Main Points :

- JPMorgan’s CFO publicly warned that yield-bearing stablecoins could undermine the regulated banking system if left outside traditional supervisory frameworks.

- The debate highlights a structural conflict between regulated banking stability and crypto-native financial innovation.

- Recent U.S. legislative efforts, including the GENIUS Act and the CLARITY Act, aim to define strict guardrails for stablecoin issuance and rewards.

- Yield-bearing designs remain controversial, but activity-based rewards (liquidity provision, staking, governance) are being treated differently from passive interest.

- For investors and builders, this moment signals both regulatory risk and strategic opportunity in stablecoin design and blockchain-based finance.

Introduction: A Rare Public Warning from Wall Street’s Core

During JPMorgan Chase’s Q4 2025 earnings call, an unusual topic took center stage: stablecoins. While Wall Street executives increasingly acknowledge blockchain’s efficiency and inevitability, JPMorgan’s Chief Financial Officer, Jeremy Barnum, delivered a clear warning. His concern was not about blockchain itself, but about a specific design choice—yield-bearing stablecoins that resemble bank deposits without being subject to bank-level regulation.

This statement, prompted by a question from Evercore analyst Glenn Schorr, arrived at a time when U.S. lawmakers are actively debating how digital assets should be regulated. Stablecoins, once viewed as a narrow crypto tool, have now become a focal point for policymakers, banks, and investors alike.

For readers seeking new crypto assets, alternative revenue streams, or practical blockchain use cases, this debate is more than regulatory noise. It directly affects where yield comes from, who controls money, and how trust is enforced in the next financial system.

JPMorgan’s Core Argument: Parallel Banking Without Guardrails

Barnum emphasized that JPMorgan supports competition and innovation. However, he drew a sharp line when stablecoins begin to replicate the core functions of banks—particularly interest-bearing deposits—without equivalent oversight.

In his words, creating a parallel banking system that includes interest-paying deposits “without the hundreds of years of bank regulation and safety measures” is “clearly dangerous and undesirable.”

Why This Matters Structurally

Traditional banks operate under:

- Capital adequacy requirements

- Liquidity coverage ratios

- Deposit insurance frameworks

- Continuous supervisory examinations

Yield-bearing stablecoins, by contrast, may:

- Hold reserves off-balance-sheet

- Reinvest collateral into short-term instruments

- Offer daily liquidity without lender-of-last-resort support

From a systemic risk perspective, this creates an asymmetry: similar functions, radically different safeguards.

The Banking Industry’s Anxiety: Not Just Protectionism

In May last year, industry sources described the U.S. banking lobby’s reaction to yield-bearing stablecoins as “full panic.” While critics often frame this as incumbents defending their turf, the fear is not entirely irrational.

Competitive Pressure Explained

- Average U.S. retail bank deposit rates have struggled to keep pace with inflation.

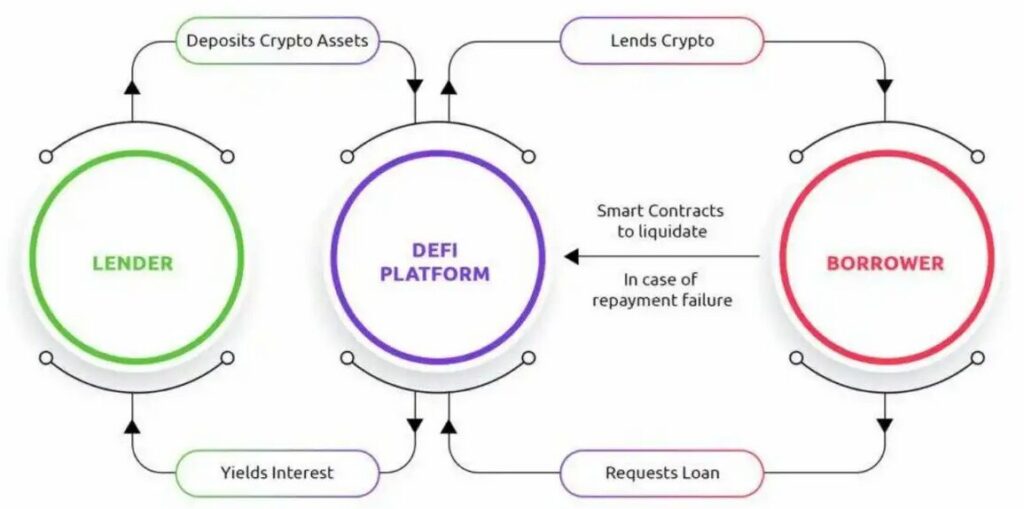

- Stablecoins settle instantly, operate globally, and increasingly integrate with DeFi protocols.

