Main Points:

- Mounting national debt: U.S. federal debt has surpassed $36 trillion, threatening fiscal stability.

- Persistent inflation: Elevated consumer prices erode purchasing power, driving demand for crypto as a hedge.

- Outdated financial infrastructure: Legacy institutions struggle to meet global, low-cost, real-time payments and digital asset needs.

1. A Crisis of Unprecedented National Debt

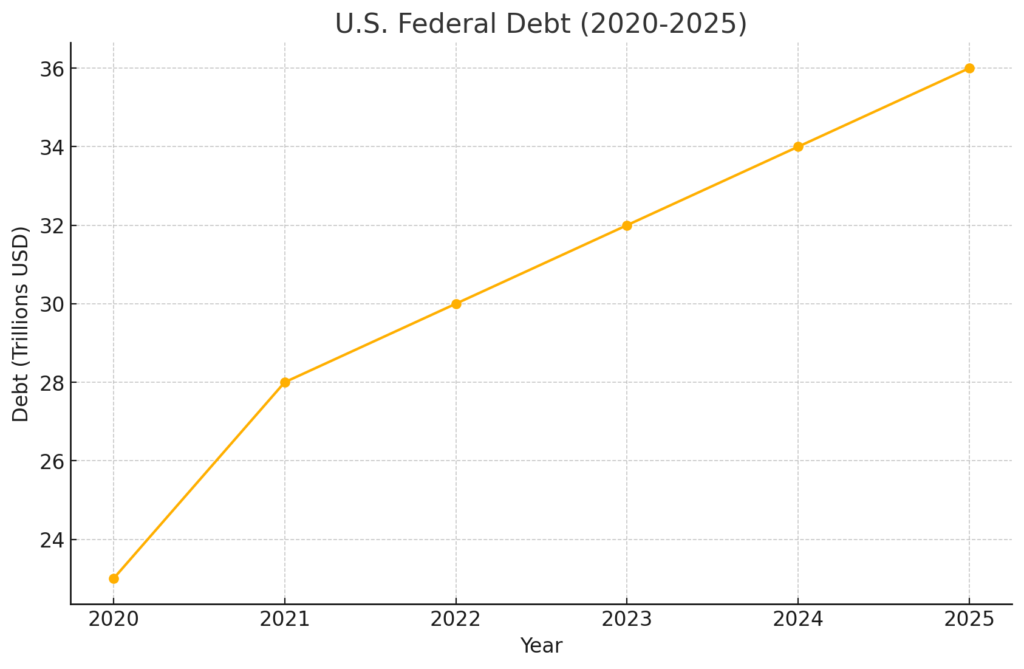

In mid-June 2025, U.S. federal debt officially exceeded $36 trillion, rising from roughly $23 trillion in 2020 to its current level of $36 trillion (see chart below). This growth reflects persistent annual deficits and mounting interest obligations, crowding out other forms of government spending and increasing the risk of fiscal crisis. As sovereign balance sheets weaken, individuals and institutions seek alternative stores of value and mediums of exchange that operate outside traditional credit cycles. Bitcoin’s hard-capped supply and predictable issuance have positioned it as a digital “reserve currency” for hedging against sovereign insolvency.

See U.S. Federal Debt (2020–2025) chart above.

