Main Points:

- The U.S. SEC is reportedly exploring allowing blockchain-registered shares (stock tokens) to trade on regulated crypto exchanges.

- This represents a potential bridge between traditional finance and decentralized digital assets, reflecting a more collaborative regulatory stance.

- Major players like Robinhood, Coinbase, Kraken, and Nasdaq have already begun or applied for stock-token initiatives.

- Critics warn of regulatory arbitrage and emphasize that tokenization must deliver real value beyond mere gimmicks.

- The tokenization market, especially for real-world assets and securities, is projected to grow rapidly over the coming decade.

- For blockchain and crypto practitioners, the tokenized equity space may offer a promising frontier—but with significant legal, technical, and adoption challenges.

1. Emergence of SEC’s Tokenized Stock Proposal

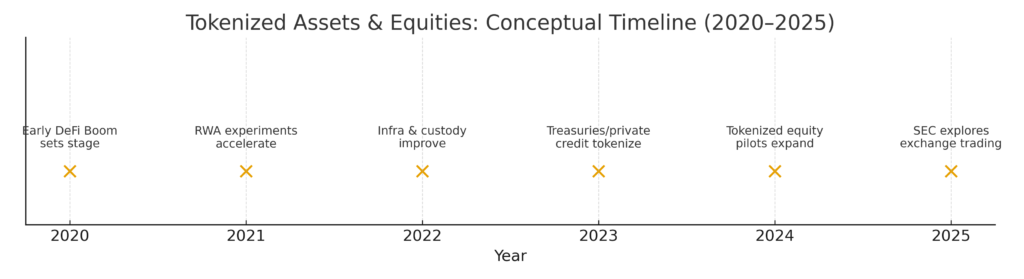

In recent reports, the U.S. Securities and Exchange Commission (SEC) is said to be developing plans to permit blockchain-based versions of public company shares—so-called “stock tokens”—to be bought and sold on qualified cryptocurrency exchanges. Under this concept, each token would represent ownership of an underlying share (or fraction thereof), maintained via token infrastructure and standards.

At present, the initiative is in its early stage, and many of the legal frameworks, custodial requirements, and enforcement safeguards are still being worked out. The Information and related outlets report that the SEC staff is actively exploring how such a system might be integrated with existing securities law regimes.

This proposal goes beyond tokenizing private assets or bond/debt instruments: by targeting mainstream equities (e.g. Tesla, Nvidia), the move signals that tokenized securities could become a core dimension of capital markets.

From the SEC’s side, Commissioner Hester Peirce has publicly expressed support for tokenized securities, urging that regulation should facilitate innovation, rather than stifle it. Nonetheless, she reminds that tokenized securities remain securities—and thus must comply with existing securities laws.

2. Stakeholders & Industry Momentum

2.1 Crypto Firms & Exchanges

Already, several platforms are moving ahead with stock token offerings:

- Robinhood has launched tokenized U.S. equities for European users, allowing 24/7 trading of over 200 stocks and ETFs via Arbitrum, with plans to expand further.

- Kraken is developing “xStocks” on the Solana blockchain, backing them with real shares, allowing users globally (outside the U.S.) to trade tokenized equities.

- Coinbase is reportedly seeking regulatory clearance to list stock tokens.

- Nasdaq has filed rule changes to allow tokenized securities to list and trade on its platform.

Some of these efforts are already live; others are still in application or pilot stages.

