Main Points :

- The White House has convened crypto and banking leaders to resolve disputes over how stablecoin yield should be treated in pending U.S. market structure legislation.

- The outcome of these discussions could determine whether stablecoins remain mere payment instruments or evolve into yield-bearing financial primitives.

- Ongoing negotiations reflect deeper tensions between traditional banking, DeFi innovation, and regulatory clarity.

- For investors and builders, the debate signals where the next generation of revenue models and tokenized financial products may emerge in the U.S. market.

Introduction: Why Stablecoins Are Now a White House Priority

Stablecoins have quietly become one of the most important infrastructures in the global digital asset economy. Pegged primarily to the U.S. dollar, they function as the settlement layer for crypto trading, decentralized finance (DeFi), cross-border payments, and increasingly, tokenized real-world assets.

Against this backdrop, senior officials from the administration of President Donald Trump recently met with representatives from the cryptocurrency industry and the traditional banking sector at the White House. The focus of the meeting was not merely regulatory housekeeping—it was the unresolved question of how stablecoin yield and rewards should be treated under U.S. law.

The talks center on provisions within the Digital Asset Market Clarity Act, a market structure bill currently under consideration in the U.S. Senate. At stake is whether stablecoins can legally distribute yield, and if so, under what regulatory framework. This question has implications that reach far beyond stablecoins themselves, touching tokenized securities, DeFi protocols, and even the ethical rules governing public officials’ digital asset holdings.

The Core Issue: Stablecoin Yield and Regulatory Ambiguity

At the heart of the discussion lies a deceptively simple question:

Should stablecoins be allowed to generate and distribute yield to users?

From a technical perspective, many stablecoin issuers already earn yield. Dollar-backed stablecoins typically hold reserves in short-term U.S. Treasury bills or cash equivalents. With U.S. interest rates hovering in the 4–5% range, these reserves generate billions of dollars in annual interest income.

The controversy arises over who is allowed to receive that yield.

- Banks argue that allowing stablecoins to distribute yield directly to users risks creating unregulated deposit-like instruments.

- Crypto firms counter that preventing yield distribution entrenches incumbents and undermines innovation, especially when users already bear counterparty and protocol risk.

- Regulators worry that yield-bearing stablecoins may blur the line between payments, securities, and collective investment schemes.

The White House meeting aimed to narrow these differences and unblock legislative progress that has stalled since January.

Inside the White House Meeting: Industry and Government at the Same Table

According to public statements, the meeting included representatives from major crypto advocacy groups such as the Digital Chamber, the Crypto Council for Innovation, and the Blockchain Association, alongside traditional financial representatives from the American Bankers Association.

Cody Carbone, CEO of the Digital Chamber, described the meeting as a meaningful step forward, emphasizing that stablecoin yield treatment is one of the biggest remaining obstacles to advancing market structure legislation.

Patrick DeWitt, the White House’s crypto adviser, characterized the discussions as “constructive, fact-based, and solution-oriented,” expressing confidence that stakeholders are close to a workable compromise.

Importantly, these talks occurred while the U.S. federal government was experiencing a partial shutdown, underscoring how strategically important digital asset policy has become—even amid broader political gridlock.

Market Structure Legislation: A Senate Divided

The broader legislative context is complex. Responsibility for digital asset oversight in the U.S. is split primarily between:

- The Senate Banking Committee, which oversees the Securities and Exchange Commission (SEC).

- The Senate Agriculture Committee, which oversees the Commodity Futures Trading Commission (CFTC).

Recently, the Senate Agriculture Committee advanced its own version of the market structure bill without Democratic support. One major point of contention was whether public officials should be allowed to hold or invest in digital assets, a concern raised repeatedly by Democratic lawmakers.

Before any bill reaches a full Senate vote, these competing versions must be reconciled—a process made more difficult by disagreements over stablecoins, DeFi, and tokenized equities.

Stablecoins as Financial Infrastructure, Not Just Crypto Tools

To understand why this debate matters, it is essential to recognize how stablecoins are already used in practice.

Stablecoins now serve as:

- The primary quote currency on global crypto exchanges.

- The settlement asset for DeFi lending, derivatives, and liquidity pools.

- A bridge currency for cross-border remittances, often cheaper and faster than traditional correspondent banking.

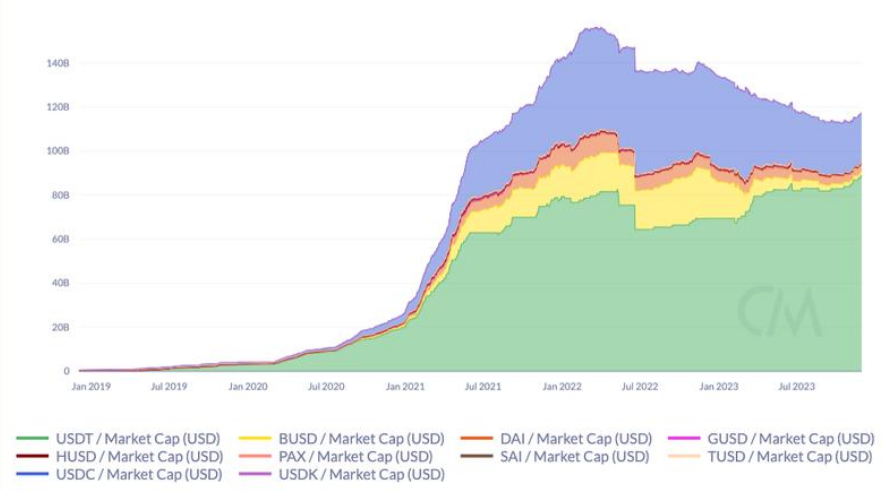

Global Stablecoin Market Capitalization (in $ billions, USD-based)

As of recent estimates, the total stablecoin market capitalization exceeds $130 billion, with transaction volumes that rival major card networks on certain days. This scale makes regulatory clarity unavoidable.

