Main Points :

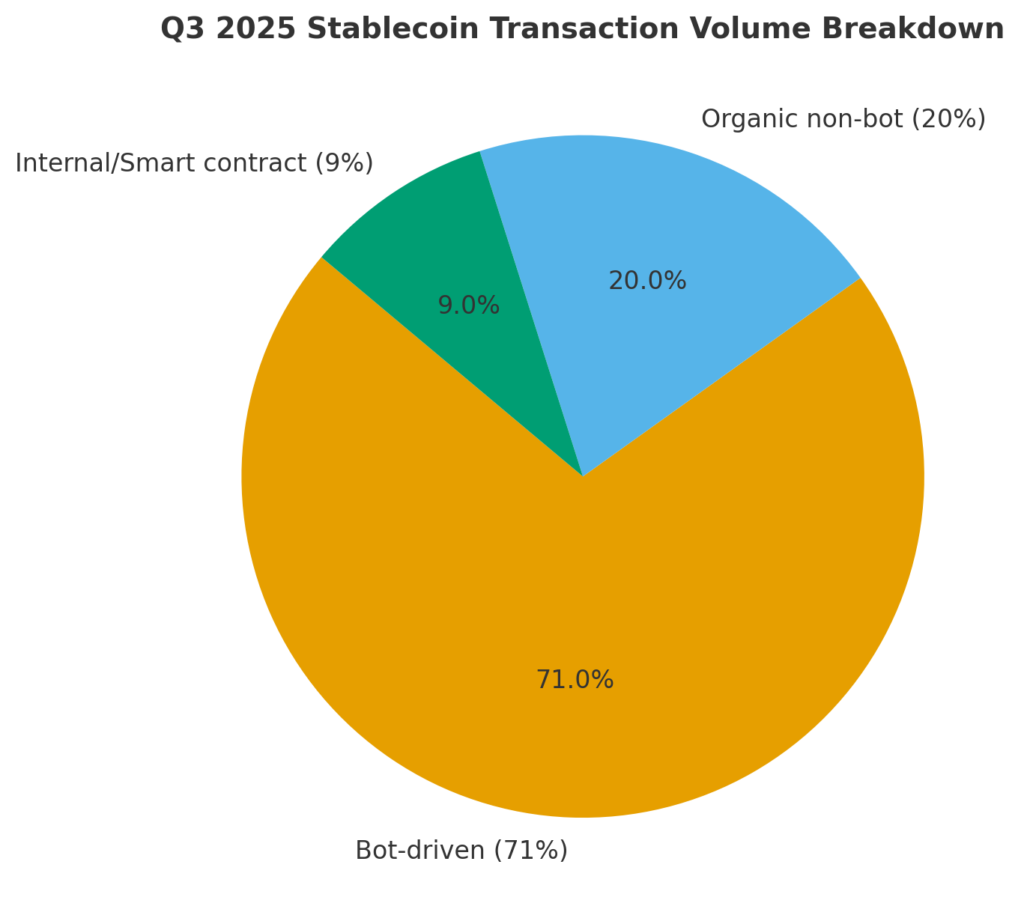

- In Q3 2025, stablecoin on-chain transfer volume reached a record $15.6 trillion, with ~71 % attributed to automated bots.

- Non-bot “organic” transfers were only ~20 %, with internal smart contract / exchange operations ~9 %.

- Retail-sized transfers (≤ $250) also hit all-time highs, pointing to growing real usage beyond bot markets.

