Main Points :

- The US Treasury plans to withdraw $500–600 billion from markets over the next 2–4 months to rebuild its General Account (TGA), potentially limiting liquidity.

- Historically, Bitcoin has lagged after peaks in the M2 money supply, particularly when paired with massive Treasury issuance.

- The Fed’s reverse repo buffer has shrunk from over $2 trillion to about $28.8 billion, weakening absorption support.

- Stablecoin supply contraction tends to coincide with crypto stagnation, and stablecoin issuers are now holding over $120 billion in Treasury debt.

- Structural market support is weaker in 2025 due to constrained bank balance sheets, unrealized losses, and reduced foreign demand.

- These conditions likely set the stage for Bitcoin underperformance through the fall, with relief only after the liquidity draw concludes in late 2025.

1. Treasury Liquidity Drain: Setting the Stage

According to the most recent Delphi Digital analysis (as reported by CryptoSlate and other outlets), the US Treasury is poised to begin absorbing a substantial amount of liquidity—$500 to $600 billion—from financial markets over the next two to four months as it rebuilds its General Account (TGA) at the Federal Reserve. This process could deeply impact crypto markets, notably Bitcoin.

2. M2 Money Supply Peak as a Liquidity Signal

Bitcoin’s price performance has historically mirrored peaks in the M2 money supply, typically with a time lag of several weeks. Delphi Digital’s modeling suggests that M2 is expected to peak around September 2025, and may already be rolling over by approximately 8 percent relative to projected highs.

Such a peak, when combined with aggressive Treasury issuance, creates a potent dual shock—reducing liquidity while removing cash from markets—a scenario known to correlate with Bitcoin underperformance.

3. Stablecoin Contraction: Gatekeeper of Crypto Liquidity

A notable dynamic of the 2023 TGA refill was the contraction in the total supply of stablecoins to around $5.15 billion, coinciding with a flattening of Bitcoin’s price. Stablecoins serve as key liquidity gateways for crypto transactions. Today, issuers hold over $120 billion in Treasury debt, making them highly sensitive to redemption pressure when the Treasury begins absorbing cash.

In short, a drawdown in stablecoin supply can throttle liquidity deep into the crypto rails, making altcoins and even Bitcoin vulnerable.

4. Structural Weakness: Why 2025 is Different

Three main structural weaknesses elevate risk in 2025 compared to prior cycles:

- Bank balance sheet constraints: Delphii notes that banks are facing roughly $482 billion in unrealized securities losses—reducing their capacity to absorb shocks.

- Reduced foreign demand: China and Japan, historically major buyers of Treasuries, have reduced their holdings by over $400 billion since 2021, shifting the burden back to domestic buyers.

- Quantitative Tightening: The Federal Reserve continues QT at about $60 billion per month, further tightening liquidity.

These compounding factors heighten the impact of Treasury issuance and amplify liquidity stress within crypto markets.

5. Bitcoin’s Vulnerability This Fall

Taken together, the expected M2 peak, massive Treasury borrowing, weak absorption buffers, shrinking stablecoin liquidity, constrained banks, and limited foreign demand create an environment ripe for Bitcoin underperformance through the fall of 2025.

As CryptoSlate summarizes: “This liquidity headwind would temporarily but substantially limit crypto enthusiasm until the refill is completed in late 2025”.

市場全体のリスク選好が減少し、高β資産であるアルトコインはより大きな打撃を受ける可能性も高いです。 [Insert Graph Here]

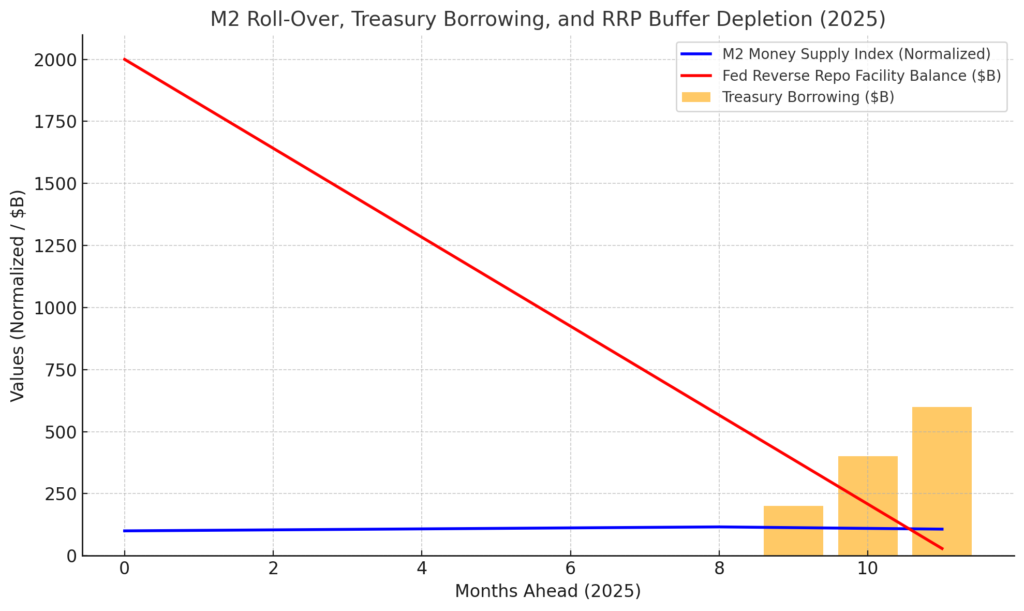

Planned insertion location: After section 2 (M2 Money Supply Peak).

Caption: Projected M2 Money Supply Roll-Over vs. Expected Treasury Borrowing ($500–600 billion over 2–4 months) vs. Fed’s Reverse Repo Buffer Depletion.

このグラフでは、M2のピークアウト時期、国債発行による資金吸収、そしてFRBのリバースレポファシリティ残高の減少という、三つの主要動向が視覚的に比較できます。これによって流動性リスクの構造が一目で理解できます。

6. Broader Implications: Beyond Bitcoin

While the focus is on Bitcoin, broader crypto markets are also at risk. Stablecoins serve as plumbing for DeFi, trading, and on‑chain activity. Their contraction could affect DeFi protocols, institutional inflows, yield strategies, and tokenized assets.

Furthermore, altcoins—especially those with high beta—may experience accelerated declines during this liquidity drawdown. The report indicates that structural inflows such as ETF-driven investment or corporate treasury allocations could mitigate some of these effects, but such support is uncertain at this juncture.

7. Conclusion: Timing and Strategic Outlook

By late 2025, once the Treasury refilling process concludes, liquidity conditions may stabilize and crypto enthusiasm could return. For now, prospective investors seeking the “next crypto opportunity” or practical blockchain deployment should navigate carefully:

- Timing matters: A cautious stance through the fall may be prudent, with potential repositioning expected in late 2025.

- Diversification strategy: Consider allocating across stable, yield-generating, or utility-oriented blockchain projects that are less dependent on speculative inflows.

- Monitor on-chain and macro indicators: M2 trends, stablecoin flows, Treasury issuance schedules, and Fed facility usage all offer early signals of shifting liquidity conditions.