2. Inflation’s Ongoing Toll on Purchasing Power

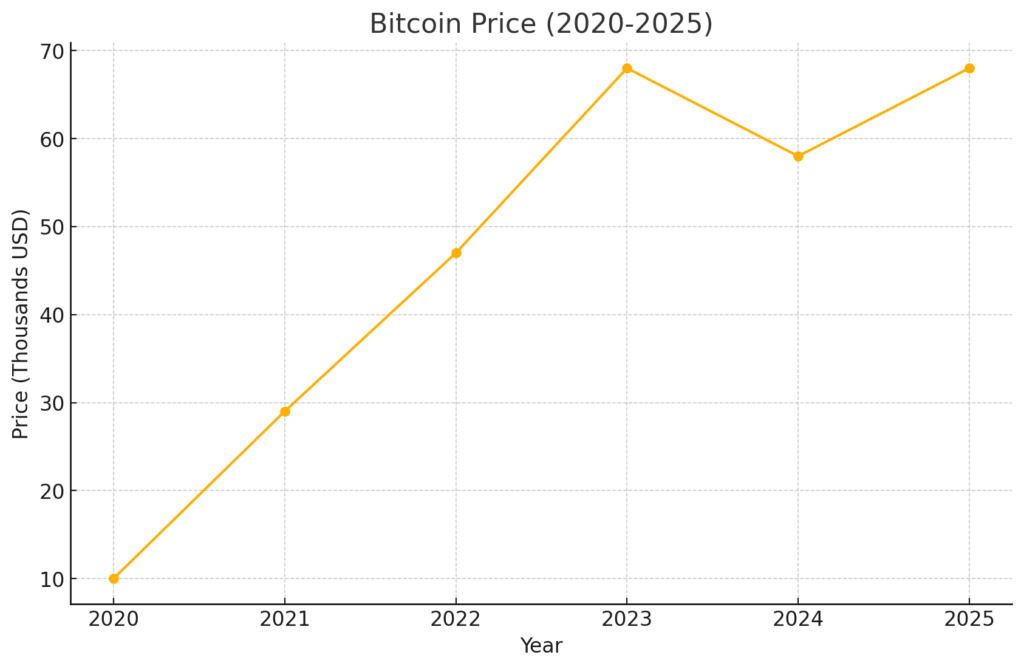

Even after the peak inflation years of 2021–2022, consumer price inflation remains notably above the Federal Reserve’s 2 percent target, hovering near 3–4 percent annually. Persistent inflation—driven by supply chain constraints, fiscal stimulus, and geopolitical tensions—directly reduces real incomes and wealth. In response, both retail and institutional investors have turned to Bitcoin and other crypto assets as inflation hedges. In the past week alone, BTC/EUR trading volume saw a 9 percent surge, pushing Bitcoin prices back toward their all-time highs of approximately $68 000 per coin (see chart below). This reflects broader confidence in crypto’s capacity to preserve purchasing power when fiat currencies falter.

See Bitcoin Price (2020–2025) chart above.

3. Reinventing an Outdated Financial System

Legacy banks and payment rails were built for a different era—characterized by siloed networks, batch settlement processes, and high transaction costs. Brian Armstrong argues that crypto assets represent transformative technology capable of overhauling the entire financial stack. With decentralized networks:

- Individuals regain control: Users can custody their own assets, reducing counterparty risk.

- Cross-border payments accelerate: Transactions settle in seconds or minutes at a fraction of legacy costs.

- New revenue models emerge: Creators (artists, musicians, writers) can monetize directly via tokenized assets (e.g., NFTs), bypassing intermediaries and retaining a larger share of proceeds.

Coinbase actively supports this vision with its payment API suite and Bitcoin rewards card, enabling merchants and consumers to pay in crypto seamlessly.

Recent Trends in the Crypto Landscape

Stablecoins Growing as Corporate Tools

The U.S. Senate’s passage of the GENIUS Act on June 18, 2025, established a federal framework for stablecoins, requiring 100 percent reserves and regular audits for large issuers. This clarity has spurred major banks—Bank of America, Morgan Stanley, Société Générale, Banco Santander—and retailers like Amazon and Walmart to explore or pilot dollar-pegged tokens for payments and liquidity management

Stablecoin Corporate Adoption

Institutional Bitcoin Inflows

Since January 2024, BlackRock’s iShares Bitcoin Trust (IBIT) has amassed over 662 500 BTC (over 3 percent of total supply), representing nearly $72 billion in assets under management. IBIT now commands more than half of all U.S. spot Bitcoin ETF flows, reflecting robust institutional demand for regulated crypto exposure.

Creative Finance and Tokenization

Beyond payments and stores of value, crypto enables novel financing structures. Decentralized finance (DeFi) protocols now total over $200 billion in TVL, offering lending, derivatives, and automated market-making without traditional banks. Meanwhile, NFT marketplaces facilitate direct creator monetization; secondary sales sometimes yield royalty streams for artists, underscoring crypto’s disruptive potential in creative industries (e.g., SuperRare, Zora).

Conclusion

Brian Armstrong’s three pillars—sovereign debt, inflation, and outdated banking—paint a compelling case for why crypto assets matter now more than ever. They offer an escape hatch from fiat vulnerabilities, a hedge against rising prices, and a blueprint for rebuilding finance from the ground up. As stablecoin legislation clarifies regulatory frameworks and institutional products like BlackRock’s IBIT ETF scale Bitcoin exposure, the ecosystem is poised to accelerate its transition from speculative fringe to foundational financial infrastructure.