Key Takeaways :

- Despite Bitcoin’s record highs, most investors remain unexposed to crypto — meaning considerable runway remains.

- Institutional flows and regulatory clarity (e.g. U.S. stablecoin / crypto laws) are becoming stronger tailwinds.

- Altcoins like Ethereum and Solana are positioned to evolve as large tech platforms, rather than mere speculative tokens.

- Tokenization of real-world assets and DeFi yield strategies face structural challenges but promise a new frontier.

- Macro tailwinds, ETF booms, and global demand point to sustained growth, though execution, liquidity, and regulation are critical.

Introduction: A Bold Claim from Pantera’s Cosmo Jiang

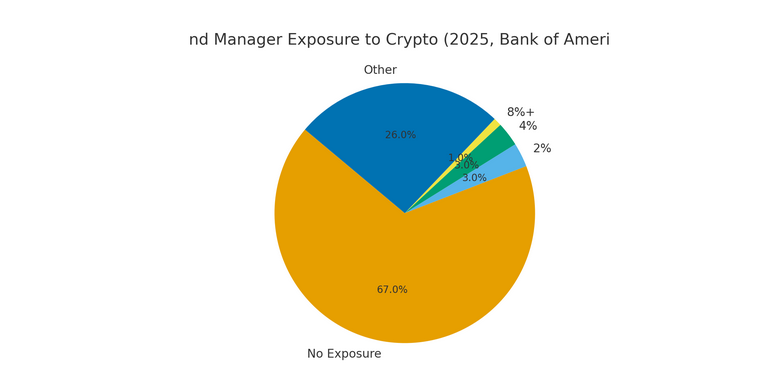

In a recent interview with CNBC, Cosmo Jiang, General Partner at Pantera Capital, asserted that it is not too late to invest in crypto. He referred to a Bank of America survey showing that over 60% of investors currently hold zero exposure to digital assets. In other words, even at Bitcoin’s all-time highs, most capital is still on the sidelines. (Pantera’s view suggests that the narrative of “everyone who wanted Bitcoin already owns it” is flawed.)

Jiang’s point is that the crypto market has been in a phase of legitimization of Bitcoin, and now is entering a stage where altcoins and supporting infrastructure may take off, especially under clearer regulation. He highlighted that laws passed or debated in the U.S., such as the GENIUS Act and the Clarity Bill, may help provide frameworks for stablecoins and crypto market structures.

Pantera’s optimism prompts a question: in 2025, what trends support the idea that there’s still room for growth — and where should a serious crypto investor look?