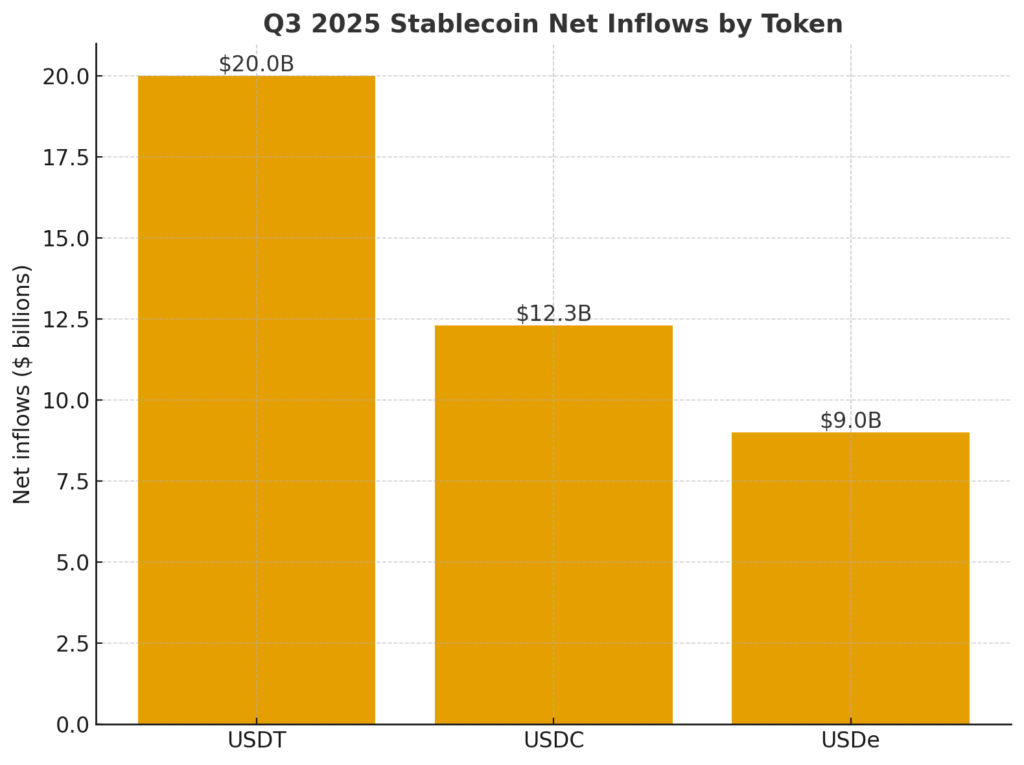

- Q3 saw net inflows of stablecoins > $46 billion, led by USDT (~$20B), USDC (~$12.3B), and synthetic stablecoin USDe (~$9B).

- Bots include high‐frequency trading, MEV bots, and unlabeled algorithmic accounts; much of the bot volume may not reflect “economic” usage.

- Policymakers and analysts face growing pressure to distinguish bot-driven volume from real adoption for accurate metrics, oversight, and risk evaluation.

- Recent academic research points toward hybrid protocols (AI, algorithmic stabilization, cross-chain designs) as likely directions for next-gen stablecoin infrastructure.

The Q3 2025 Explosion in Stablecoin Activity

In what many crypto observers are calling a shock to conventional metrics, Q3 2025 saw on-chain stablecoin transfers balloon to $15.6 trillion, the highest single quarter ever recorded. That scale is astonishing in itself — but even more remarkable is that 71 % of that volume appears to be driven by automated bots executing predefined trading or liquidity strategies.

“Organic” non-bot transactions — those that more plausibly correspond to human users moving funds, remittances, payments, or exchanges — made up only about 20 % of total volume. The remaining 9 % is attributed to internal smart contract flows or exchange internal operations.

This dichotomy challenges normative assumptions about crypto activity: large aggregate numbers may mask the fact that real economic usage — the kind of stablecoin flows consistent with payments, user transfers, merchant adoption or cross-border remittances — might remain a smaller fraction of the “total.”

What kinds of bots dominate?

According to CEX.io analyst Ilya Otychenko, much of the bot volume comes from unlabeled high-frequency bots — accounts doing over 1,000 trades per month and more than $10 million in volume. Some bots are involved with MEV strategies (extracting value from on-chain order sequencing) or interacting with DeFi protocols, but those represent less than half of the total bot-driven volume.

Because bot activity can include wash trading (circular trades that inflate metrics without net change) or algorithmic market making that doesn’t reflect real demand, analysts caution that not all bot volume equals “real adoption.”

Thus, distinguishing among bot types (market-making bots, arbitrage bots, MEV bots, wash trading bots) becomes critical for assessing the health of the stablecoin ecosystem.

Retail Uptake: Small Transfers Surge

While bots dominate large volume flows, the retail side of stablecoin use is showing its strongest growth ever. Transfers under $250 — a proxy for user-level or small payments — hit new all-time highs in Q3 and September specifically.

At the current trajectory, retail transfers are expected to exceed $60 billion by the end of 2025. Within that sub-$250 segment, ~88 % of the transactions are tied to exchanges (i.e. deposits, withdrawals, conversions) per internal CEX.io data.

However, interestingly, the share of non-trading uses (remittances, payments, fiat cash-outs) is growing: exchanges report a >15 % year-to-date growth in non-trading volume in 2025. This trend suggests that stablecoins are creeping into their intended roles (medium of exchange, remittance tool, payout instrument), not just trading instruments.

Thus, the picture is one of dual dynamics: massive bot activity inflating volumes, but simultaneously a grassroots increase in real-user transfers at the edges of the system.