2.2 Traditional Finance & Critics

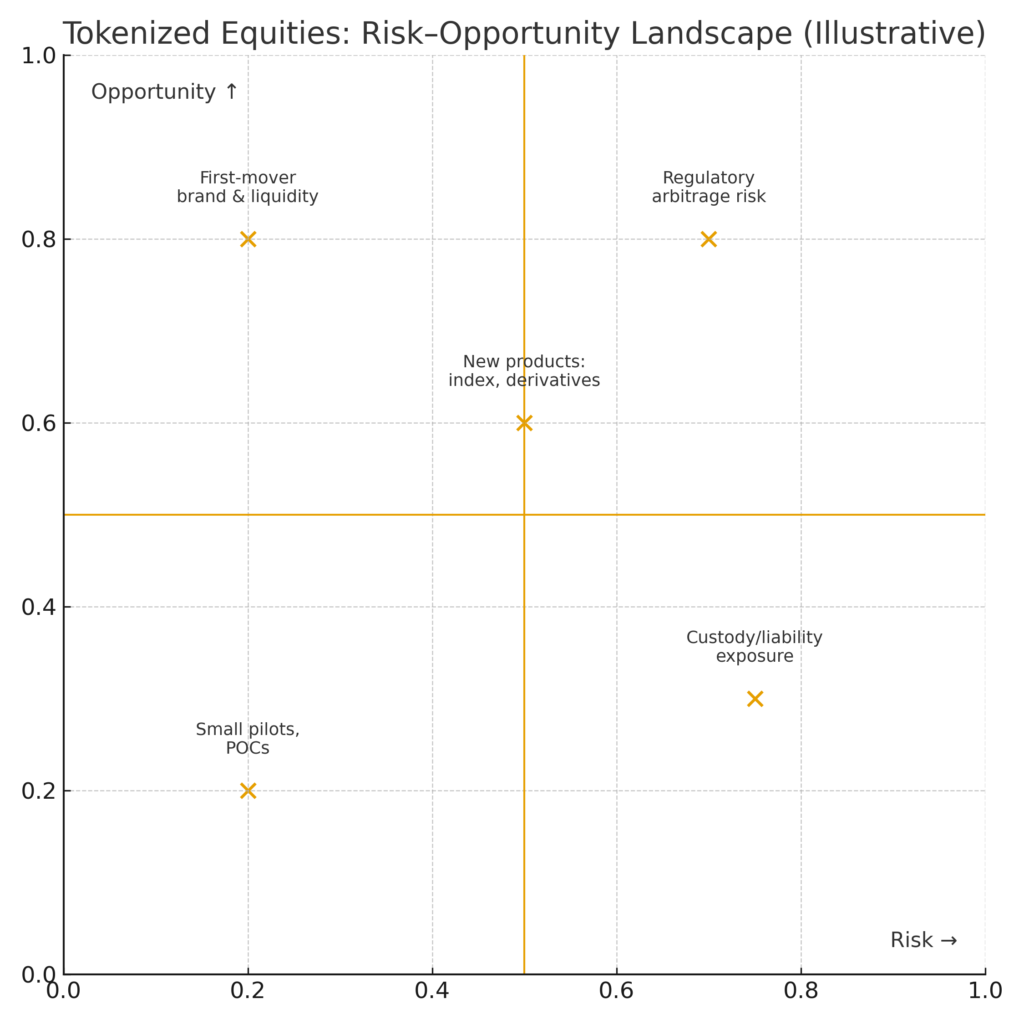

While some in traditional finance see tokenization’s promise to lower costs and increase market access, others remain cautious or even critical. For example, Citadel Securities, in comments to the SEC’s crypto task force, warned against tokenization becoming a loophole for regulatory arbitrage. They argued that tokenization must deliver genuine market efficiency and not merely exploit gaps in oversight.

Part of the tension also arises because the existing equities industry—including brokers, custodians, exchanges, and clearinghouses—has deep infrastructure and entrenched roles that tokenization might disrupt. Aligning interests among incumbents and blockchain innovators will be a delicate process.

2.3 SEC & Regulatory Posture

The SEC’s own Crypto Task Force is charged with clarifying how federal securities law applies to digital assets, including tokenized securities.Meanwhile, the SEC has recently issued a “no-action” letter to crypto startup DoubleZero, suggesting a more collaborative regulatory tone (i.e. based on facts presented, enforcement would not proceed).

Moreover, Commissioner Peirce has indicated that the SEC is open to working directly with tokenization projects to clarify regulatory standards. This marks a shift from purely adversarial enforcement to potential co-design of frameworks.