Yield-Bearing Stablecoins: Threat or Evolution?

From an investor and builder perspective, yield-bearing stablecoins represent a natural evolution rather than a radical departure.

In traditional finance:

- Money market funds distribute yield.

- Bank deposits generate interest (albeit unevenly passed on to customers).

- Treasury-backed instruments are widely accessible.

In crypto:

- Yield is often generated via transparent, on-chain mechanisms.

- Users can audit reserve backing and smart contract behavior.

- Risk is explicit rather than hidden behind balance sheets.

The question policymakers face is not whether yield exists, but how transparently and fairly it is allocated.

Implications for DeFi and Tokenized Assets

The stablecoin yield debate also affects adjacent innovations:

Tokenized Stocks and Bonds

If stablecoins are barred from distributing yield, tokenized securities may face similar restrictions, limiting their attractiveness compared to traditional instruments.

DeFi Protocols

Many DeFi systems rely on stablecoins as base collateral. Restrictions on yield could push innovation offshore, weakening U.S. competitiveness.

Institutional Adoption

Banks exploring tokenized deposits and blockchain settlement systems need clarity on whether their digital liabilities can compete with crypto-native stablecoins on equal terms.

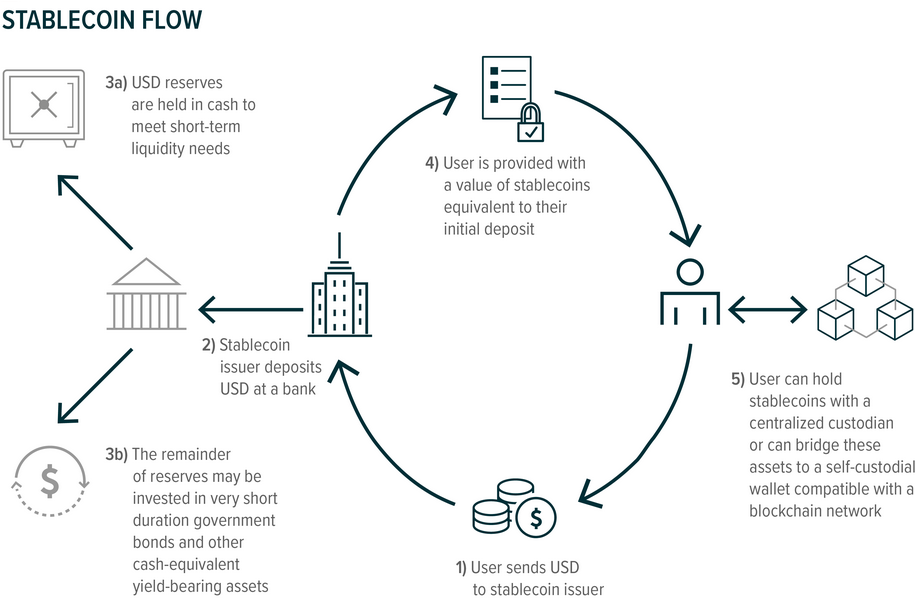

Stablecoin Yield Flow (Reserves → Interest → Issuer vs User)

Banking Industry Concerns: Competition and Systemic Risk

Traditional banks are not opposed to stablecoins per se. In fact, many are experimenting with blockchain-based settlement and tokenized deposits. Their concern lies in regulatory asymmetry.

Banks argue that:

- They are subject to capital requirements, deposit insurance fees, and consumer protection rules.

- Yield-bearing stablecoins could attract deposits without equivalent safeguards.

- A rapid migration of deposits could stress the traditional banking system during periods of market volatility.

These concerns are not unfounded, but crypto advocates note that shadow banking already exists—often with far less transparency than blockchain-based systems.

Global Context: The U.S. Is Not Alone

Internationally, other jurisdictions are moving faster:

- The European Union’s MiCA framework provides clearer rules for stablecoin issuance.

- Singapore and Hong Kong are actively licensing stablecoin operators.

- Emerging markets increasingly rely on USD stablecoins for dollar access.

If U.S. legislation remains stalled, innovation and capital may continue to flow abroad.

What This Means for Crypto Investors and Builders

For readers seeking new crypto assets and revenue opportunities, several signals stand out:

- Stablecoin infrastructure tokens may gain value as regulation legitimizes on-chain finance.

- Yield design will become a competitive differentiator—whether yield accrues to users, DAOs, or issuers.

- Compliance-first DeFi projects are likely to attract institutional partnerships.

- Builders should expect tighter integration between banks and blockchain rails rather than outright replacement.

Conclusion: A Pivotal Moment for Digital Finance

The White House–led discussions on stablecoins mark a turning point. What may appear to be a technical debate over yield is, in reality, a referendum on the future shape of money, banking, and financial innovation in the United States.

If lawmakers succeed in crafting a balanced framework, stablecoins could become the foundation of a more open, efficient, and programmable financial system. If they fail, the next wave of growth may happen elsewhere.

For investors, developers, and institutions alike, this is not a moment to watch passively—it is a moment to prepare.