Main Points :

- On-chain metrics from Glassnode hint that Bitcoin’s post-FOMC rally is entering a correction or consolidation phase.

- Long-term holders (LTHs) have realized ~3.4 million BTC in profits, pressuring supply.

- Inflows into spot Bitcoin ETFs have slowed sharply, weakening a key institutional demand source.

- Futures and derivatives markets show signs of deleveraging, reduced open interest, and increased downside skew.

- Volatility drawdowns remain modest (~8 %), but lower overall volatility may amplify liquidity-driven swings.

- The balance between long-term holder supply and institutional appetite is becoming tenuous — risking further market cooling unless new catalysts emerge.

- Recent trends suggest Bitcoin is increasingly viewed as a “flight to quality” among crypto assets; broader institutional participation and macro sentiment will be critical going forward.

1. Post-FOMC Exhaustion & “Rumour-Buy, News-Sell” Dynamics

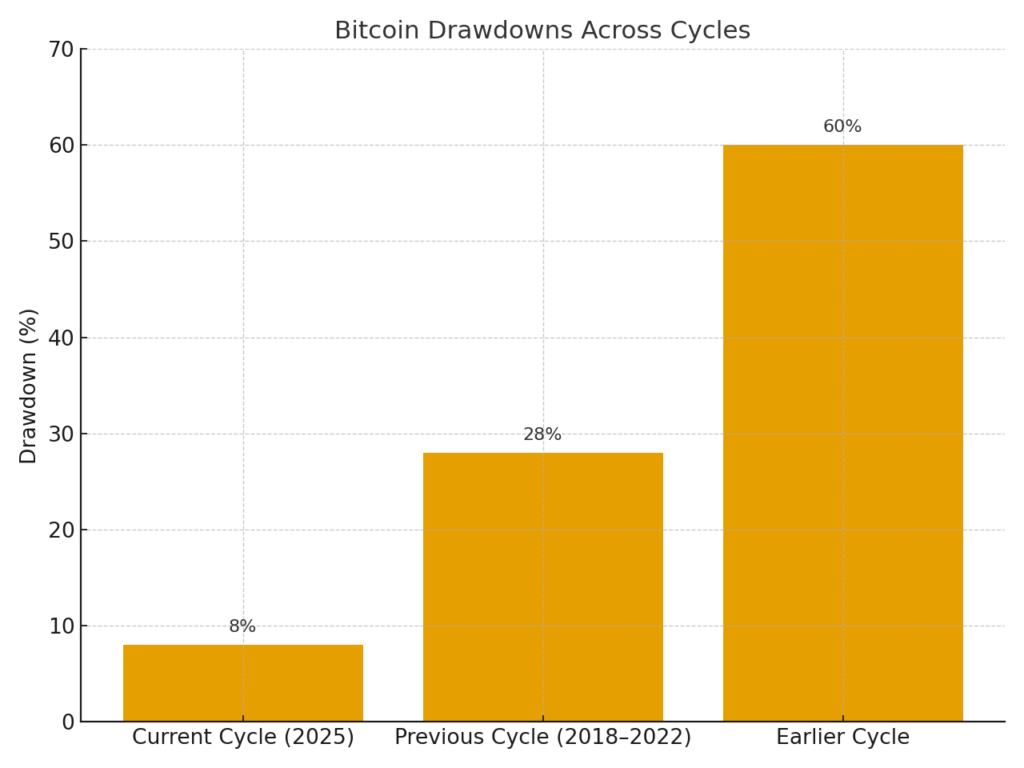

Glassnode’s latest weekly market report interprets Bitcoin’s recent behavior as characteristic of a “buy the rumor, sell the news” pattern, following a sharp FOMC-driven rally. After reaching a peak near $124,000, price has retraced to around $113,700, marking an ~8 % drawdown — a relatively mild correction compared to earlier cycles that saw 28 % to 60 % drops. In Glassnode’s view, this suggests a maturing pattern of volatility compression across cycles.

