Tesla’s profit recognition is the recent change by the Financial Accounting Standards Board (FASB). Under the previous rules, companies that held Bitcoin and similar digital assets were required to treat them as “indefinite-lived intangible assets.” That meant unrealised losses had to be recognised (via write-downs) but unrealised gains could not be booked unless the asset was sold.

With the new rules (notably ASU 2023-08), companies can mark digital-asset holdings to fair value and report gains. That change made Tesla’s $80 million gain possible. However, the shift also opens up risks for others: for instance, large unrealised gains may trigger tax or minimum tax liabilities in the future.

For a practicioner, this means that if you are advising companies or investigating digital-asset use in corporate treasuries, you must be mindful of accounting and tax treatment—an allocation to Bitcoin is no longer off-balance-sheet but must be fully integrated into corporate finance and compliance.

3. Broader Corporate Adoption of Bitcoin in 2025

Tesla’s move is not isolated. Data show that corporate or institutional Bitcoin treasury adoption is gaining meaningful momentum in 2025. According to BusinessInitiative.org, business inflows into Bitcoin from Jan-Aug 2025 summed to about $12.5 billion, already exceeding the full year of 2024.

Furthermore, the number of publicly-traded companies holding Bitcoin jumped about 38 % in Q3: from 124 to 172 firms. This suggests a structural shift: Bitcoin is increasingly being treated as part of corporate strategy rather than just speculation.

For those seeking new crypto-assets or business models, this trend is meaningful. Corporate adoption signals maturer markets, deeper liquidity, and perhaps slower hype cycles—but potentially more stable institutional demand.

4. Risks and Strategic Considerations for Blockchain Practitioners

Even as corporate Bitcoin adoption grows, there are significant caveats and risks worth noting:

- Volatility risk: Bitcoin remains highly volatile. A large corporate holding can amplify the company’s earnings swings if prices move sharply.

- Tax and regulatory risk: The new accounting rules open up risk of tax exposure, especially for unrealised gains and the corporate alternative minimum tax (CAMT) in the U.S.

- Liquidity and operational risk: Holding digital-assets at scale involves custody, security, and operational infrastructure. For companies not well-versed in crypto, this may be non-trivial.

- Strategic fit: For blockchain professionals, advising or building business models around corporate crypto use means aligning digital-asset strategies with broader business goals—not just “buying Bitcoin” but integrating it meaningfully (e.g., combining with DeFi, tokenization of assets, treasury diversification).

Therefore, if you are working in the blockchain domain or investigating next-wave crypto investments, you should evaluate: (a) whether the business model leverages corporate treasury and digital-asset synergy, (b) how accounting/tax rules apply in that jurisdiction, and (c) how suitably the blockchain solution is integrated into the enterprise’s core operations.

5. What This Means for Crypto Investors and Blockchain Builders

For your audience—those looking for new crypto assets, revenue sources, or practical blockchain use cases—Tesla’s Bitcoin-gain story offers several take-aways:

- The institutionalisation of Bitcoin continues: more companies are holding Bitcoin, which may reduce the all-or-nothing speculative nature and shift toward strategic allocations.

- Blockchain use in the corporate treasury is an actionable use case: not just building apps, but deploying Bitcoin as a corporate asset. This bridges the gap between “blockchain innovation” and real-world balance sheet strategy.

- For investors, the fact that companies like Tesla are publicly discussing Bitcoin holdings adds transparency and legitimacy to digital-asset exposure. It may mean less extreme tail-risk but also lower reward multiples than pure speculation.

- For business builders, there may be emerging opportunities around custody infrastructure, treasury-asset management for crypto, tokenization services (e.g., firms helping corporates adopt digital assets), and audit/accounting services tailored to blockchain assets.

- If you’re exploring new crypto assets beyond Bitcoin, the corporate treasury trend hints that assets which support enterprise use cases (tokenized assets, infrastructure tokens, stablecoin ecosystems) may become more interesting—especially if they link to treasury or financial-service workflows.

6. Recent Market & Holder-Behaviour Trends (Beyond Tesla)

Some additional recent data of interest:

- According to CoinDesk, short-term holders (defined as investors having held Bitcoin for less than ~155 days) currently hold around 18 % of circulating supply, down from about 22 % in previous peaks. This suggests speculative momentum may be moderating, which could influence how corporate holders behave.

- Academic work (Di Wu 2025) shows Bitcoin’s correlation with equity markets (e.g., the S&P 500) has grown, with peaks of ~0.87 correlation in 2024. For investors, that means Bitcoin is becoming less of an “un-correlated hedge” and more integrated into market dynamics.

- The “bitcoin treasury” companies phenomenon is gaining academic treatment: B K Meister (2025) discusses how companies amass large Bitcoin holdings and how leverage, corporate debt, and risk models tie into that. From a builder/investor vantage, this offers insight that corporate crypto-allocations are not just purchases—they are embedded in broader financial architecture (debt, hedging, corporate strategy).

Summary & Final Thoughts

In summary, Tesla’s announcement of an ~$80 million profit from its Bitcoin holdings in Q3 underscores a broader shift: digital assets are increasingly being adopted in corporate treasuries, no longer relegated to niche speculation. The accounting rule changes by the FASB have unlocked this possibility, but they also create new tax, regulatory and risk-management considerations. For blockchain practitioners, this evolution opens up real business use cases—ranging from treasury-asset management to tokenization platforms and corporate custody services. For crypto investors, the institutionalization trend may reduce extreme upside but provides deeper liquidity and legitimisation of digital-asset exposure.

As you explore new crypto assets or build blockchain-related business models, consider how the corporate world is treating digital assets—not just as speculative tokens, but as strategic reserves. Look for assets and platforms that bridge the gap between enterprise treasury operations and the decentralized-finance world. And always keep in mind: adoption is gaining traction, but risk remains very real.