Main Points :

- Conflict ratchets up: SWIFT’s CIO compares private tokens to fax machines, igniting pushback from XRP community

- Ripple and XRP advocates argue superiority of public, permissionless architecture over bank-controlled systems

- SWIFT responds with plans to build its own shared blockchain ledger with global banks and ConsenSys

- XRP is reportedly making inroads into SWIFT’s network via fintech partners, bypassing direct collaboration

- Ripple expands its stablecoin infrastructure via acquisitions and regulatory moves

- The competition is reshaping the future of cross-border payments, touching both technical and regulatory domains

1. Renewed Flashpoint: The “Fax Machine” Remark and Reactions

A new flashpoint in the longstanding tension between Ripple / XRP and SWIFT erupted on October 4, 2025, when Tom Zschach, Chief Innovation Officer at SWIFT, posted on X (formerly Twitter) a provocative analogy:

“Calling a private token a ‘bridge currency’ is like calling a fax machine the Internet. Similar in shape maybe, but functionally utterly different.”

He added:

“Fast? Sure. Revolutionary? Only if you’ve never used Wi-Fi.”

Although Zschach did not explicitly name XRP or Ripple, the metaphor was widely interpreted—and criticized—by the XRP community as a direct jab at Ripple’s bridge token model.

In response, XRP supporters and former Ripple executives pushed back, emphasizing that XRP is public, permissionless, and transparent, rather than a proprietary “private token.” They argued this mischaracterization betrays a fundamental misunderstanding of blockchain.

Some voices within the “XRP Army” mockingly reframed the remark: if SWIFT’s infrastructure is the fax machine, then XRP is the value-internet. Others questioned why, if blockchain were unimportant, SWIFT has only recently begun prototyping its own ledger.

Thus, what might have started as a rhetorical flourish has instead amplified the symbolic clash between legacy financial messaging rails and emergent decentralized settlement networks.

2. SWIFT’s Response: Building a Blockchain Ledger

Rather than stay passive, SWIFT has counterattacked by pivoting toward blockchain itself. On September 29, 2025, SWIFT formally announced it is partnering with Consensys and over 30 global financial institutions to develop a shared digital ledger infrastructure.

2.1 Goals and Architecture

- The initial prototype focuses on real-time, 24/7 cross-border payments.

- SWIFT describes this ledger as a secure, real-time log that will record, sequence, and validate transactions, governed via smart contract enforcement of rules.

- Interoperability is key: the ledger is intended to coexist with existing and emerging systems, bridging messaging rails and tokenized networks.

This move signals SWIFT’s ambition to evolve from purely a messaging network to a settlement-layer infrastructure supporting tokenized value transfers, including stablecoins and tokenized assets.

2.2 Consortium Strategy & Timeline

- The prototype phase is underway with participating banks undergoing tests of architecture, consensus models, ISO 20022 integration, and latency optimization.

- There is no fixed timetable yet for full rollout; decisions will depend on testing outcomes and compliance requirements.

Notably, SWIFT’s expansion into blockchain does not immediately guarantee dominance. Observers warn potential fragmentation risks, and question whether the shared ledger will achieve broad adoption given incumbents have entrenched positions.

3. XRP’s Strategy: Penetrating SWIFT Indirectly

Ripple does not appear to be waiting for SWIFT’s approval. Analysts have documented how XRP is already penetrating SWIFT’s network through indirect paths via fintech intermediaries.

3.1 Fintech Bridges Within the SWIFT Realm

A thread by researcher “SMQKE” outlines seven fintech firms—ACI, EastNets, Finastra, TAS, Temenos, Volante, CGI, and also Thunes—that already operate ISO 20022–compliant messaging systems. These act as entry points to SWIFT’s network for XRP liquidity.

Because these firms already handle cross-border messaging, they can route XRP-based liquidity into SWIFT-connected banks without a formal XRP-SWIFT partnership. In this model, XRP becomes a backend bridge asset, hidden from view in some transactions.

3.2 Ripple’s SWIFT Integration Moves

- Ripple’s relationship with Thunes is often cited as a key step: Thunes has integrated its Pay-to-Banks service into SWIFT’s network, linking XRP to ~11,000 banks worldwide.

- Other integrations include partnerships with Finastra and Temenos, aligning real-time settlement infrastructure with legacy banking systems.

