Main Points :

- Bitcoin fell over 50% from its all-time high near $126,200, triggering the sharpest monthly decline of the year.

- A highly leveraged Asia-originated trade, reportedly involving Hong Kong hedge funds using Japanese yen funding, likely acted as the initial spark.

- Structured products linked to spot Bitcoin ETFs, possibly involving banks such as Morgan Stanley, may have amplified the sell-off through negative gamma hedging.

- Bitcoin miners are quietly pivoting toward AI data centers, increasing BTC sales and weakening on-chain support.

- Long-term holders are no longer aggressively accumulating, signaling a structural transition rather than a simple panic event.

1. Bitcoin’s Steepest Drop in Months: Setting the Stage

Bitcoin (BTC) experienced its most severe monthly downturn in recent memory, plunging to $59,930, its lowest level of the year. This marks a decline of more than 50% from the all-time high of approximately $126,200 recorded in October 2025.

At first glance, the move looked like a familiar crypto panic: leveraged longs flushed out, sentiment flipped, and social media filled with speculation. But as the dust settled, it became clear that this was not merely a retail-driven sell-off. Instead, multiple institutional and structural forces appear to have converged.

To understand what truly happened—and what it means going forward—we need to examine three overlapping narratives:

- A leveraged Asia-based macro trade gone wrong

- ETF-linked structured products triggering forced hedging

- A fundamental shift in miner economics driven by AI infrastructure demand

Each alone might not have caused a 50% drawdown. Together, they created a cascade.

2. The Hong Kong Hedge Fund Hypothesis: When Carry Trades Break

One of the most widely discussed explanations is that the sell-off originated in Asia, particularly among Hong Kong–based hedge funds.

According to Parker White, COO and CIO of Nasdaq-listed DeFi Development (DFDV), several funds had built large, leveraged Bitcoin exposure using a classic carry trade structure:

- Borrow Japanese yen at relatively low interest rates

- Convert yen into dollars or other currencies

- Gain Bitcoin exposure via options linked to spot BTC ETFs, such as BlackRock’s IBIT

This strategy relies on two assumptions:

- Bitcoin continues rising

- Funding costs remain stable

Both assumptions failed.

As Bitcoin’s price stalled and volatility rose, yen funding costs increased, squeezing the trade from both sides. Lenders demanded additional collateral, forcing funds to liquidate Bitcoin and correlated assets quickly.

This is a textbook example of leverage transforming a slow correction into a violent unwind.

What makes this episode particularly important is that it highlights how crypto is now deeply entangled with global FX and macro funding markets. Bitcoin did not fall in isolation—it fell because a cross-currency leverage structure collapsed.

3. Morgan Stanley and the Structured Product Feedback Loop

Another compelling explanation was raised by Arthur Hayes, former CEO of BitMEX. He pointed to the role of structured products linked to spot Bitcoin ETFs.

Morgan Stanley and other large banks reportedly offer products that provide:

- Returns linked to Bitcoin prices

- Principal protection or conditional barriers

- Embedded options structures

These products are popular with wealth management and private banking clients who want crypto exposure without holding BTC directly.

The Critical Level Problem

Many of these products are structured around key price levels, such as $78,700. When Bitcoin trades above the level, the bank’s hedge is manageable. But once the price breaks below it, dealers must sell spot Bitcoin or futures to maintain delta neutrality.

This creates a negative gamma effect:

- Price falls → hedge selling increases

- Hedge selling → price falls further

In this scenario, banks unintentionally shift from liquidity providers to forced sellers, accelerating the downturn.

This mechanism is well known in equity markets, but its growing presence in Bitcoin marks a critical evolution: BTC is now subject to the same derivatives-driven reflexivity as traditional financial assets.

4. Miner Capitulation or Strategic Exit? The AI Pivot

While leverage and structured products explain the speed of the drop, they do not explain the persistent selling pressure. For that, we must look at miners.

Analyst Judge Gibson noted that Bitcoin’s network hash rate has fallen by an estimated 10–40%, a significant move. The reason is not technical failure—it is capital reallocation.

Miners Are Choosing AI Over Bitcoin

Large miners are increasingly shifting resources toward AI-focused data centers, where returns are more predictable.