Institutional Adoption: Gaps, Momentum, and Correlation

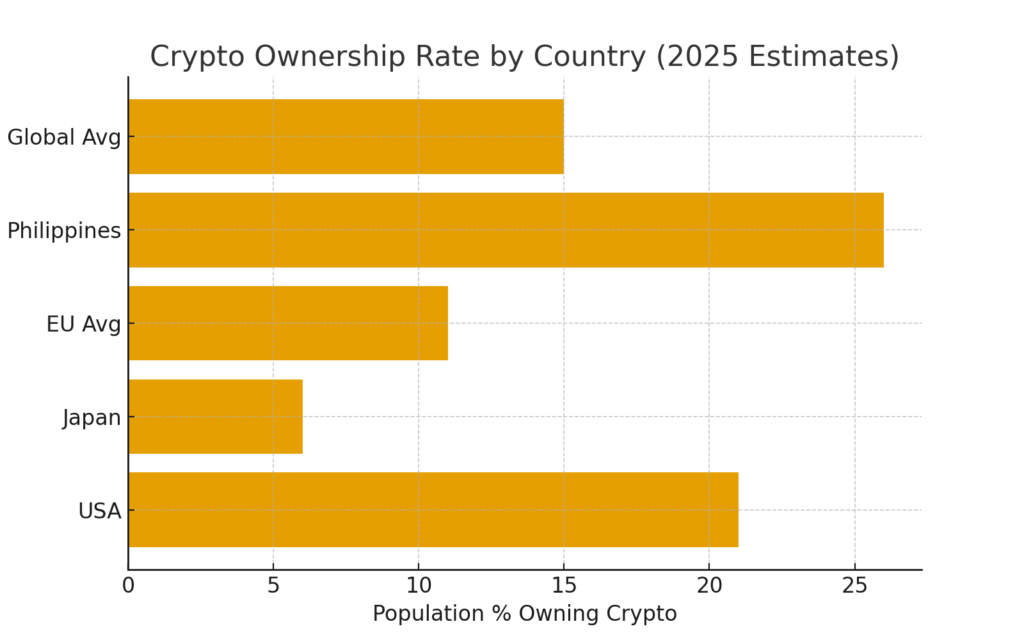

Still Much Zero Exposure

Jiang’s invocation of “60% of investors with zero exposure” aligns with other data showing low penetration of crypto among retail and institutional investors. For example, reports indicate that only 21% of American adults hold some crypto assets, and globally, many regions show adoption far below saturation.

From the institutional side, a 2025 survey by EY shows that many institutional investors have increased their allocation to digital assets in the last year and intend to continue doing so. Meanwhile, industry commentary emphasizes that the current wave is being driven by institutional adoption and market momentum.

Captured Correlations & Portfolio Integration

Bitcoin’s evolving role is increasingly intertwined with traditional markets. A recent academic study shows that its correlation with major equity indices (e.g. S&P 500, Nasdaq) has risen, particularly around key institutional milestones.

This implies that crypto is shifting from purely “alternative” status toward a more integrated piece of modern portfolios. For investors seeking diversification, risk management, and returns beyond traditional assets, crypto is becoming less of a wild outlier and more of a testable allocation class.