- The SEC’s recent issuance of a no-action letter allowing registered advisers and broker-dealers to custody XRP further unlocks institutional demand.

In effect, XRP is weaving itself into the traditional financial plumbing by sidestepping the need for direct SWIFT endorsement, strengthening its utility without waiting for legacy institutions to fully embrace it.

4. Ripple’s Ecosystem Expansion & Regulatory Posture

While the SWIFT clash draws headlines, Ripple is also proactively building out its broader infrastructure and positioning itself for the regulatory future.

4.1 Stablecoin Infrastructure & Acquisitions

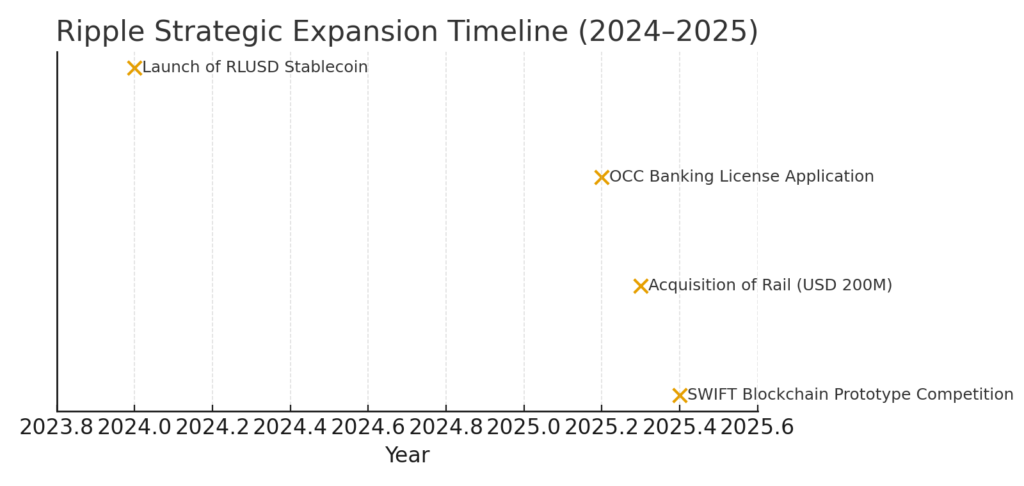

In 2024, Ripple launched its own dollar-pegged stablecoin, RLUSD. By October 2025, RLUSD’s market cap had grown to ~$800 million, adding a native on-chain USD component to its ecosystem.

To further solidify its position, Ripple in August 2025 announced a $200 million acquisition of Rail, a Toronto-based stablecoin payments platform. The acquisition is expected to close in Q4 2025 (pending regulatory approvals). Rail brings cross-border payments, virtual account infrastructure, and back-office automation to Ripple’s stack.

This move positions Ripple to enhance its turnkey stablecoin payments solution and accelerate adoption in regulated environments.

4.2 Banking License Ambitions

Ripple CEO Brad Garlinghouse disclosed that Ripple has applied for a federal banking license via the Office of the Comptroller of the Currency (OCC). If granted, Ripple would gain access to Federal Reserve master accounts and direct settlement capabilities with the U.S. central banking infrastructure.

This regulatory ambition, if realized, could represent a transformational step—shifting Ripple from a payments-layer company to a regulated financial institution.

