Main Points :

- Michael Saylor anticipates a Bitcoin price rebound toward year-end, underpinned by institutional and corporate accumulation.

- Businesses and ETFs are absorbing BTC at multiples of miner issuance, tightening available supply.

- Some risk factors remain: policy, market sentiment, and potential demand slowdowns.

- Broader trends: more non-mining firms holding BTC, shrinking exchange reserves, and evolving institutional adoption.

- The outlook suggests a favorable setup for new crypto opportunities and business uses of blockchain.

1. Saylor’s Year-End Forecast: Price Poised to “Move Up Smartly”

Michael Saylor, Executive Chairman of Strategy (formerly MicroStrategy), appeared on CNBC and projected that Bitcoin would shift into an upward trajectory toward the end of 2025. He argues that after wrestling with macro headwinds and resistance levels, the momentum from corporate and institutional accumulation will help Bitcoin “move up smartly again.”

Saylor’s logic rests on the view that demand from corporate treasuries and ETFs already surpasses natural supply from miners. He frames this mismatch as a structural driver for price appreciation.

Some analysts have taken this further: one projection posits BTC exceeding $124,000 by year-end based on corporate demand, ETF inflows, and seasonal tailwinds. Others remain more conservative, anticipating milder gains in light of macro pressures.

All told, Saylor’s forecast is bullish, betting that supply constraints and sustained demand will overcome any interim headwinds.

2. Institutional and Corporate Accumulation: Absorbing the Supply

2.1 Demand outpacing miner issuance

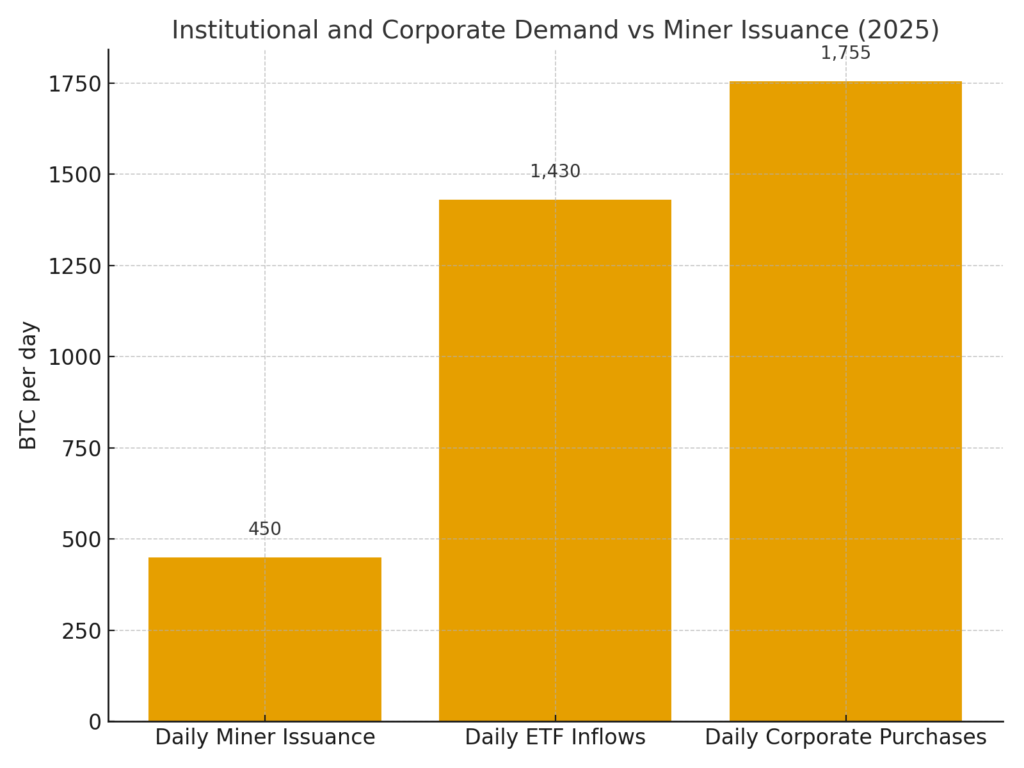

One of the most striking developments in 2025 is the disparity between Bitcoin issuance by miners and absorption by institutions. According to River’s flow analysis, businesses are acquiring on average 1,755 BTC per day. In contrast, miners’ new issuance is estimated at only about 450 BTC per day (post-halving).

ETFs and funds add further pressure: about 1,430 BTC per day in net inflows. Combined, institutional and corporate demand far outpaces supply, creating a tightening of free float.

River’s researchers caution that the flow figures are estimates based on address tagging and heuristics, so they should be interpreted as directional rather than exact.

