Key Takeaways :

- Visa has launched a dedicated enterprise stablecoin advisory and implementation program led by Visa Consulting & Analytics (VCA).

- The initiative goes beyond experimentation, offering end-to-end support from strategy design to technical deployment.

- Stablecoins are transitioning from crypto-native tools into regulated financial infrastructure, driven by banks, fintechs, and global merchants.

- Market projections suggest stablecoin issuance could grow from roughly $280 billion in 2025 to as much as $1.9–$4.0 trillion by 2030.

- Visa’s move positions it as a core infrastructure provider in programmable, blockchain-based global payments.

1. Visa Launches Enterprise Stablecoin Advisory and Implementation Support

On December 15, 2025, Visa announced the launch of a new enterprise-focused program titled the Stablecoin Advisory Practice, aimed at supporting corporations, banks, fintech firms, and merchants seeking to deploy stablecoin-based payment and settlement solutions.

Unlike earlier pilot programs that focused primarily on proof-of-concept testing, this initiative represents a structural shift in Visa’s strategy. The program is operated by Visa Consulting & Analytics (VCA), Visa’s specialized advisory arm, and is designed to provide comprehensive support ranging from early-stage education to full technical and operational implementation.

Visa has been actively accumulating expertise in the stablecoin domain. In 2023, the company conducted pilot payment programs using USD Coin (USDC), demonstrating on-chain settlement feasibility for cross-border transactions. Since then, Visa has expanded significantly, enabling more than 130 stablecoin-linked card programs across over 40 countries, reflecting growing institutional demand.

This new advisory service formalizes those experiences into a scalable offering, signaling that Visa views stablecoins not as experimental crypto assets, but as a foundational component of modern global payments infrastructure.

2. The Strategic Role of Visa Consulting & Analytics (VCA)

Visa Consulting & Analytics serves as the backbone of this initiative. VCA brings together consultants, data scientists, product specialists, and payment infrastructure experts across Visa’s global network.

Through the Stablecoin Advisory Practice, VCA offers:

- Education and executive briefings on stablecoin mechanics, risks, and regulatory frameworks

- Market and use-case analysis, including treasury management, cross-border settlement, and merchant payments

- Strategic design, helping enterprises decide whether to issue, integrate, or accept stablecoins

- Technical and operational support, including blockchain selection, custody models, and compliance alignment

Karl Rutstein, Global Head of VCA, emphasized that clients increasingly seek guidance not only on payments, but on navigating structural transformation across financial systems. As payment rails evolve at unprecedented speed, Visa positions itself as both a technology provider and a strategic advisor.

3. Visa’s Expanding Stablecoin Payment Infrastructure

Visa’s advisory launch coincides with rapid expansion of its stablecoin settlement network. The company has extended USDC-based settlement capabilities across Europe, the Middle East, and Africa (EMEA), significantly reducing cross-border transaction costs and settlement times.

Additionally, Visa has announced support for multiple stablecoins and blockchains, reflecting a shift away from single-asset dependency. This multi-chain, multi-asset approach aligns with enterprise requirements for resilience, liquidity access, and regulatory flexibility.

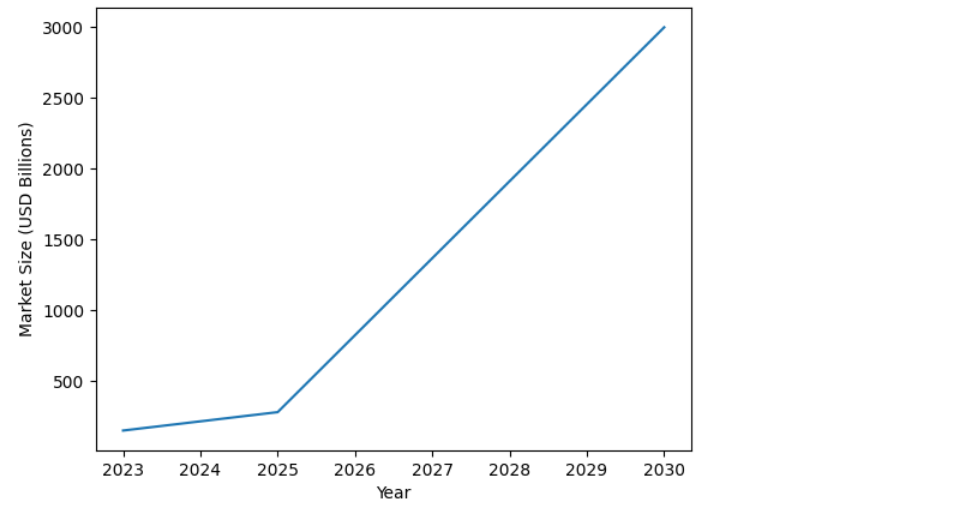

Title: Growth of the Global Stablecoin Market

This chart visualizes the expansion of stablecoin issuance from early adoption to projected institutional scale.