- Adding yield to stablecoins creates a direct substitute for savings accounts—without branch costs or geographic limits.

For consumers, the value proposition is obvious. For banks, it threatens the foundation of deposit-funded lending.

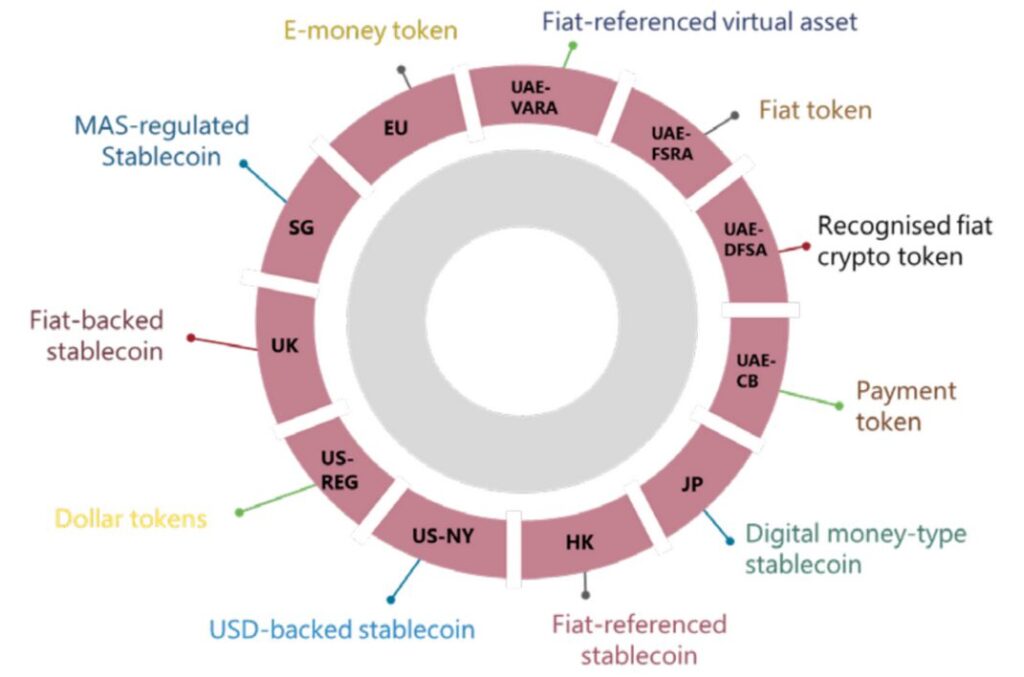

Legislative Response: GENIUS Act and CLARITY Act

GENIUS Act: Guardrails First

Barnum stated that JPMorgan’s position aligns with the GENIUS Act, which focuses on establishing guardrails for stablecoin issuance. The intent is not to ban stablecoins, but to ensure:

- Reserve transparency

- Issuer accountability

- Limits on functional overlap with bank deposits

CLARITY Act: Drawing the Line on Yield

The CLARITY Act, a broader digital asset market structure bill, has placed stablecoin rewards at the center of debate. According to recently released amendments:

- Digital asset service providers would be prohibited from paying interest or yield solely for holding a stablecoin.

- The goal is to prevent stablecoins from functioning as de facto interest-bearing deposits.

This distinction is subtle but critical.

Passive Yield vs. Activity-Based Rewards

Importantly, lawmakers are not rejecting all forms of yield. The proposed framework differentiates between:

Prohibited

- Passive yield earned only by holding a dollar-pegged token.

Potentially Permitted

- Rewards tied to:

- Liquidity provision

- Network validation or staking

- Governance participation

- Other ecosystem-supporting activities

This reflects a regulatory philosophy: returns should compensate risk or contribution, not merely custody.