2.2 Corporate treasuries and non-traditional adopters

It’s not just classic Bitcoin treasury companies (like Strategy) accumulating; non-mining firms are quietly putting BTC on their books too. Analysts estimate that “ordinary companies” have added about 84,000 BTC in 2025. Real estate firms reportedly led allocations, often deploying 8–15% of profits into BTC.

In total, businesses now hold more than 6% of Bitcoin’s circulating supply, a twenty-one-fold increase since 2020.

A case in point: as of 2025, Strategy is said to hold over 630,000 BTC, making it one of the largest corporate holders globally.

These patterns suggest that corporate adoption is maturing beyond just a few high-profile names to a broader base of firms that view BTC as a reserve or strategic asset.

2.3 Shrinking exchange reserves and potential supply shock

As institutions accumulate and hold, BTC balances held on exchanges continue to decline, reaching multi-year lows. The concentration of supply in wallets unlikely to sell creates the risk of a supply shock if demand remains strong and available float dries up.

Many analysts view this supply compression as a bullish structural factor: if institutional demand continues, it could magnify upward moves during bull phases.

3. Risks and Counterpoints to the Bull Thesis

While the accumulation story is compelling, there are several caveats and risks that could derail or moderate a year-end rally.

3.1 Demand slowdown or capital rotation

If companies slow their purchases, or shift funds elsewhere (e.g. equities, bonds), the demand tailwind may weaken. The pace of corporate allocation is not guaranteed.

Similarly, ETF flows are sensitive to macro and regulatory sentiment. A reversal or capital outflow could introduce volatility.

3.2 Policy and regulatory overhang

Bitcoin remains exposed to regulatory risk, especially in major jurisdictions like the U.S. Any adverse shifts—tax changes, crackdowns on exchanges, or restrictions on institutional holdings—could weigh on price sentiment.

Saylor has indicated he has had discussions with U.S. policymakers and sees Bitcoin as beneficial to national interests, but he has not confirmed giving direct advice.

3.3 Valuation volatility and mark-to-market losses

For firms holding large BTC inventories, accounting rules and market volatility can generate large unrealized losses on balance sheets. Strategy (MicroStrategy) itself reported five straight quarterly losses as of early 2025, driven largely by fair-value accounting of its BTC holdings.

Investors may penalize firms with levered positions into Bitcoin if the volatility persists, especially during drawdowns.

3.4 Macroheadwinds and correlation risk

Bitcoin is not immune to macro collapses. Liquidity squeezes, rate hike cycles, currency depreciation, or equity market stress could drag cryptos downward, regardless of internal supply dynamics.

Saylor himself references “macro headwinds” as obstacles Bitcoin must navigate before resuming its climb.

4. Implications and Strategic Takeaways

Given this landscape, what are the key lessons or signals for your audience of crypto-seekers, builders, and business users?

4.1 Watching accumulation flows is essential

Net flows into corporate treasuries and ETFs may now be as meaningful as price charts themselves. Tracking on-chain flows, wallet tags, and exchange reserve data can provide early signs of structural shifts.

4.2 Explore secondary opportunities

While many are focused on BTC, the same structural dynamic may begin to favor select altcoins or Layer-1s with utility, yield, or interoperability. Higher BTC valuations could create new capital rotations.

Projects that serve institutional adoption—e.g. custody, regulation, compliance, tokenization—stand to benefit in this environment.

4.3 Business blockchain use cases get renewed attention

As firms accept crypto on their balance sheets, they may also explore blockchain as infrastructure for finance (e.g. tokenizing assets, stablecoin usage, programmable treasury operations). This supports demand not just for BTC but for broader blockchain ecosystems.

4.4 Risk management and diversification remain critical

Given volatility, prudent allocation, hedging strategies, and clarity about regulatory exposure remain necessary. Even strong structural trends can misfire in the short run.

Summary & Outlook

Michael Saylor’s recent forecasts inject vitality into the narrative that Bitcoin is on the cusp of a strong year-end move. The underpinning logic is clear: with corporate and ETF demand absorbing BTC faster than miners can issue it, the free float is tightening. This demand–supply imbalance is the central thesis for a late-2025 rally.

However, the path is far from certain. Momentum depends on sustained accumulation, favorable regulation, macro stability, and confidence among institutional actors. The risks of drawdowns, accounting losses for firms, or demand pullbacks must not be overlooked.

For readers scouting new cryptos or building blockchain use cases, this is an inflection point. The capital flows into BTC could eventually spill into adjacent protocols, infrastructure, and tokenized assets. Meanwhile, companies with real use cases for blockchain may find fresh impetus in this environment.

In sum: the structural setup is favorable for Bitcoin heading into year-end, but execution, discipline, and external conditions will determine if the rally becomes real.