Main Points :

- Rapid growth in crypto adoption across Sub-Saharan Africa, especially Nigeria and Kenya

- Stablecoins becoming foundational for remittances, inflation hedging, and payments

- Blockchain/crypto projects serving communities in slums, SMEs, humanitarian aid

- Key barriers: regulatory uncertainty, fraud, currency sovereignty, volatility

- Emerging lessons from EU’s MiCA regime and calls for inclusive licensing/regulation

- Outlook: Africa has potential to leapfrog legacy systems and chart a new financial frontier

Introduction

Over the past decade, Africa has transformed from a region with limited financial infrastructure into one of the fastest-growing hotspots for digital assets. Traditional banking has struggled to reach millions, making mobile money—and now crypto—an increasingly practical alternative. Heavy remittance costs, volatile local currencies, and constrained access to global financial rails have pushed many to explore digital assets. In recent years, Bitcoin and stablecoins together have become tools not only for speculation, but for day-to-day transfers, savings, and business. This article summarizes the current state of crypto adoption in Africa—especially in Kenya and Nigeria—surveys recent data and trends, and explores how the continent may shape future financial innovation.

Below, I first summarize key developments in narrative form, then translate the same English into Japanese, so readers can access both versions.

Rapid Growth Across Africa: A New Financial Landscape

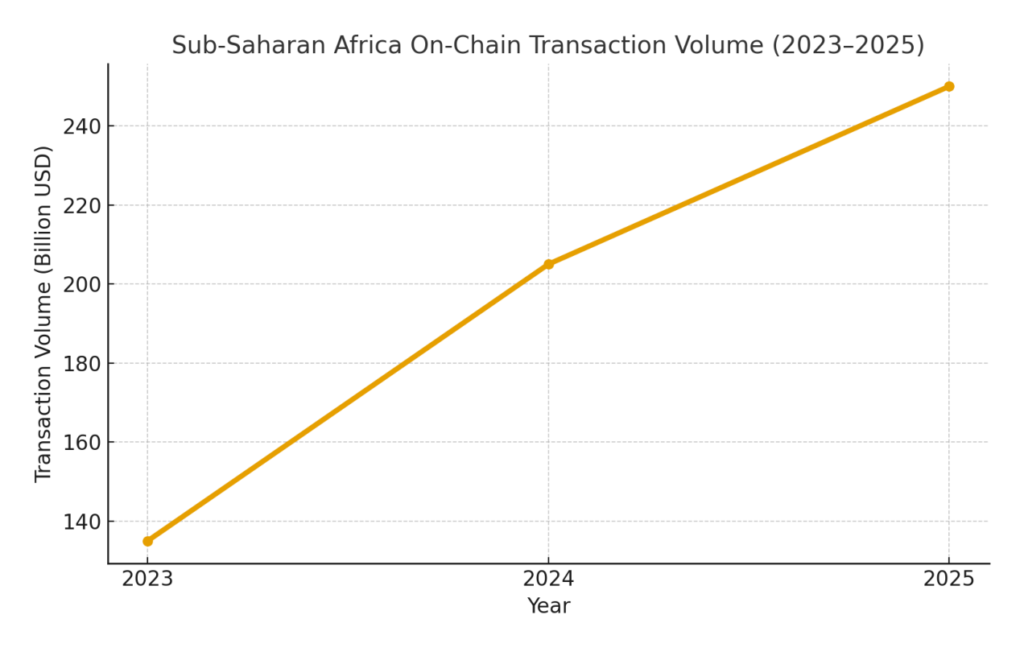

In recent years, Sub-Saharan Africa has recorded some of the highest year-on-year growth rates in cryptocurrency usage globally. According to Chainalysis, between July 2024 and June 2025, on-chain transaction volumes from Sub-Saharan Africa surged, with March 2025 alone reaching nearly US $25 billion, driven largely by a currency devaluation in Nigeria.

Overall, Africa is now commonly cited as among the fastest-growing regions in crypto adoption. Some reports suggest a 45% growth rate year over year, surpassing Latin America. The continent is still a relatively small slice of the global crypto market, but the momentum is clear.

Nigeria has become the continent’s crypto powerhouse. In 2024, Nigeria processed approximately US $59 billion in cryptocurrency volume, with stablecoins accounting for roughly 40 % of that volume. Nigeria’s digital asset user count is estimated in the tens of millions, and its stablecoin adoption rate (9.3 % in Sub-Saharan Africa) leads the region.

In global rankings, Nigeria often appears in the top tier of crypto adoption. For example, Coinpedia lists Nigeria as the top in Africa, with strong peer-to-peer activity. Meanwhile, other countries like Kenya and Ghana continue to support robust local P2P markets.