3. Why Tokenized Stocks Could Matter

3.1 Efficiency, Access, & Cost Reduction

Tokenized stocks offer several potential advantages:

- Fractional ownership: Investors can buy micro-fractions of high-value equities, improving accessibility

- 24/7 trading: Unlike traditional stock markets with fixed hours, token trading could run continuously

- Faster settlement: On-chain settlement can reduce or eliminate multi-day clearing delays

- Lower intermediaries: With fewer middlemen, costs could shrink

- Increased liquidity / market depth: Lower barriers and fractionalization may attract more participants

These features may help democratize equity ownership, especially in jurisdictions with limited access to U.S. markets.

3.2 Market Growth and Tokenization Trends

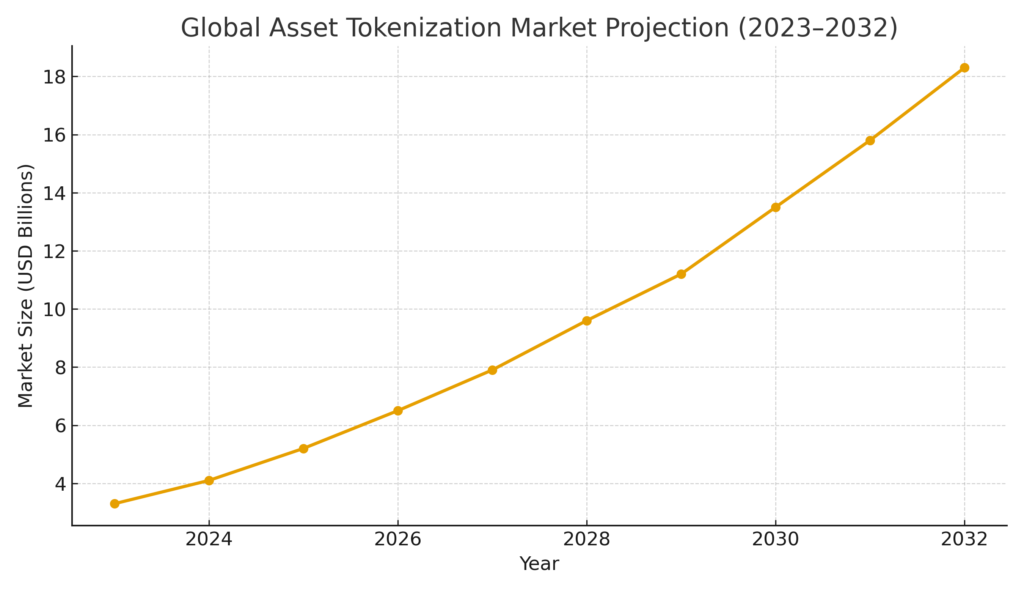

The broader tokenization market (encompassing real estate, debt, commodities, etc.) is projected to grow rapidly. Some forecasts estimate the market will reach USD 12.83 billion by 2032, growing at ~18.3 % CAGR. Others cite even more ambitious figures, suggesting USD 30 trillion in real-world asset tokenization by 2030, led by equities, real estate, bonds, and gold.

In the securities universe, the tokenized securities market is already sizable: in 2023 it was valued at around USD 54 billion, and expected to reach USD 77 billion by 2031 (CAGR ~5.2 %). Another projection sees it growing from ~USD 1.91 billion in 2024 to USD 17.44 billion by 2033 (CAGR ~27.3 %).

These numbers show both the nascency and the upside potential of the tokenized securities sector.

3.3 A “Hybrid Finance” Inflection

Many observers regard stock tokenization as a critical step in evolving from siloed DeFi towards “hybrid finance” (the fusion of traditional finance and on-chain infrastructure). Binance Research compares tokenized equity growth to the early DeFi boom. In this view, tokenized stocks could serve as the on-ramp for institutional flows and real capital markets into blockchain ecosystems.

If even a fraction of global equities migrate to tokenized form, the addressable market is enormous. For example, Binance Research estimates that converting just 1 % of world equity markets to blockchain could yield a USD 1.3 trillion tokenized stock market.