However, the signs of momentum fading shouldn’t be ignored. The rally’s tailwinds are weakening, and without fresh demand, supply pressure may take over.

2. Realized Profits: Long-Term Holders Cashing Out

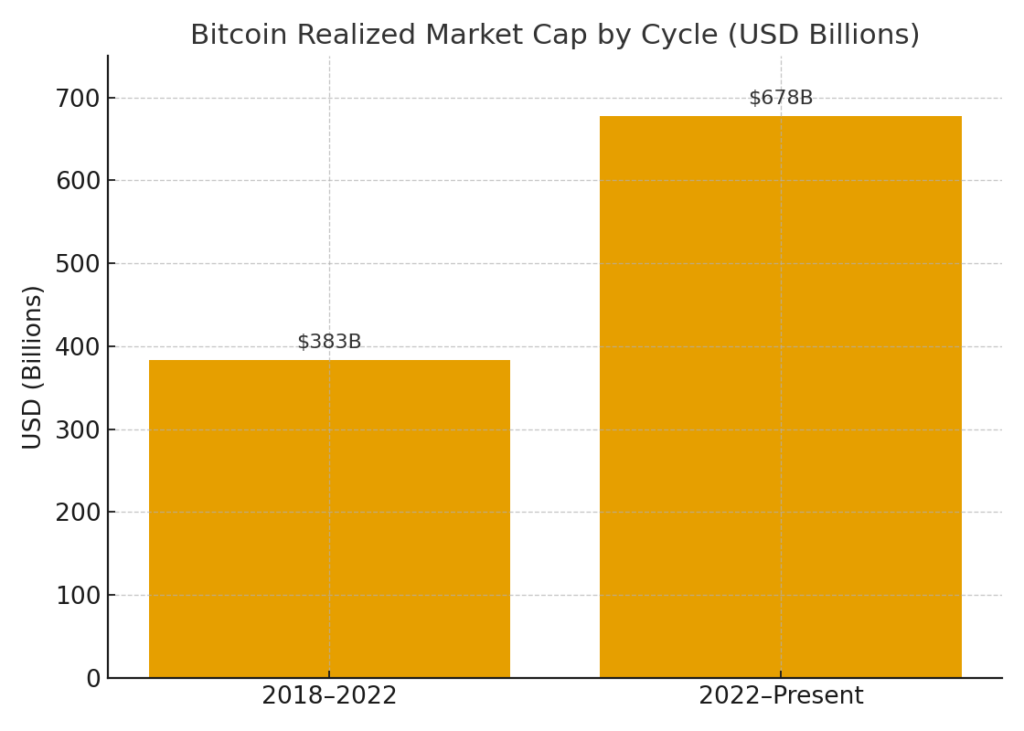

A striking signal is the volume of realized profits by long-term holders (LTHs). To date, LTHs have taken profits on approximately 3.4 million BTC in this cycle — a figure already surpassing comparable points in prior cycles. The realized market cap (i.e. value of coins when last moved) for the current cycle has reached ~$678 billion in USD terms, eclipsing the prior cycle’s ~$383 billion by nearly 1.8×.

What this means in practice is that a segment of holders who were previously inert are now supplying coins to the market — before institutional or ETF demand can fully absorb it.

