Main Points :

- A sharp and prolonged decline in Ethereum’s price could, in theory, weaken validator participation and the economic security that underpins permissionless blockchains.

- Even if native tokens lose value, stablecoins and tokenized assets running on the same infrastructure may still face operational and security risks.

- Counterarguments highlight Ethereum’s adaptive incentives, long attack timelines, and high residual costs, suggesting resilience rather than fragility.

- Regulators face a strategic choice: restrict public blockchains for critical finance, or allow them with robust risk-mitigation frameworks.

- For investors and builders, the debate reveals where future opportunities lie: infrastructure hardening, redundancy, and compliance-ready blockchain design.

1. Introduction: Why Ethereum’s Price Matters Beyond Speculation

Ethereum is no longer just a speculative asset or a playground for decentralized finance enthusiasts. It has evolved into a general-purpose settlement layer for stablecoins, tokenized securities, NFTs, and enterprise blockchain applications. As such, its reliability as infrastructure increasingly resembles that of traditional payment rails.

A recent paper by economist Claudia Biancotti of the Italian central bank raises a provocative question: what happens if Ethereum’s price collapses? More precisely, could a sustained decline in ETH undermine the blockchain’s ability to function as a secure and reliable settlement infrastructure?

This question is especially relevant for readers seeking new crypto assets, alternative revenue streams, and practical blockchain applications. Understanding systemic risk is not only about downside protection—it is also about identifying where the next wave of innovation and value creation will emerge.

2. Permissionless Blockchains as Financial Infrastructure

Biancotti’s analysis focuses on permissionless blockchains, defined as networks where anyone can participate in transaction validation (as a validator), without centralized authorization. Ethereum is the canonical example.

These networks are operated by independent, decentralized validators who stake the native token (ETH) and earn rewards for proposing and validating blocks. This design replaces traditional trust in institutions with economic incentives and cryptography.

Crucially, Ethereum is assumed not merely as a network for ETH transfers, but as an infrastructure supporting:

- Stablecoins pegged to fiat currencies,

- Tokenized equities and bonds,

- Other real-world assets represented on-chain.

In this context, Ethereum’s price is not just an investment metric—it directly influences the economic security budget of the network.

3. Validator Economics Under a Price Collapse

According to Biancotti, a large and sustained drop in ETH’s price could trigger a chain reaction.

First, validator rewards—denominated in ETH—would lose fiat value. If rewards fall below operational costs (hardware, cloud services, energy, compliance), validators may exit the network.

A significant reduction in active validators could lead to:

- Slower transaction finality,

- Congestion and settlement delays,

- In extreme cases, partial or full network halts.

From the perspective of payment infrastructure, even short-lived disruptions can be unacceptable, especially when stablecoins or tokenized securities are involved.

4. The Economic Security Budget and Attack Risk

Beyond performance issues, Biancotti emphasizes security risks. Ethereum’s security relies on the cost of attacking the network exceeding the potential gains.

To successfully perform a so-called 51% attack, an attacker would need to control more than half of all staked ETH. This required investment is referred to as the economic security budget—the minimum capital necessary to compromise the network.

If ETH’s price collapses:

- The dollar cost of acquiring majority stake declines,

- The barrier to attacks such as double spending is reduced,

- Theoretically, malicious actors could rewrite transaction history.

This is particularly concerning because even if ETH itself loses value, assets built on Ethereum may not.

5. Stablecoins and Tokenized Assets: Collateral Damage

A key insight of the paper is that Ethereum’s native token and the assets running on top of it can diverge in value.

For example:

- ETH could lose most of its market value,

- Yet stablecoins pegged to $1 or tokenized bonds could retain full economic value.

In such a scenario, attackers would have strong incentives to target the infrastructure, not the token itself. If the blockchain’s integrity is compromised, high-value assets riding on it become vulnerable to manipulation, double spending, or censorship.

This distinction is critical for institutional adoption: infrastructure risk does not disappear simply because the native token is volatile.

6. Quantifying the Cost of Attacking Ethereum

It is important to balance theoretical risk with empirical analysis. In February 2024, Coin Metrics researcher Lucas Nuzzi estimated the feasibility of a 51% attack on Ethereum.

At that time:

- ETH was priced around $2,800,

- A successful attack would require more than $34 billion in capital,

- Due to staking withdrawal and activation limits, it would take approximately six months to assemble the required stake.

As of now, ETH trades closer to $3,300, implying an even higher security budget in dollar terms.

These parameters significantly constrain attackers, making opportunistic attacks unrealistic under normal market conditions.