Why Stablecoins Keep Growing Anyway

Despite regulatory uncertainty, stablecoin adoption continues to accelerate.

Key Drivers

- Faster settlement compared to traditional rails

- Lower transaction costs for cross-border payments

- On-chain transparency and programmability

- Dollar access in emerging and restricted markets

Stablecoins are no longer a niche crypto instrument; they are becoming financial infrastructure.

Implications for Crypto Investors: Where Yield Will Come From Next

For investors seeking yield, the message is clear: passive dollar yield via stablecoins is under pressure. However, this does not eliminate opportunity.

Emerging Yield Pathways

- Protocol-native incentives rather than issuer-paid interest

- Revenue-sharing from transaction fees

- Structured products combining stablecoins with DeFi strategies

- Regulated, bank-issued or bank-partnered stablecoins

The shift favors design sophistication over simplicity.

Implications for Builders: Designing Within the New Reality

For founders and developers, JPMorgan’s warning is a signal to rethink architecture.

Practical Design Takeaways

- Separate settlement tokens from yield mechanisms

- Emphasize utility, not passive holding

- Build compliance-friendly reward logic

- Prepare for disclosure and audit requirements

In practice, this may accelerate hybrid models that blend traditional finance discipline with blockchain efficiency.

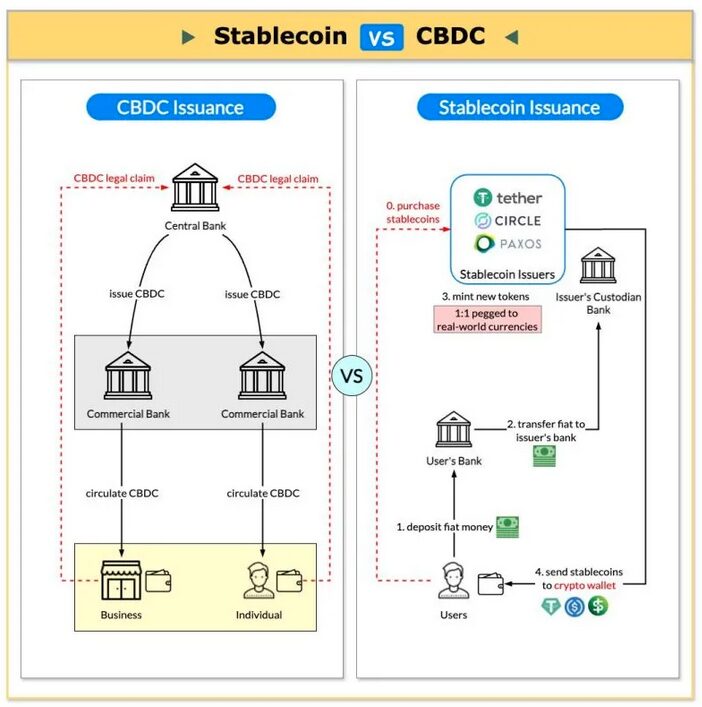

Visual Explanation: Stablecoin Models Compared

(“Comparison of Non-Yield Stablecoins vs Yield-Bearing Stablecoins vs Activity-Based Reward Tokens”)

The Bigger Picture: Two Financial Philosophies Collide

At its core, this debate reflects a deeper tension:

- Banking philosophy prioritizes systemic stability, predictability, and centralized oversight.

- Crypto philosophy prioritizes openness, composability, and market-driven incentives.

Yield-bearing stablecoins sit precisely at the fault line between these worldviews.

Conclusion: A Maturing Market, Not a Rejection of Crypto

JPMorgan’s warning should not be read as an anti-crypto stance. On the contrary, it signals that stablecoins have grown powerful enough to matter at a systemic level.

For investors, the era of “easy yield” is likely ending—but a more sustainable, transparent yield economy is emerging.

For builders, regulatory alignment will become a competitive advantage, not a constraint.

For the broader ecosystem, this moment marks the transition from experimentation to financial adulthood.

The future of stablecoins will not be defined by whether they offer yield—but how, why, and under what rules that yield exists.