ETF Inflows & Active vs Passive Strategies

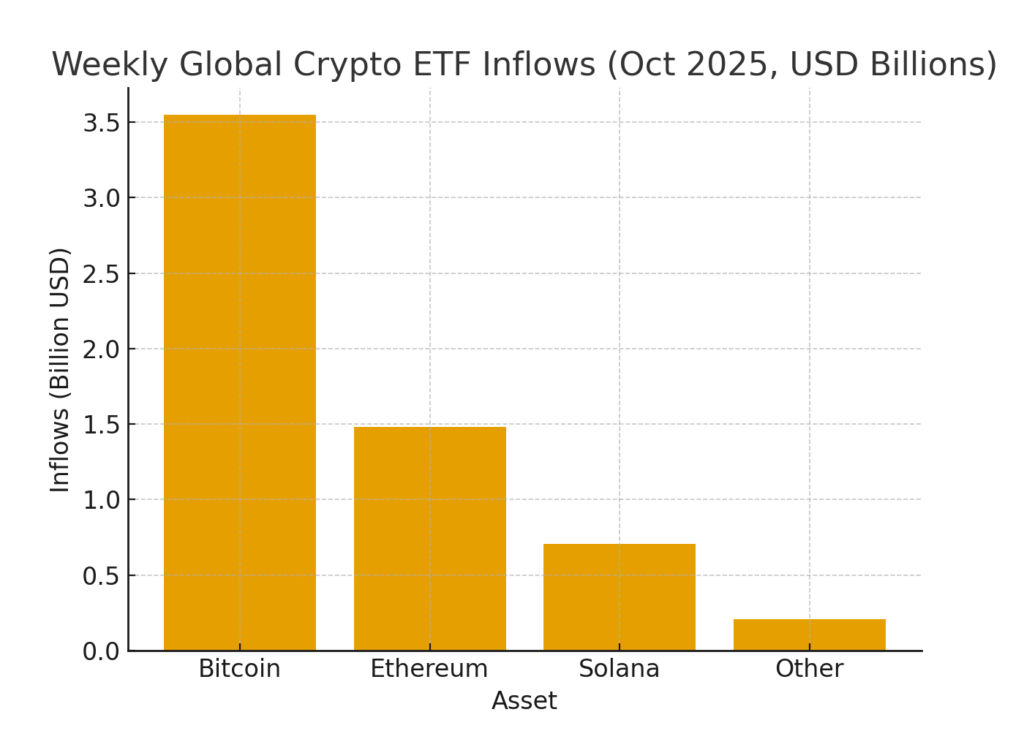

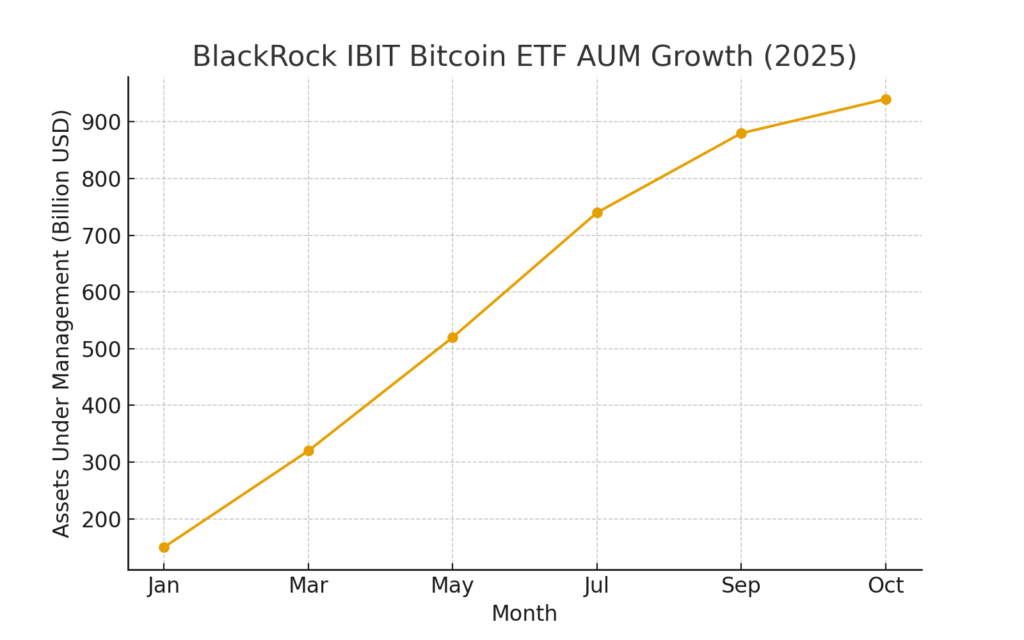

One powerful indicator is the record ETF inflows into crypto funds. In the week ending October 4, 2025, global crypto ETFs saw roughly $5.95 billion of new capital inflows, with about $3.55B into Bitcoin, $1.48B to Ether, and $706M to Solana.

Jiang made a distinction between passive exposure (simply buying a spot ETF) and active management, which might layer yield strategies (staking, DeFi) or dynamic asset allocation. He believed these active maneuvers justify valuation premiums in certain crypto asset managers.

However, despite this activity, some crypto treasury companies have cooled their pace of accumulation—September 2025 saw corporate crypto purchases drop to their lowest levels in months.

Altcoins as Platforms: Ethereum, Solana, and Beyond

The Shift from Speculation to Infrastructure

Cosmo Jiang projects that Ethereum and Solana may evolve into mega-cap tech platforms in their own right, beyond simple “coins.” The idea is that these chains will host applications, tokenization, stablecoins, and DeFi infrastructure at scale.

Supporting this, many institutional players are now eyeing Ethereum’s architecture for tokenizing traditional assets, enabling yield strategies, and anchoring smart contract ecosystems.

Challenges & Opportunities in Altcoin Architecture

However, scaling is nontrivial. Cross-chain connectivity, gas fees, consensus innovations, and security remain significant hurdles. Several industry voices argue that regulatory clarity will be key for altcoins to flourish without existential uncertainty.

Moreover, some altcoins built on new L1 or L2 architectures must compete with incumbents while demonstrating scalable utility (e.g. for DeFi, gaming, tokenization). The winners may be those who combine protocol-level innovation with developer ecosystem traction.

Tokenization & Real-World Assets (RWAs): Promise vs Liquidity

One of the more ambitious frontiers is the tokenization of real-world assets — real estate, private credit, government bonds, etc. The promise is fractionalization, global access, programmable settlement, and 24/7 markets.

