Main points :

- BlackRock has not filed a U.S. spot Solana (SOL) ETF as of today; top ETF analysts think it would be problematic if they jumped in at the last moment alongside issuers that have worked with the SEC for months.

- The first U.S. spot SOL ETF filing came from VanEck in June 2024; since then, multiple issuers (Bitwise, Grayscale, Invesco, 21Shares, CoinShares, Canary Capital, Franklin Templeton, Fidelity) have filed or amended S-1s.

- The SEC has delayed decisions and set new deadlines around Oct 10, 2025 for at least some SOL filings, while asking for updated documents to improve legal clarity.

- In June 2025, seven SOL ETP issuers amended S-1s to add staking language (with CoinShares and Invesco Galaxy following soon after), highlighting an industry push to allow staking inside ETPs.

- BlackRock’s likely near-term play is to grow IBIT (Bitcoin) and ETH funds and possibly explore multi-asset crypto index products rather than a single-asset SOL ETF—especially since BTC+ETH account for ~90% of total crypto market cap and IBIT alone has reached roughly $70B AUM.

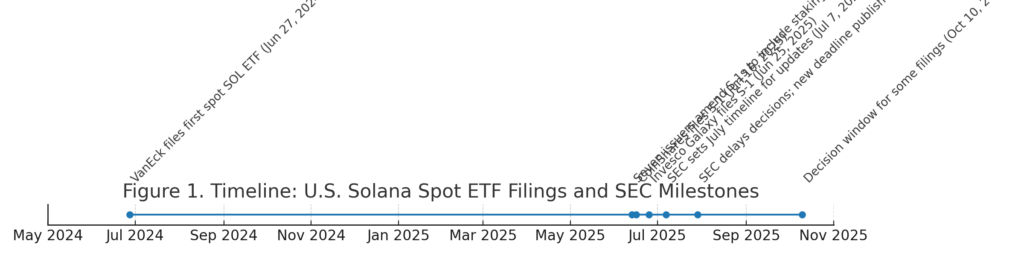

[Insert Figure 1 here — Timeline of U.S. Solana ETF filings and SEC milestones]

1) The spark: “Should BlackRock jump the line on a SOL ETF?”

The debate reignited after a widely shared interview where ETF analyst James Seyffart said it would be “messed up” if BlackRock—without any SOL filing—submitted a last-minute application and launched simultaneously with first movers who have engaged with the SEC for months. Nate Geraci added that BlackRock may be letting competitors test demand first; if uptake is strong, they could enter later. The same exchange noted that BlackRock might instead prioritize a crypto index product and that skipping a SOL ETF isn’t a big risk given BTC+ETH dominate market cap.

2) Who has filed for a U.S. spot Solana ETF so far?

VanEck broke ground with the first U.S. spot SOL filing in June 2024. Subsequent/parallel applicants include Bitwise, Grayscale, Invesco, 21Shares, CoinShares, Canary Capital, Franklin Templeton, and Fidelity. These firms have invested substantial time iterating S-1s and 19b-4s to align with SEC feedback—one reason analysts argue it would be unfair for a latecomer to leapfrog to a first-wave launch.

What’s changed in 2025: In June 2025, seven filers updated S-1s to explicitly enable staking if allowed; CoinShares joined days later and Invesco Galaxy followed, all proposing some form of staking or liquid-staking-token (LST) approach. This marks the first coordinated push to let proof-of-stake economics flow to ETP investors (subject to SEC conditions).

See Figure 1 for a compact timeline of filings, amendments, and SEC milestones.

3) Where the SEC stands: delays, deadlines, and the staking question

The SEC has postponed decisions on SOL proposals multiple times, with decision windows around Oct 10, 2025 reported for at least some applications. Beyond timing, the Commission has asked issuers to tighten legal language and address operational risks (safekeeping, pricing, surveillance, conflicts, and—critically for SOL—if and how staking can be permitted).

A July 31, 2025 submission to the SEC’s Crypto Task Force summarized the amended SOL filings and advocated for allowing LSTs in ETPs. The letter cites seven issuers that amended S-1s on June 13, 2025 to include staking language, CoinShares on June 16, and Invesco Galaxy on June 25—one of the clearest public snapshots of how staking has become central to SOL ETP design.