3. ETF Inflows Decelerating: Demand Slackens

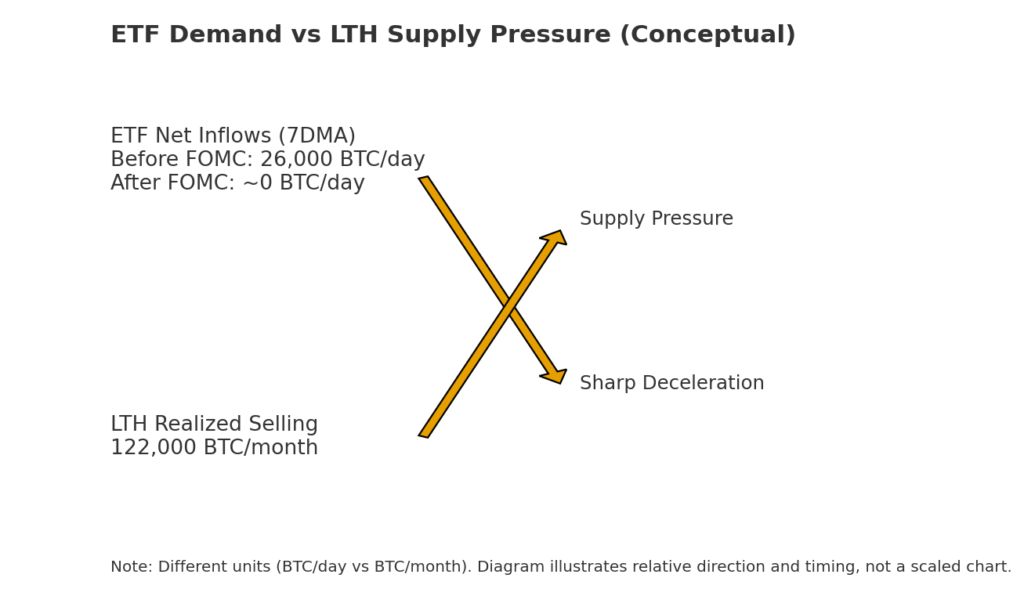

Spot Bitcoin ETFs had been a key demand sink, absorbing much of the supply released by long-term holders. But that demand appears to be cooling. According to Farside / Bitcoin ETF flow data, net inflows dropped from ~$2.03 billion to ~$931 million week-over-week — a 54 % decline. Glassnode’s own commentary highlights that while accumulation has not reversed entirely, a “slowdown suggests a pause in institutional demand.”

In the specific Glassnode weekly report, around the FOMC timeline, ETF inflows (7-day moving average) fell from ~26,000 BTC/day to near zero, even as LTHs’ monthly sales jumped to ~122,000 BTC.

In short: the buffer that institutional flows provided is weakening at precisely the moment supply pressure increases.