South Africa, as Africa’s more mature economy, has also moved toward crypto regulation: its financial regulator (FSCA) has approved dozens of crypto licenses, formalizing the space.

In summary, while Africa still occupies a small fraction of global crypto volume, its growth trajectory, younger population, and strong grassroots use make it a region to watch closely.

Kenya’s Case: Innovation Meets Structural Challenges

Kenya offers a microcosm of both the promise and friction of crypto adoption in Africa. The Kenyan shilling has frequently lost value due to inflation, eroding household savings and prompting individuals to seek alternatives in digital assets.

Concurrently, Kenya is home to M-Pesa—one of the world’s most successful mobile money systems. As of 2024, M-Pesa had over 34 million active users; by mid-2025, mobile subscription numbers rose to 45.36 million, supported by 416,000 agents. M-Pesa’s utility contributes significantly to Kenya’s economy: mobile money transactions made up 8.6 % of GDP in 2023, compared to 3.9 % a decade earlier.

Crypto is increasingly bridging with this mobile infrastructure: surveys suggest 82 % of Kenyan users recognize stablecoins (USDT, USDC), and 41 % cite remittance as their primary crypto use case. Over 80 % of users convert via M-Pesa, positioning mobile money as the on-ramp/off-ramp between fiat and crypto.

Politically, Kenya has taken steps toward regulating digital assets. In July 2025, Kenya scrapped a controversial 3 % digital asset tax and replaced it with a 10 % goods & services tax on transaction fees levied by exchanges, wallets, and VASP platforms. A pending Virtual Asset Service Provider Act aims to bring exchanges and wallet providers under the oversight of Kenya’s central bank and capital markets authority.

In terms of grassroots deployment, Afribit (founded 2019) operates in Nairobi’s Kibera slum to help residents use Bitcoin and stablecoin tools for clean water projects, microbusiness support, and savings. Because local households hold value in shillings (vulnerable to inflation), the program offers dollar-pegged “Stablesats” built atop Bitcoin to combine some stability with long-term value accrual.

However, risks persist. Bitcoin’s volatility and the possibility of stablecoin dependence weakening local currency sovereignty are real concerns. Trust is another barrier: many still associate crypto with speculative or fraudulent schemes. Afribit emphasizes that regulation should not exclude the poor, and offers educational efforts, low-entry tools, and sandbox experiments for innovation.

Key Use Cases: Why Crypto Matters in Africa

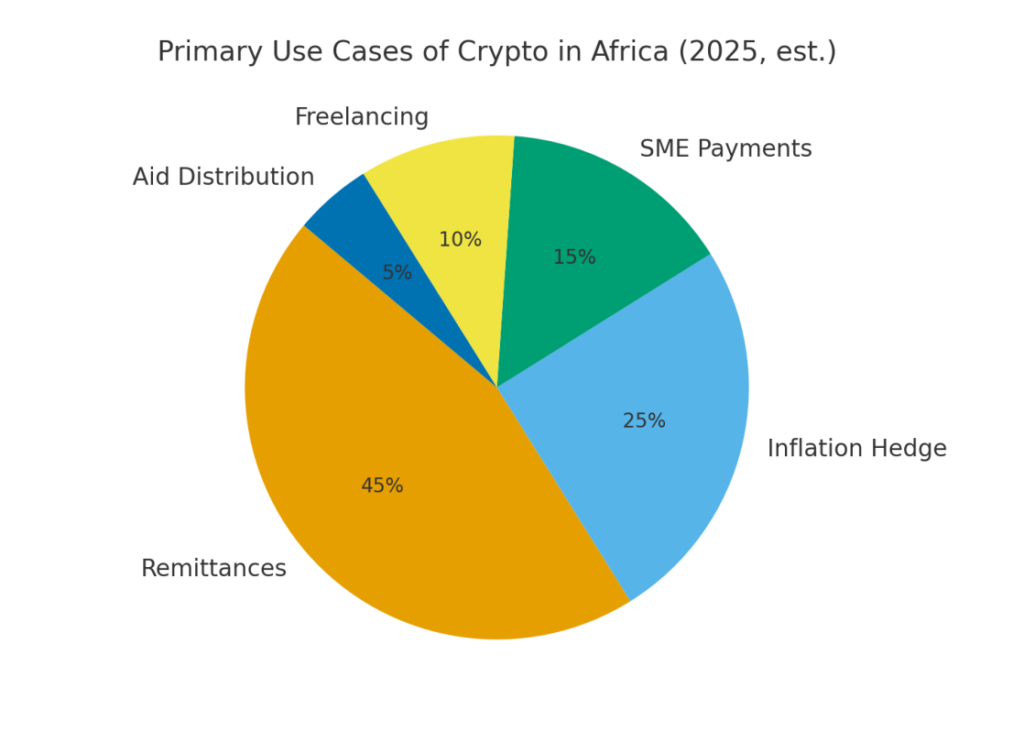

1. Lower-Cost Cross-Border Remittances

Africa has one of the highest remittance costs globally. The World Bank reports average remittance fees of around 8 %, significantly draining funds sent by diaspora.