7. Counterarguments: Why Ethereum May Be More Resilient Than It Appears

Many experts contest the notion that a price crash would lead to immediate infrastructure failure.

First, Ethereum’s protocol is adaptive. As validators exit:

- The reward rate for remaining validators automatically increases,

- Participation incentives strengthen,

- Equilibrium is restored without centralized intervention.

Second, even after a severe price decline, the absolute cost of an attack would likely remain in the tens of billions of dollars, combined with months of preparation and high execution risk.

Third, attacks on a global, highly visible network would face rapid detection, social coordination, and potential countermeasures, including chain reorganizations or emergency governance responses.

From this perspective, Ethereum’s security model is not fragile, but robust by design, albeit not invulnerable.

8. Regulatory Choices: Restrict or Mitigate?

Biancotti concludes by outlining two broad regulatory paths.

Option 1: Restriction

Regulators could decide that public blockchains dependent on volatile native tokens are unsuitable for regulated financial institutions. Under this view, permissioned or centrally governed ledgers would be favored for critical financial infrastructure.

Option 2: Conditional Adoption with Risk Mitigation

Alternatively, regulators could allow the use of public blockchains, provided robust safeguards are implemented. This path is more innovation-friendly but significantly more complex.

Biancotti suggests that the most realistic solution lies in obligations imposed on asset issuers, rather than the blockchain itself.

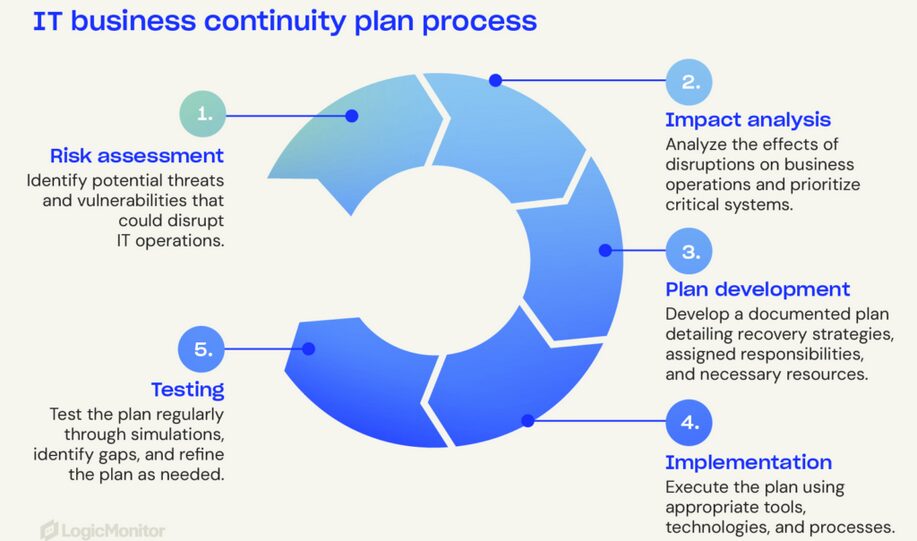

9. Business Continuity, Redundancy, and Alternative Chains

One proposed mitigation measure aligns with recommendations from the Basel Committee on Banking Supervision: business continuity planning.

Concrete examples include:

- Maintaining off-chain databases of asset ownership,

- Pre-selecting alternative blockchains for emergency migration,

- Establishing legal and operational frameworks for asset reissuance.

Additionally, regulators could mandate minimum economic security thresholds, effectively banning the use of blockchains that fail to meet defined resilience criteria.

10. Implications for Investors and Builders

For readers seeking new opportunities, this debate is not merely academic.

Potential growth areas include:

- Blockchain redundancy and interoperability solutions,

- Security analytics and risk monitoring tools,

- Compliance-ready stablecoin and tokenization platforms,

- Infrastructure services that abstract away native token volatility.

Rather than signaling the end of public blockchains, the discussion highlights where value will concentrate next: in making decentralized infrastructure robust enough for global finance.

11. Conclusion: Risk as a Catalyst, Not a Dead End

The Italian central bank paper serves as a valuable stress test for assumptions around blockchain-based financial infrastructure. It reminds us that economic incentives matter, and that infrastructure built on volatile assets must be examined with rigor.

Yet, the counterarguments are equally compelling. Ethereum’s design incorporates adaptive mechanisms, high attack costs, and social resilience that resemble, in many ways, the safeguards of traditional financial systems.

For investors, entrepreneurs, and technologists, the key takeaway is clear:

the future lies not in ignoring these risks, but in building systems that manage them intelligently.

In that sense, discussions about Ethereum’s potential price collapse are less about fear—and more about where the next generation of blockchain innovation will emerge.