4. Derivatives Market: Deleveraging & Skew

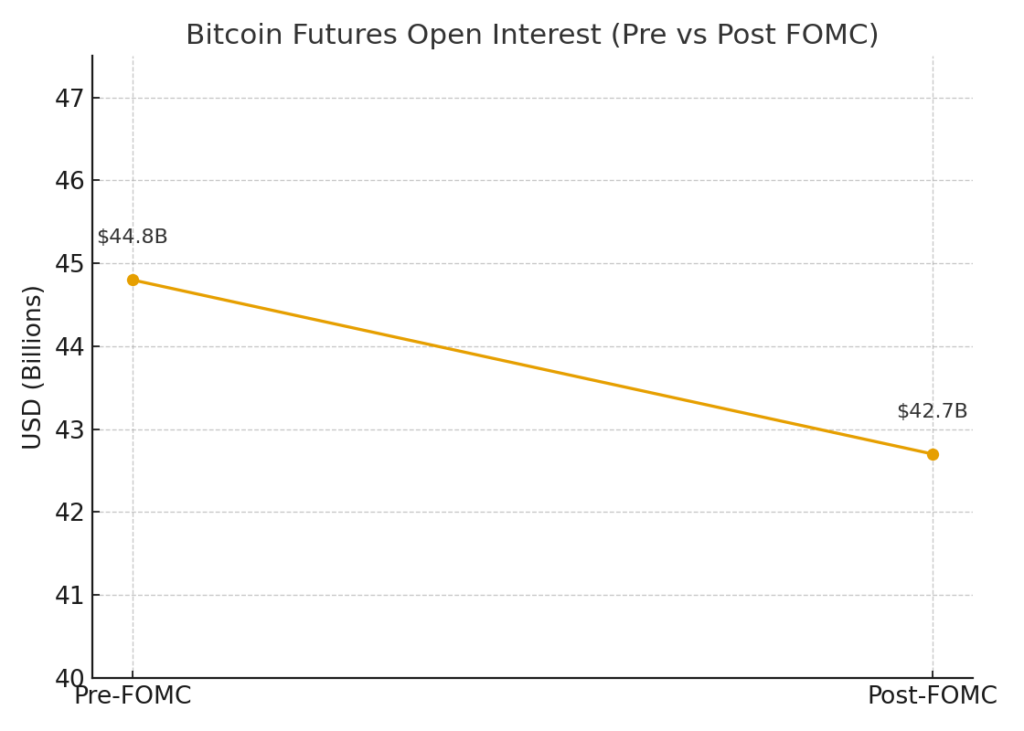

Beyond spot markets, the derivatives space is reflecting stress. Futures open interest has declined (e.g. from $44.8 billion to $42.8 billion), indicating that leveraged bets are being unwound. Long-heavy positions have been squeezed, and many leverage-driven longs have been liquidated.

In options markets, the put–call skew is rising: demand for protective puts is increasing relative to call demand, pricing in greater downside risk. Short- and medium-term options still tilt toward puts, consistent with a market hedging for downside exposures.

These signals, combined with lower overall volatility, suggest the market is vulnerable to liquidity-driven swings — even modest catalysts could push it meaningfully either way.

5. Volatility Regime & Liquidity Sensitivity

Although the drawdown has been limited (~8 %), that is in line with the idea of volatility compression across longer cycles. Historically, lower volatility regimes precede decisive moves because markets are more responsive to flow imbalances in low-volatility environments.

In such contexts, shifts in liquidity become more impactful: minor changes in supply or demand can lead to outsized directional moves. This suggests that the market’s next leg — up or down — may be determined less by fundamentals and more by capital flows and positioning.

6. Battle of Supply vs Demand: A Fragile Equilibrium

We are now in a tug-of-war between two forces:

- On one side, LTHs realizing profits and increasing supply pressure.

- On the other, institutional/ETF demand that has historically soaked up excess coins.

With the latter decelerating, the balance is fragile. If ETF and institutional flows don’t revive or if fresh buyers don’t step in, further downside or extended consolidation becomes the path of least resistance.