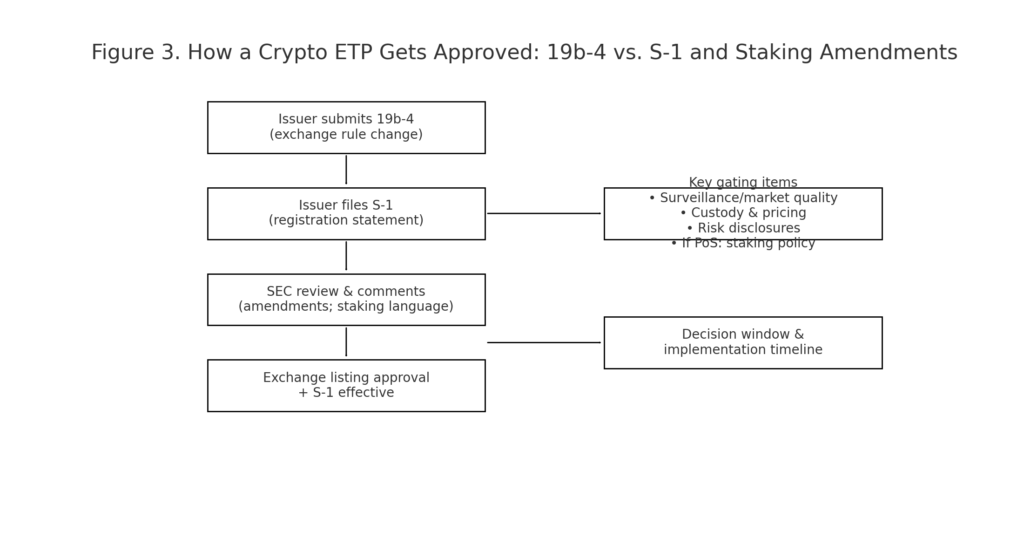

[Insert Figure 3 here — How a crypto ETP gets approved: 19b-4 vs. S-1 and staking amendments]

4) Will BlackRock file a SOL ETF? Reading the tea leaves

Fact pattern today: BlackRock has IBIT (spot Bitcoin) and an Ethereum product; its SOL filing does not exist at the time of writing. Multiple trade outlets note that BlackRock is not currently pursuing a SOL or XRP ETF “at this time,” focusing instead on scaling its existing crypto products. Analysts also float the possibility that, if SOL ETP demand proves strong after initial launches by other issuers, BlackRock could enter later.

Strategic logic:

- Scale and simplicity: The addressable market for BTC and ETH dwarfs other assets. If ~90% of crypto market cap sits in BTC and ETH, capturing those two, plus a diversified index beyond them, might be a better risk-adjusted use of BlackRock’s brand and distribution.

- Operational leverage: A multi-asset crypto index can aggregate demand across several top coins while avoiding single-asset regulatory chokepoints (e.g., staking nuances unique to SOL). Seyffart explicitly pointed toward index product demand as strong.

- Tokenization runway: BlackRock is leaning into tokenization (e.g., its BUIDL tokenized money market fund). That direction, plus expanding IBIT and ETH exposure, may be a nearer-term priority than a SOL-only fund.

Bottom line: A SOL ETF from BlackRock is possible later—especially if first-mover issuers prove strong, durable demand—but a near-term filing feels unlikely given what the firm is saying and doing today.

5) Demand math: what would a SOL ETF need to succeed?