Crypto, especially stablecoins, often reduces remittance costs to under 1 %, while offering near-instant settlement. For households dependent on remittances, that difference is substantial.

2. Inflation Hedging & Store of Value

Countries like Zimbabwe, Sudan, and Nigeria have experienced runaway inflation, eroding savings almost overnight. In such contexts, dollar-pegged stablecoins function as a lifeline, preserving purchasing power.

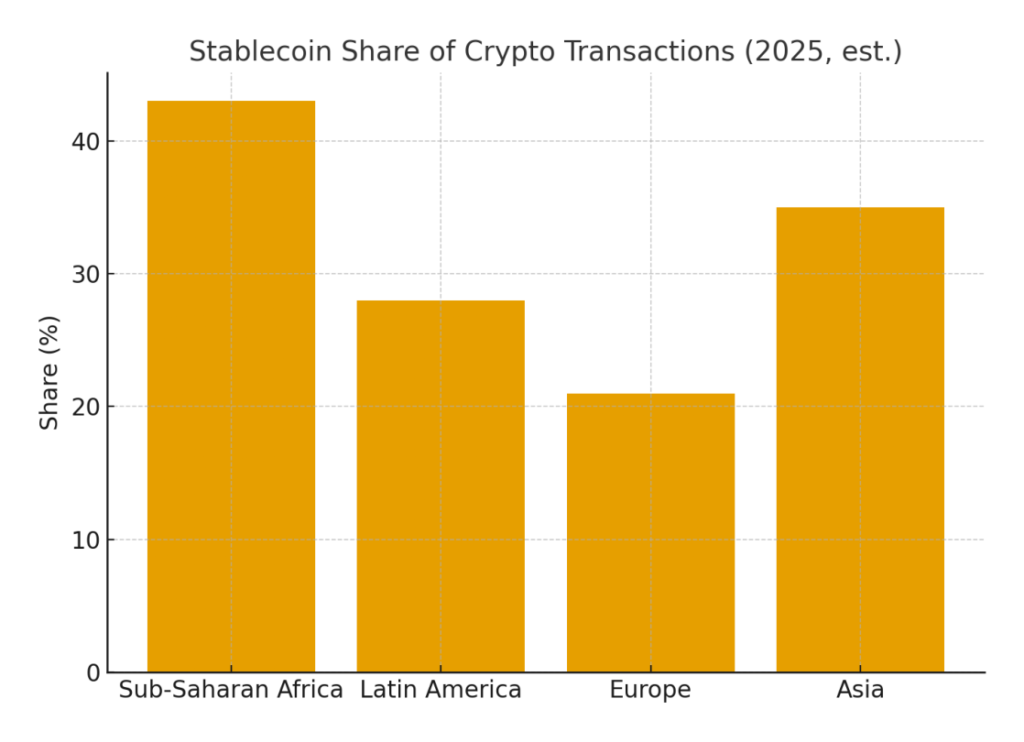

As of 2025, stablecoin transactions in Sub-Saharan Africa make up 40-43 % of all crypto moves—underscoring their importance.

3. SMEs and Entrepreneurial Scaling

Small and medium enterprises (SMEs) in Africa often struggle with cross-border payments, high remittance costs, and limited banking access. Crypto allows them to invoice globally in stablecoins, convert to local currency, and bypass bureaucratic friction.

Platforms like Bitnob in Nigeria, for instance, let SMEs receive stablecoins internationally and manage conversions locally.

4. Gig Economy & Freelancing

Africa’s young, digital-savvy population is increasingly working remotely for global clients. Many prefer receiving payment in stablecoins rather than volatile local currencies. With platforms like Binance Pay and USDT-based remits, stablecoins are becoming the native currency of Africa’s digital workforce.

5. Humanitarian Aid & Transparent Aid Delivery

Blockchain’s transparency and speed make it attractive for aid distribution. Ripple has piloted using RLUSD in Kenya to distribute assistance without exposing recipients to volatility risk. In Kibera, Bitcoin was introduced as a payment tool for vendors and service providers via Afribit’s initiative.