7. Broader Trends: Flight to Quality & Institutional Lens

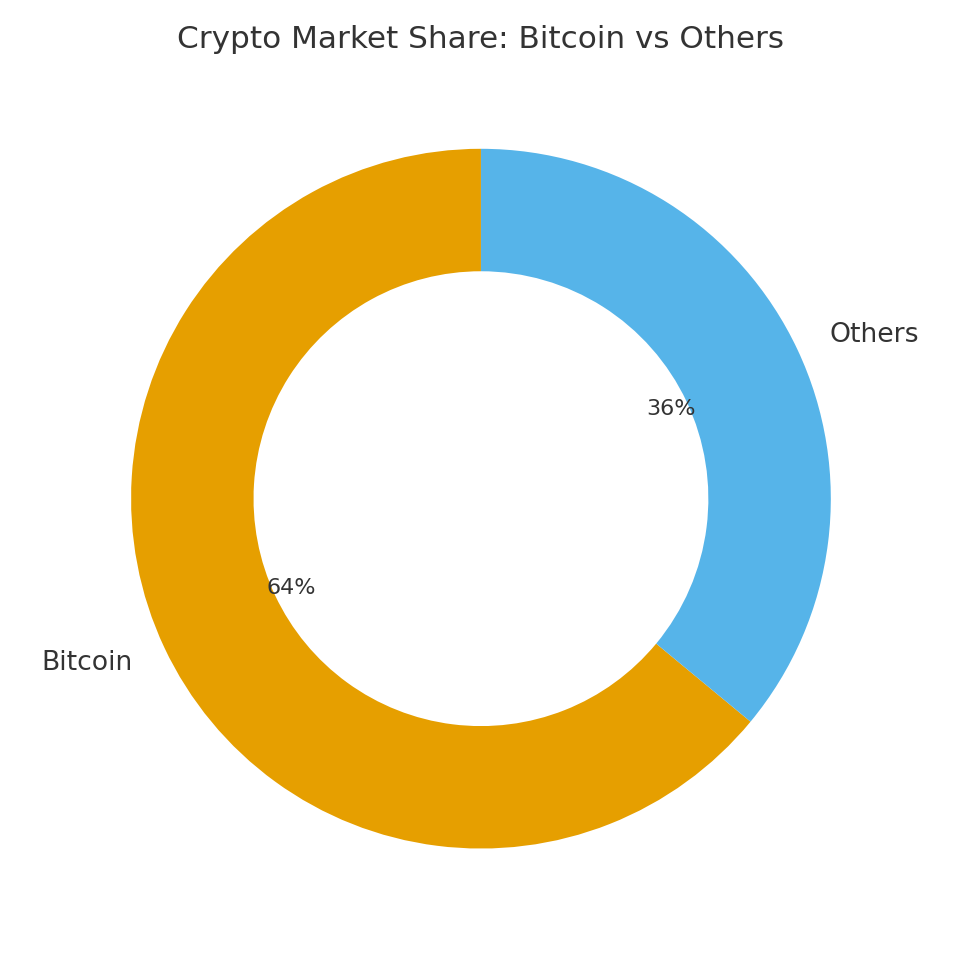

Outside of pure supply-demand dynamics, there are thematic shifts worth noting. In the broader crypto market, Bitcoin has regained dominance as a “flight to quality” asset: its share of total crypto market cap rose to about 64 %, the highest since early 2021. This suggests capital is rotating out of smaller, riskier alts and toward more liquid, institutionally recognized assets.

Meanwhile, academic studies are highlighting Bitcoin’s growing integration into traditional financial markets. Correlation with U.S. equities (Nasdaq, S&P 500) has intensified around institutional arrival milestones. This means macro and regulatory moves will increasingly impact Bitcoin’s trajectory.

On the technical/protocol side, a notable new academic study argues that in Bitcoin’s propagation topology, full nodes (especially home-hosted ones) have become peripheral, with the miner clique dominating transaction broadcast paths. While this is more of a structural or network insight, it underscores how infrastructure centralization dynamics may evolve in parallel to market behavior.

8. Recent News & Developments

To contextualize these signals, a few recent developments are illustrative:

- ETF flow deceleration is being tracked across platforms; according to TradingView / Cointelegraph, net inflows dropped ~54 % month-on-month, reinforcing a narrative of “ETF slowdown.”

- Market update from The Block noted Bitcoin dipping below $112,000 despite ~$241 million in spot inflows, pointing to macro jitters (particularly around Fed rate expectations) dampening sentiment.

- Glassnode’s “Market Impulse” report flags that Bitcoin futures open interest is falling and leverage is being withdrawn — consistent with the on-chain decomposition.

These developments align with the broader theme: the market is in a neutral or negative drift unless fresh catalysts (e.g. renewed institutional flows, macro tailwinds, regulatory clarity) emerge.

Summary & Outlook

In sum, Glassnode’s analysis — supplemented by ETF flow data, derivatives positioning, and recent market commentary — paints a picture of a Bitcoin market entering a more defensive phase. The post-FOMC rally is showing signs of fatigue. Long-term holders are realizing profits aggressively, and the institutional demand that once buffered this supply is cooling. Derivatives markets are unwinding leveraged positions, and volatility remains compressed, making liquidity flows more consequential than ever.

From here, Bitcoin’s trajectory will likely depend on who blinks first in the supply-demand tug-of-war. If ETF and institutional participation reignite, the market may resume its uptrend; however, absent a fresh catalyst, extended consolidation or even downside risk is real. The increasing maturity of the market means macro, regulatory, and institutional frameworks will weigh heavily in shaping the next leg.

For readers hunting new crypto opportunities or practical blockchain applications: Bitcoin now behaves less like a young, nascent asset and more like a quasi-systemic, institutional instrument. That means entrants must pay close attention to capital flows, infrastructure developments, regulatory shifts, and macro inputs — not just price charts or sentiment alone.