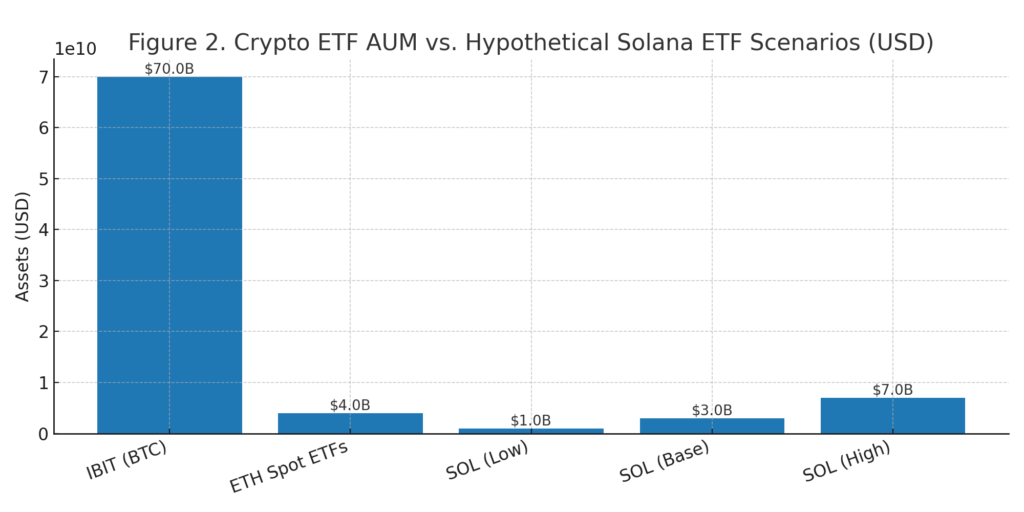

To frame potential assets under management (AUM) and flows in U.S. dollars ($):

- IBIT (BlackRock’s spot BTC) has grown into a behemoth, widely reported around $70B AUM—the fastest-growing ETF in history by many accounts. ETH spot ETFs have reached roughly $4B. These figures shape expectations for a next-wave asset like SOL.

From those anchors, a reasonable initial range for SOL ETPs (across all issuers) could look like $1B–$7B in the first 1–3 months if (a) market conditions are supportive, (b) staking economics are clearly approved and passed through (or priced in), and (c) liquidity on major U.S. exchanges is deep and predictable. That’s not a forecast—just a scenario range informed by BTC/ETH precedents and the scale of institutions that want compliant wrappers. (For context, see Figure 2 below.)

[Insert Figure 2 here — Crypto ETF AUM vs. hypothetical Solana ETF demand scenarios]

Method note: IBIT and ETH AUM are indicative snapshots; SOL “Low/Base/High” are illustrative scenarios to help plan liquidity and market-making, not predictions.

6) What could still hold SOL back?

- Regulatory heuristics: Historically, the SEC looked favorably on assets with CFTC-regulated futures that support robust surveillance sharing. ETH had CME futures; SOL does not (as of writing), which has been flagged in prior market commentary. This doesn’t preclude approval, but it’s a hurdle in the narrative.

- Staking policy clarity: The staking question—direct staking vs. LSTs, who performs it, who bears slashing risk, tax treatment, and revenue split—remains under SEC scrutiny. That’s why the June 2025 S-1 amendments matter so much.

- Macro flows: If crypto flows soften or volatility spikes, marginal demand for a new single-asset ETP can shrink quickly. That’s one reason index products are attractive.

7) For builders, traders, and treasuries: practical takeaways

- Builders on Solana: Approval momentum—especially with staking allowed—could deepen capital markets rails (basis trades, structured notes, options overlays) and reduce the cost of capital for projects building on SOL. No filing from BlackRock doesn’t hurt this dynamic if other issuers get to market.

- Active traders/market makers: Prepare inventory and delta hedges for likely day-1 inflows in the $1B–$7B range (all issuers combined) in a supportive tape; widen ranges if macro deteriorates.

- Treasuries and funds: For institutions that cannot buy tokens directly, SOL ETPs would provide compliant exposure in $ and simplify ops (KYC’d brokers, qualified custody). If staking gets approved inside the wrapper, review accounting and revenue recognition.

8) What to watch next (and when)

- 19b-4 orders and S-1 comment cycles through Q3–Q4 2025, especially language around staking or LSTs.

- SEC decision windows near Oct 10, 2025 (at least for some filings).

- Issuer coordination: If one SOL ETP gets approved, others may launch in quick succession; watch for fee races and seed AUM.

- BlackRock signals: Continued public comments from leadership and any filings that suggest index or basket approaches (e.g., diversified crypto index ETP).

9) Conclusion

The smart read for now: BlackRock is unlikely to file a SOL ETF before first movers. Their focus on IBIT and ETH, plus potential index-style products, makes strategic sense given how BTC and ETH dominate flows and market cap. Meanwhile, SOL ETP applicants have done the hard yards—amending S-1s to include staking and iterating with the SEC—and are moving toward key decision windows around October 2025.

If early SOL ETFs attract meaningful $-denominated inflows and staking terms are workable, BlackRock can always follow. But if demand proves niche relative to BTC/ETH, the index path looks like the more scalable avenue for the world’s largest asset manager.