- In December 2025, Riot Platforms announced a pivot toward data center infrastructure and sold $161 million worth of BTC

- Another miner, IREN, made a similar announcement weeks later

The Hash Ribbon indicator confirmed a negative crossover: the 30-day moving average of hash rate fell below the 60-day average. Historically, this signals miner stress and increased selling risk.

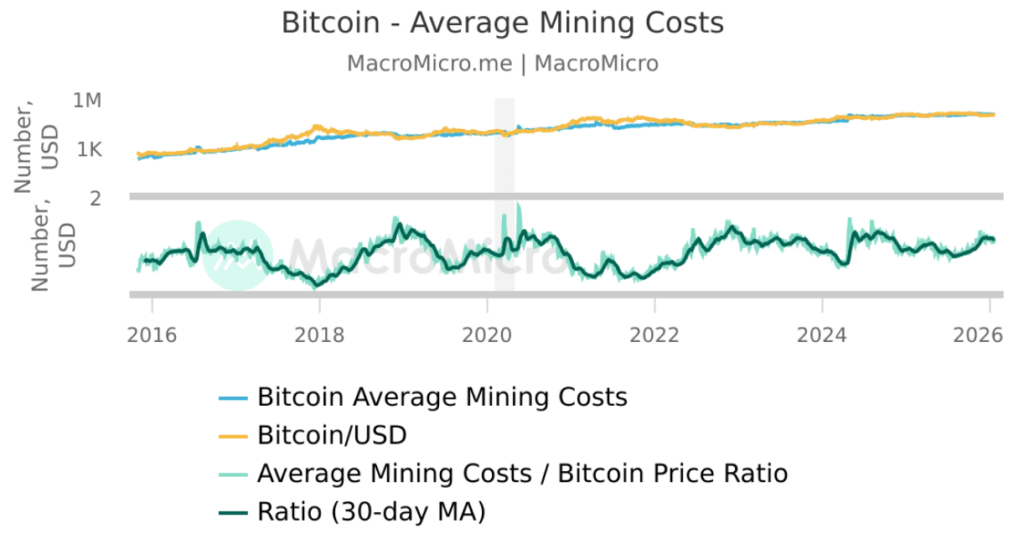

Mining Economics Are Tight

Current estimates suggest:

- Average electricity cost per BTC: $58,160

- Total production cost per BTC: $72,700

If Bitcoin remains below $60,000, many miners face sustained margin pressure. Selling BTC to fund AI infrastructure becomes a rational—if bearish—decision.

This is not panic. It is strategic reallocation.

5. Long-Term Holders Are Stepping Back

On-chain data adds another layer of concern. Wallets holding 10 to 10,000 BTC now control the lowest share of supply in nine months.

This cohort typically represents:

- Funds

- Family offices

- Long-term strategic investors

Their reduced exposure suggests that the market is not merely resetting—it is re-pricing risk.

Instead of aggressively buying dips, these players appear to be waiting for:

- Structural clarity

- Lower volatility

- A new equilibrium between crypto, TradFi, and AI infrastructure

6. What This Means for Investors and Builders

For readers seeking new crypto assets, yield opportunities, or practical blockchain use cases, this crash delivers several lessons:

1. Leverage Is the Hidden Enemy

The most dangerous risks are no longer obvious on-chain leverage but off-chain, cross-asset leverage.

2. ETFs Changed Bitcoin’s Market Microstructure

Spot ETFs brought liquidity—but also imported derivatives reflexivity from traditional finance.

3. AI Is Now a Direct Competitor to Bitcoin Mining

Capital flows follow returns. Bitcoin must now compete with AI for energy and infrastructure investment.

4. The Next Cycle Will Be More Institutional—and More Complex

Future upside will likely favor:

- Infrastructure tokens

- Compliance-friendly DeFi

- Settlement, custody, and tokenization layers

Not purely narrative-driven assets.

7. Conclusion: A Structural Reset, Not the End

Bitcoin’s crash was not caused by a single villain. It was the result of interlocking systems failing simultaneously:

- Leveraged macro trades

- Structured product hedging

- Miner capital rotation

- Cautious long-term holders

This is painful—but also constructive.

Markets are flushing excess leverage, repricing risk, and redefining Bitcoin’s role in a world where AI, traditional finance, and blockchain now compete for the same capital pools.

For serious investors and builders, this is not the end of opportunity. It is the start of a more mature—and more demanding—phase of the crypto economy.