4.3 Market Reactions & Price Dynamics

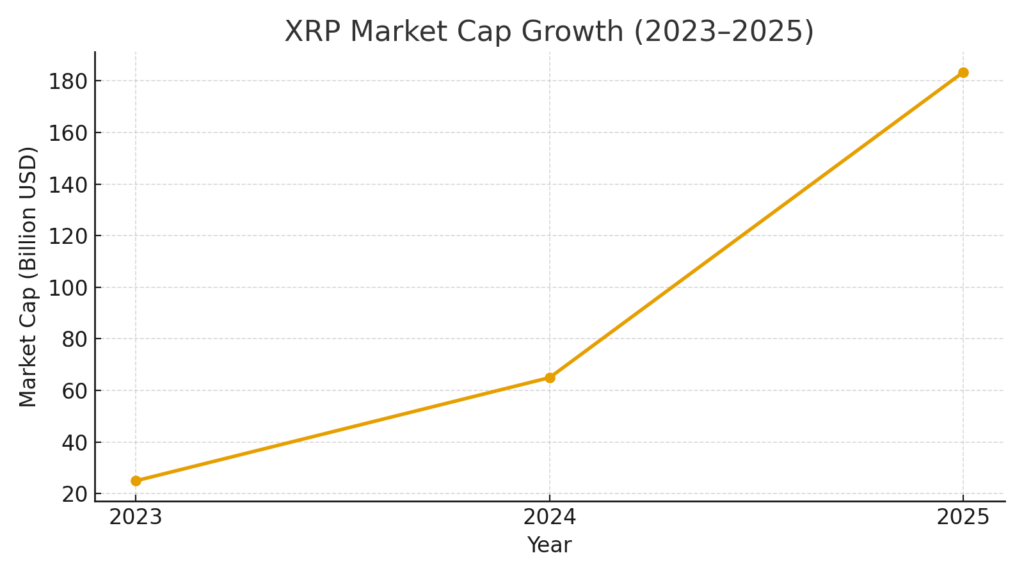

These strategic pivots have fueled investor optimism. On October 5, 2025, XRP’s market cap briefly reached ~$183.4 billion, reportedly surpassing that of BlackRock.

Moreover, technical analysis suggests that XRP may be near a breakout above $3.15, which some traders view as a trigger for further upside toward ~$3.50. Recent upgrades of SWIFT and Fedwire are also cited as favorable tailwinds for blockchain-enabled settlement tokens like XRP, Hedera (HBAR), and Stellar (XLM).

5. Challenges, Critiques & Competitive Landscape

Even as both sides marshal arguments and infrastructure, the path ahead is neither smooth nor uncontested.

5.1 Technical & Adoption Risks

- Fragmentation risk: The coexistence of multiple blockchains and messaging rails could lead to siloed ecosystems rather than convergence.

- Interoperability and standardization: SWIFT’s new ledger must integrate seamlessly with legacy systems and multiple token protocols; misalignment could slow uptake.

- Performance constraints: Ensuring scalability, latency, and settlement atomicity remain major design challenges in real-world conditions.

5.2 Competitive Threats

- SWIFT’s own blockchain initiative is now a direct competitive frontier. Even if Ripple’s solution is more mature, SWIFT’s distribution reach and institutional relationships give it a formidable position.

- Other blockchain consortia—such as Fnality, Canton Network, or mBridge—are also advancing institutional-grade settlement infrastructure.

- For example, Fnality recently raised $136 million, backed by giants like Bank of America and Citi, to expand its blockchain payments ecosystem.

- The Canton Network aims to support regulated financial institutions in interoperable, privacy-preserving settlement workflows.

- Legacy banks may prefer to adopt SWIFT’s built-in ledger rather than integrate with external tokens, favoring minimal disruption to existing operations.

5.3 Regulatory & Political Hurdles

- Regulatory frameworks around stablecoins, cross-border compliance (KYC/AML), and token settlement vary globally.

- Ripple’s pursuit of a banking license introduces regulatory exposure and potential constraints on its operating flexibility.

- The balance between decentralization and compliance is inherently fraught when dealing with institutional networks.

Conclusion: A Clash of Railroads vs. the Value Highway

The evolving tension between Ripple / XRP and SWIFT is more than PR drama—it encapsulates a structural contest over the future architecture of global finance. On one side is a legacy messaging giant making a cautious move into blockchain. On the other is an insurgent, token-native network pushing for the high ground of value settlement itself.

Ripple’s strategy is multifaceted: building permissionless infrastructure, forging fintech integrations, expanding stablecoin capabilities, and seeking regulated legitimacy. Meanwhile, SWIFT is reinforcing its dominance by constructing a new shared ledger on top of its existing reach—blurring the lines between messaging and settlement.

For readers exploring new crypto opportunities or real-world blockchain use cases, several implications emerge:

- XRP’s path into established finance may increasingly rely on indirect connectivity via fintech bridges rather than frontal assaults.

- The success of SWIFT’s ledger will depend not just on technology, but on governance, adoption incentives, and institutional alignment.

- Tokens that combine utility, compliance-readiness, and interoperability may have an edge in the next wave of blockchain adoption.

In sum, we are witnessing a strategic race: can Ripple leverage its token and ecosystem innovation to outpace SWIFT’s incumbency and coopt its future? Or will SWIFT’s pivot into blockchain subsume or neutralize that threat? The answer may well define the settlement layer of tomorrow’s global financial system.