Yet a 2025 academic paper highlights a major friction: liquidity. Many tokenized assets show low trading volume, limited secondary markets, and long holding periods. Structural barriers include custody concentration, regulatory restrictions, whitelisting, opacity of valuations, and lack of decentralized trading venues.

To make RWA tokenization viable at scale, progress must occur not only in technical infrastructure but in legal, institutional, and market-making layers. Hybrid models (on-chain settlement + off-chain market makers) may help bridge the gap.

Macro & Regulatory Tailwinds in 2025

U.S. Legislation: GENIUS Act, CLARITY, & Reserve Proposals

A major supportive factor is the evolving U.S. regulatory landscape. The GENIUS Act (passed in mid-2025) aims to regulate stablecoins. Meanwhile, the Clarity Bill, when enacted, would define rules for crypto market structure.

Another striking development: the U.S. government is exploring a “strategic digital asset reserve”, naming Bitcoin, Ethereum, Solana, XRP, and Cardano as potential assets. This signals a shift from viewing digital assets as fringe to potentially part of national balance sheet policy.

Global & Banking Integration

Institutionally, banks are stepping in. For instance, Standard Chartered recently launched spot trading desks for Bitcoin and Ether targeting institutional clients, integrating those services into existing FX trading infrastructure.

At the same time, flows into crypto ETFs in multiple geographies are breaking records, signaling broadening demand across regions.

Macro Pressures & Market Risks

Crypto does not live in a vacuum. Inflationary pressures, U.S. dollar strength/weakness, central bank interest rate policies, and equity volatility all affect flows. As crypto correlation with equities rises (as studied earlier), the space becomes more exposed to broader macro cycles.

Moreover, regulatory missteps, security exploits, or sudden deleveraging remain persistent risks. The market’s promise will only be delivered if execution, risk controls, and structural robustness align.

What It Means for Investors: Strategies & Ideas

Diversified Core + Opportunistic Layer

A prudent approach may be to allocate a core position to “blue-chip” assets like Bitcoin and Ether (via ETF or custody), and reserve a smaller portion for higher-risk, higher-upside bets in altcoins, protocols, or tokenization plays.

Yield & Active Layer

Given Jiang’s distinction, investors may seek active strategies such as staking, restaking, liquidity provision, DeFi yield farming, or protocol-level yield capture. These can enhance returns over plain spot holding — but also carry operational and smart contract risk.

Focus on Infrastructure, Not Just Tokens

Because so much of long-term value may accrue to infrastructure, bridges, middleware, and tokenization platforms, it is wise to look beyond speculative memecoins and toward protocols enabling cross-chain connectivity, oracle services, stablecoin rails, and identity infrastructure.

Monitor Regulation and Liquidity

Stay attuned to regulatory developments, especially in major jurisdictions (U.S., EU, Asia). Also keep an eye on liquidity metrics (on-chain volume, order book depth), particularly for newer tokenized assets.

Closing Summary

The view floated by Pantera’s Cosmo Jiang — that it is not too late to invest in crypto — is bold but reasonably grounded in the data. Even at record-high Bitcoin prices, most investors remain outside the market, suggesting the bulk of institutional or retail capital has yet to flow in.

At the same time, 2025 is showing signs of maturation: massive ETF inflows, clearer regulation (e.g. GENIUS Act, Clarity Bill), and banking integration point toward a more robust infrastructure. Altcoins like Ethereum and Solana are increasingly viewed not just as speculative bets, but as foundational tech platforms. Meanwhile, tokenization of real-world assets holds enormous promise — but must overcome liquidity and structural constraints to truly deliver.

If you are seeking the next source of crypto-driven returns, this is not a simple “buy and hold everything” era. Rather, the opportunity lies in identifying which platforms, yield strategies, and tokenization models can navigate regulation, liquidity bottlenecks, and macro cycles. The runway is long, but execution will matter more than ever.

Let me know if you’d like a version of this article with charts, token-level case studies, or more detailed trade ideas.