4. Technical, Legal & Adoption Challenges

4.1 Custody & Qualified Custodians

One major question is whether crypto exchanges or platforms would qualify as “qualified custodians” under SEC rules for holding securities. SEC Chair Gary Gensler has warned that just labeling a platform as a custodian doesn’t necessarily meet requirements. Ensuring secure, legally compliant custody of underlying shares is critical.

4.2 Regulatory Harmonization & Compliance

Tokenized stocks are still securities, subject to disclosure, registration, anti-fraud provisions, and cross-border regulation. Harmonizing U.S. securities law with blockchain practices (e.g., token issuance, transfer, redemption, voting) will require new guidance and robust legal guardrails.

Cross-jurisdiction issues loom large: if tokens trade globally, regulators in multiple countries will seek oversight, complicating compliance.

4.3 Market Liquidity & Network Effects

For tokenized equity trading to gain traction, liquidity is crucial. If too few participants enter the market, spreads will remain wide and trading unattractive. Building a critical mass of market makers, retail and institutional users, brokerage integrations, etc., is essential.

4.4 Governance, Voting, Dividends, and Corporate Rights

Translating corporate actions (voting, proxy, dividends, buybacks) into token logic is nontrivial. Ensuring token holders retain conventional shareholder rights—and that corporate governance remains robust—is a non-negotiable requirement.

4.5 Technological Reliability, Scalability & Interoperability

Blockchain infrastructure must be robust, scalable, and interoperable, especially to handle high volumes and integrate with legacy financial systems. Issues of security, finality, and bridging on-chain/off-chain worlds must be addressed.

5. What This Means for Crypto Builders & Investors

If the SEC moves forward, crypto and blockchain practitioners are looking at a compelling new frontier.

- Opportunities for Protocols & Infrastructure: Token standards, custody solutions, oracle bridges, compliance plumbing, settlement layers, and token governance tooling will be in demand.

- Innovative Product Models: Tokenized ETFs, fractionalized equity funds, on-chain derivative overlays, socially composable index tokens—new financial primitives could emerge.

- Cross-selling / Hybrid Models: Platforms offering both tokens and crypto may integrate equity tokens with lending, staking, or DeFi composability.

- Early-Stage Risks & Advantages: Building early means regulatory uncertainty, but also first-mover advantages in protocol adoption, liquidity, branding, and partnerships.

- Institutional On-Ramp: Tokenization may open paths for institutional capital to flow into blockchain-native capital markets, bridging DeFi and TradFi.

That said, prudent actors will need to navigate evolving regulation, capital constraints, compliance burdens, and competitive landscapes.

6. Recent Developments & Sentiment Shifts

Some signals suggest that the SEC’s attitude toward crypto and tokenization is gradually softening:

- The SEC recently issued a no-action letter to DoubleZero, indicating a more cooperative approach toward tokenized companies.

- Commissioner Hester Peirce reiterated that the SEC is willing to engage with tokenization projects, suggesting room for collaboration.

- Meanwhile, the SEC has also streamlined its ETF approval process, reducing approval timelines drastically.

- On the industry side, Robinhood’s EU token stocks initiative (200+ US equities) bolsters the use case for stock token trading.

- Kraken’s “xStocks” ambition also shows serious movement in tokenized equity deployment.

These developments hint at growing regulatory tolerance and industry experimentation, though the U.S. domestic rollout remains uncertain.

Summary

The SEC’s approval of stock tokenization and its ability to be traded on cryptocurrency exchanges could be a historic step in integrating traditional finance and blockchain. Players such as Robinhood, Kraken, Coinbase, and Nasdaq have already begun their work, and the technology, market, and regulatory aspects hold great potential.

However, this path will not be smooth. Many hurdles remain, including custodial responsibility, legal compliance, governance design, liquidity creation, and technical reliability. Furthermore, we must not forget that tokenized stocks are still securities and are subject to existing securities law.

For crypto/blockchain practitioners, the equity token space is likely to be a new growth area. However, careful risk management and regulatory strategies will be key to success.