Main Points :

- The proposed XRPL-native lending protocol (XLS-66d) introduces fixed-term, fixed-rate credit directly at the ledger level.

- Analysts argue this could transform XRP from a speculative asset into collateral and liquidity infrastructure.

- XRPL lending aims to avoid DeFi-style contagion risk through isolated single-asset vaults.

- Institutional demand, regulatory clarity, and tokenized real-world assets (RWA) are converging around XRPL.

- Selling XRP prematurely may mean missing its transition into institutional credit markets.

1. A New Phase for XRP: The Emergence of XRPL Lending

In late December 2025, crypto analyst Brad Kimes, known for his long-running commentary under the “Digital Perspectives” banner, reignited debate within the XRP community with a blunt message: now is not the time to sell XRP.

His argument was not based on short-term price action, but on a structural development that could redefine XRP’s role in global finance: a proposed native lending protocol built directly into the XRP Ledger (XRPL).

The proposal, advanced by Ripple engineer Ed Hennis, envisions XRPL as more than a payments rail. Instead, it positions the ledger as a foundation for predictable, contract-based credit markets—the very infrastructure institutional finance requires before committing serious capital.

Unlike experimental DeFi lending platforms, XRPL lending is designed with fixed terms, fixed interest rates, and ledger-level enforcement, creating a system that resembles traditional credit markets rather than speculative yield farming.

2. The Philosophy Behind “Never Sell XRP”

Kimes’ phrase “never sell XRP” has deep roots in the community. For years, long-term holders have argued that XRP’s true value lies not in trading volatility but in its eventual integration into institutional financial plumbing.

In his December 23 post, Kimes referred to this principle as the “holy grail” of XRP investing—a reminder that assets designed for infrastructure often realize value after adoption, not before.

The lending proposal strengthens this argument by offering a practical alternative to liquidation: using XRP as productive collateral. Instead of selling into the market, holders could eventually deploy XRP to secure fixed-rate loans, preserving upside exposure while unlocking liquidity.

3. How the XRPL Lending Protocol Works (XLS-66d)

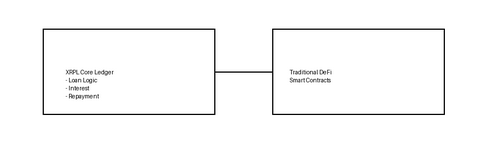

Ledger-Level Credit, Not Smart Contracts

The XRPL lending proposal, formally tracked as XLS-66d, introduces lending primitives directly into the XRPL core. This is a critical distinction.

Rather than relying on external smart contracts—often the source of exploits and systemic failures—XRPL would natively manage:

- Loan terms

- Repayment schedules

- Interest calculations

- Authorization and enforcement

This architecture reflects the operational discipline of traditional finance, where predictability and legal clarity outweigh experimental flexibility.

[XRPL Lending Architecture Diagram]

(Insert here: Diagram showing XRPL core ledger handling loans vs DeFi smart contract layers)

4. Stability by Design: Why XRPL Lending Differs from DeFi

One of the most notable features of the proposal is the single-asset vault model. Each loan exists in isolation, preventing losses from cascading across the system.

This directly addresses a critical weakness in DeFi lending platforms, where shared liquidity pools often amplify market stress. In past downturns, liquidations in one asset class triggered systemic failures across entire protocols.

XRPL lending, by contrast, aims to mirror the compartmentalization of traditional credit markets—closer to bank balance sheets than to automated market experiments.

5. Reduced Collateral Burdens Through Credit Assessment

Another potentially transformative element is the reduced reliance on overcollateralization. While many crypto lending platforms demand collateral far exceeding loan value, XRPL’s model allows for credit-based assessments.

This opens the door to:

- Corporate borrowers

- Payment service providers

- Fintech lenders

- Market makers

By incorporating reputation, history, and contractual obligations, XRPL lending begins to resemble real-world credit underwriting rather than purely algorithmic risk management.

6. Institutional Use Cases Already in Focus

Ed Hennis has outlined several practical applications that highlight XRPL’s institutional orientation:

- Payment companies borrowing USD-linked stablecoins for short-term settlement liquidity

- Market makers borrowing XRP or stable assets for inventory and arbitrage

- SME lenders extending short-term loans using on-chain credit lines

- Cross-border settlement providers smoothing cash flow without selling core assets

These are not hypothetical DeFi experiments. They are extensions of existing financial operations into blockchain-native infrastructure.

7. Validator Governance and the Road to 2026

The proposal is expected to face validator voting by late January 2026. As with all XRPL amendments, adoption requires network-wide consensus.

This governance process itself is significant. Unlike unilateral protocol changes, XRPL’s amendment system ensures that upgrades reflect collective agreement among validators—an essential feature for institutional confidence.