4. Market Growth and Institutional Adoption of Stablecoins

According to research by Citigroup, total stablecoin issuance reached approximately $280 billion in 2025. Driven by accelerating adoption and regulatory clarity, Citigroup projects issuance could reach between $1.9 trillion and $4.0 trillion by 2030.

Several factors underpin this growth:

- Regulatory clarity in major jurisdictions, particularly for fiat-backed stablecoins

- Operational demand for faster, cheaper cross-border settlement

- Integration with existing payment networks, reducing friction for enterprises

- Programmability, enabling automated compliance, treasury, and reconciliation

Stablecoins are increasingly viewed as “tokenized cash,” bridging traditional finance and blockchain-based systems rather than replacing them.

5. Why Visa’s Move Matters for the Crypto and Blockchain Industry

Visa’s entry into full-scale enterprise stablecoin support represents a validation moment for the broader blockchain ecosystem. Unlike crypto-native startups, Visa operates at global scale, under strict regulatory oversight, and with deep relationships across banks and merchants.

For enterprises, Visa’s involvement reduces perceived risk:

- Counterparty trust is strengthened by Visa’s brand and compliance standards

- Integration costs are lowered through existing Visa rails

- Regulatory alignment becomes clearer when stablecoins are embedded within traditional payment frameworks

This dynamic may accelerate adoption not only of stablecoins themselves, but also of adjacent blockchain infrastructure such as on-chain identity, compliance automation, and tokenized financial instruments.

6. Enterprise Use Cases: From Payments to Treasury Automation

Stablecoins supported by Visa and VCA are not limited to consumer payments. Key enterprise use cases include:

- Cross-border B2B settlement with near-instant finality

- Merchant settlement optimization, reducing FX and intermediary fees

- Treasury management, enabling real-time liquidity movement

- Programmable payouts, such as payroll or supplier payments

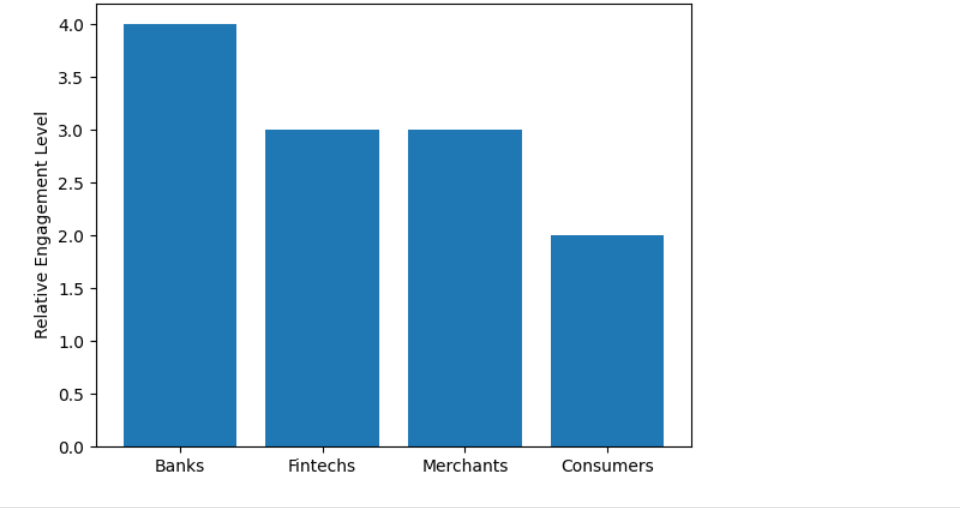

Title: Visa Stablecoin Ecosystem Participants

This diagram illustrates the relative engagement of banks, fintechs, merchants, and consumers within Visa’s stablecoin ecosystem.

7. Competitive Landscape: Visa, Banks, and Fintechs

Visa is not alone in pursuing stablecoin infrastructure. Major banks, payment processors, and fintech firms are exploring similar initiatives. However, Visa’s advantage lies in its interoperability—connecting blockchain-based settlement with existing card and payment networks.

Rather than competing directly with banks, Visa’s model positions it as an enabling layer, allowing financial institutions to innovate without rebuilding their entire payment stack.

8. Conclusion: Stablecoins as the Next Layer of Global Payments

Visa’s launch of the Stablecoin Advisory Practice marks a turning point in the evolution of stablecoins. What began as crypto-native instruments are rapidly becoming regulated, enterprise-grade financial infrastructure.

By combining advisory expertise, technical integration, and global payment reach, Visa and VCA are shaping a future where stablecoins function as programmable, borderless cash within the existing financial system.

For investors, builders, and enterprises seeking new revenue streams and operational efficiency, this shift signals that stablecoins are no longer speculative experiments—but a core component of the next generation of global finance.