Capital Flows and Token Dynamics

Beyond transfer flows, Q3 also saw significant net inflows — the difference between stablecoin issuance and redemption — totaling > $46 billion.

- USDT (Tether) led with about $20 billion net inflow

- USDC (Circle) followed with $12.3 billion

- USDe (Ethena synthetic stablecoin) also gained attention with $9 billion inflow

These flows reaffirm that despite any growing critiques, dollar-pegged stablecoins remain the liquidity backbone of crypto markets. The rise of USDe is particularly notable as synthetic or yield-oriented stablecoins gain traction.

On the network side, Ethereum (L1 and its rollups) hosted ~69 % of new stablecoin issuance in the quarter. Meanwhile, some networks like Arbitrum and Hyperliquid’s L1 saw strong growth as DeFi integrations attracted more liquidity.

Interestingly, USDT overtook USDC in DEX trading volume during Q3, crossing $100 billion monthly volume for the first time. This overturns a prior pattern where USDC had stronger positioning in DeFi interactions. The flip suggests that USDT’s dominance is no longer limited to centralized exchange corridors but is seeping into DEXs and DeFi ecosystems too.

Implications for Measurement, Policy & Infrastructure

Rethinking “Activity” Metrics

If bots account for 70 %+ of stablecoin transfers, then raw volume becomes a much noisier proxy for “adoption.” Analysts and investors must parse adjusted metrics that exclude or weight down bot-driven flows to better surface human-initiated transfers.

Some possible measurement refinements:

- Exclude known high-frequency accounts / suspicious addresses

- Focus on the retail / micro transaction band as a signal of genuine usage

- Monitor the growth of non-trading transactions (payments, remittances, merchant activity)

- Use on-chain heuristics to flag wash trades or circular flows

Policy and Regulatory Challenges

Policymakers must grapple with a dual imperative: encouraging growth and innovation while guarding against misleading metrics, manipulation, and systemic risks. If regulators treat all on-chain volume as equal, they risk inflating the perceived scale of stablecoin adoption.

Regulatory frameworks (e.g. MiCAR in Europe, U.S. stablecoin legislation proposals) must account for algorithmic activity vs. real usage. Some jurisdictions are already debating whether to impose disclosure or transparency rules on algorithmic liquidity providers or require “anchor institutions” issuing stablecoins to audit flow origin.

Architectural Innovation: Toward Smarter Stablecoins

To better align stablecoins with real economic use, emerging academic and protocol research offers paths forward. One promising direction is hybrid stabilization protocols combining:

- Algorithmic / AI-driven arbitrage incentives

- Adaptor signatures for cross-chain atomic swaps

- Zero-knowledge proofs for compliance and AML privacy

- Collateralized reserves + synthetic derivatives for stabilizing peg dynamics

Another strand of research explores hybrid monetary ecosystems, where private stablecoins co-exist with fiat or central bank money, backed by reserves and modular programmability to ensure both reliability and innovation.

Meanwhile, in the broader algorithmic trading domain, new models like multi-agent LLM / AI systems tailored for high-frequency trading (e.g. QuantAgent) are showing how advanced decision logic can further optimize bot strategies.

As smart contract environments evolve, we may see “smarter stablecoin layers” that actively self-stabilize, adjust spread, and filter bot friction — thereby pushing the stablecoin ecosystem closer to truly economic utility, not just liquidity games.

Conclusion

The Q3 2025 stablecoin landscape reveals a paradox: while volume metrics soared to all-time highs, the majority of that movement is orchestrated by automated bots, not human actors. At the same time, retail transfers are quietly breaking records, indicating that genuine usage is growing in parallel (though perhaps still in the shadow of algorithmic flows).

For participants hunting new crypto opportunities, this suggests several strategic implications:

- Beware of “false volume” — a token could show massive on-chain activity yet have minimal real demand.

- Focus on non-trading flows and retail traction — these may better signal sustainable adoption.

- Watch for next-gen stablecoin architectures (hybrid, AI-augmented, cross-chain) — these could reshape which projects capture the value zone between protocol and utility.

- If building or evaluating a project, think about bot resilience, anti-manipulation heuristics, liquidity schemes, and peg stability mechanisms from the ground up.

- For regulators and analysts, refined metrics and classification of algorithmic vs human flows become essential to avoid misleading narratives.

Ultimately, the stablecoin domain appears to be entering a maturation phase: liquidity and automation have proven viable, but the next frontier is forging real-world economic relevance. Those who can meaningfully straddle both — robust algorithmic infrastructure and true utility — may define the future of digital money.