8. XRP Market Context: Price vs Structure

At the time of writing, XRP trades around $1.85, following a sharp rally and subsequent consolidation. Technically, the market remains cautious.

However, institutional signals tell a different story.

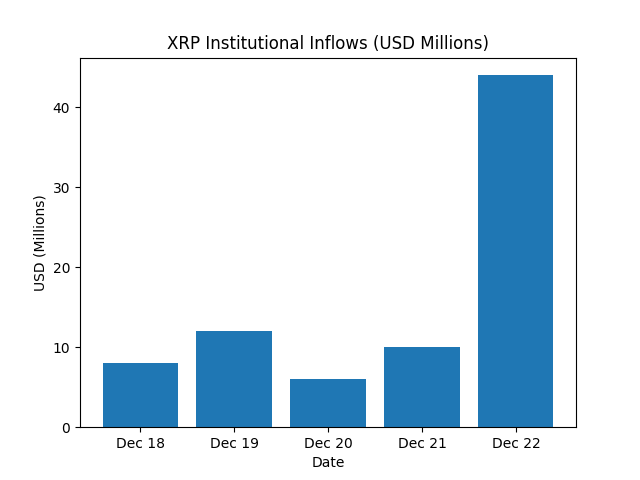

On December 22, XRP investment products recorded $44 million in net inflows in a single day, suggesting accumulation during periods of market hesitation.

[XRP Institutional Inflows Chart]

(Insert here: Bar chart showing daily institutional inflows in USD)

9. Regulatory Clarity Changes the Equation

In August 2025, the long-running legal dispute with the U.S. Securities and Exchange Commission reached a settlement confirming that XRP is not a security.

This ruling removed one of the largest obstacles to institutional adoption. With legal ambiguity reduced, banks, asset managers, and fintech firms can engage with XRP and XRPL-based products with greater confidence.

Regulatory clarity does not drive speculative hype—but it enables infrastructure investment.

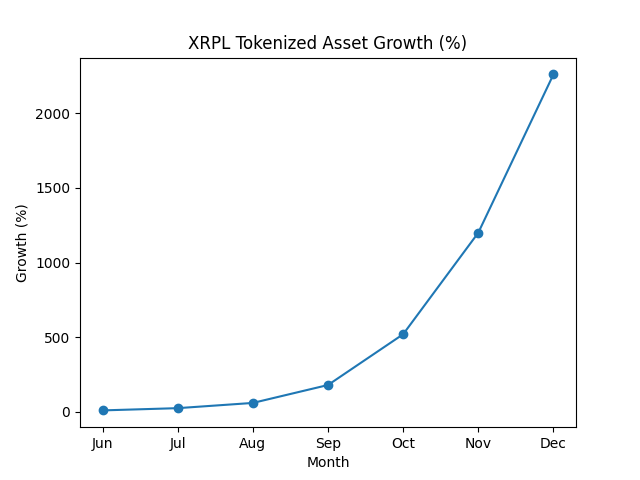

10. Tokenized Assets and the RWA Flywheel

XRPL is also seeing rapid growth in tokenized real-world assets (RWA). Over a recent six-month period, tokenized assets on XRPL reportedly increased by more than 2,260%.

This matters because credit markets thrive on assets. As RWAs expand, so does demand for:

- Collateral management

- Credit issuance

- Settlement liquidity

XRPL lending could become the connective tissue linking tokenized assets, stablecoins, and institutional borrowers.

[XRPL RWA Growth Chart]

(Insert here: Line chart showing exponential growth in tokenized assets on XRPL)

11. Strategic Implications: Hold, Don’t Liquidate?

From a strategic perspective, the lending proposal reframes XRP ownership.

Instead of asking “When should I sell?”, the more relevant question becomes “How can XRP be deployed?”

If XRP evolves into a recognized form of institutional collateral, early liquidation may resemble selling land before infrastructure arrives.

This does not guarantee price appreciation—but it changes the risk-reward calculus entirely.

12. Conclusion: XRP at the Threshold of a Credit Role

The XRPL lending proposal represents more than a technical upgrade. It signals a philosophical shift: from speculative asset to financial instrument.

By embedding credit mechanisms directly into the ledger, XRPL aligns itself with the needs of institutions, not just traders. Combined with regulatory clarity, growing RWA adoption, and observable institutional inflows, the argument for patience becomes compelling.

Whether or not XLS-66d is approved in early 2026, the direction is clear. XRP is no longer just about payments—it is positioning itself as part of the next-generation credit infrastructure.

For investors and operators focused on long-term utility rather than short-term volatility, that distinction may prove decisive.