Such models reduce leakage and improve accountability, redefining how aid can be delivered in fragile environments.

6. Integration with Mobile Money

Africa already leads the world in mobile money adoption. Platforms like Kenya’s M-Pesa or Ghana’s MTN Mobile Money process billions annually. Rather than competing, crypto wallets are increasingly linking with mobile money rail—allowing users to move seamlessly between fiat and crypto via their familiar mobile interfaces.

This hybrid approach lowers the psychological barrier to adoption and allows crypto to seep into everyday use rather than remain niche.

Obstacles & Risks

Regulatory Uncertainty & Fragmentation

Many African countries have yet to issue clear crypto rules. This ambiguity creates risk for startups, investors, and users. Nigeria, for example, has oscillated between bans and promotion, causing policy whiplash.

Kenya’s VASP bill remains pending, leaving licensing criteria opaque. Without regulatory clarity, businesses may hesitate to invest or scale.

Fraud, Scams & Trust Deficit

Fraud remains a significant threat. Ponzi schemes disguised as crypto products have targeted vulnerable populations. In Uganda, for example, DunamisCoin collapsed, wiping out community savings.

To counteract this, stronger consumer protection, disclosures, audit standards, and transparency are essential.

Volatility vs. Stability Tradeoffs

Bitcoin’s volatility makes everyday use risky for many. On the other hand, over reliance on foreign-issued stablecoins raises concerns about monetary sovereignty. Governments may fear that widespread adoption of dollar-pegged instruments undermines their ability to manage national currency and monetary policy.

Compliance Costs & Exclusion

Heavy compliance burdens (e.g., Know Your Customer, capital requirements) may stifle grassroots innovation. Projects like Afribit emphasize inclusive regulation that avoids shutting out low-resource communities.

Infrastructure & Access Gaps

Internet access, smartphone penetration, and digital literacy remain uneven. Rural regions may lag, creating a digital divide in crypto adoption.

Additionally, integrating crypto rails with local banking and mobile money infrastructure requires technological and policy coordination.

Learning from MiCA: A Template for Africa

The EU’s Markets in Crypto-Assets (MiCA) regulatory framework offers instructive lessons. MiCA classifies token types, dictates reserve requirements for stablecoins, standardizes disclosure obligations, and unifies rules across nations to reduce fragmentation.

Africa could adopt a similar umbrella approach via continental bodies like the African Union (AU), ECOWAS, or the East African Community (EAC). Harmonized regulation would facilitate cross-border crypto flows and reduce jurisdictional arbitrage.

Licensing should aim to protect users without locking out small innovators. Tiered compliance, regulatory sandboxes, and consistent oversight could balance inclusion and vigilance. Recent Developments & Emerging Signals

- A Standard Chartered report estimates U.S. dollar–backed stablecoins could displace US $1 trillion from emerging market bank deposits over the next three years as people shift savings into stablecoins.

- In Kibera (Kenya), approximately 200 residents now transact in Bitcoin via Afribit’s program, including garbage collectors and vendors.

- South Africa’s regulator has authorized 59 crypto business licenses, signaling regulatory maturation in one of Africa’s biggest economies.

- Morocco, long banning crypto, is now drafting legislation and considering a CBDC for cross-border payments.

- At SiGMA Africa 2025, speakers emphasized the shift from retail speculation to institutional adoption and integration of crypto into commerce and payments.

These developments underscore that Africa is not only experimenting at the grassroots level but also attracting regulatory and institutional attention.

Outlook & Strategic Imperatives

Africa’s chance lies in leveraging its unique position: mobile money ubiquity, youthful populations, and a yearning for alternatives to failing monetary systems. If properly nurtured, this could allow the continent to bypass legacy banking models and lead financial innovation globally.

For those seeking new crypto projects or investment opportunities, Africa offers fertile ground: stablecoin infrastructure, cross-border payment rails, DeFi applications tailored to local needs, tokenized credit and lending platforms, and humanitarian aid solutions.

But success depends on solving the following:

- Regulatory clarity and harmonization: working with regional bodies to set shared standards

- Inclusive licensing & sandbox frameworks: protecting users without strangling grassroots innovation

- Robust consumer protection: audits, transparency, disclosure, anti-fraud mechanisms

- Bridging fiat–crypto rails: seamless mobile money integration

- Education and trust-building: clarifying myths, improving financial literacy

If these elements come together, Africa could become a blueprint for global crypto adoption—not by catching up, but by leaping ahead.

In summary, Africa’s crypto story is not a footnote—it could be a new chapter in the global financial era.