Key Points :

- The U.S. Treasury and IRS issued interim guidance stating that corporations may exclude unrealized gains and losses on cryptocurrency holdings when computing adjusted financial statement income (AFSI) for the corporate alternative minimum tax (CAMT).

- This guidance offers relief to crypto-holding firms (e.g. Strategy Inc, MicroStrategy) and reduces a major tax risk that had loomed under new accounting and tax laws.

- The guidance is interim and not final — the IRS still plans to issue formal regulations.

- The change comes amid shifting accounting standards (FASB’s ASU 2023-08) requiring fair-value measurement of crypto assets, which had raised tensions between accounting and tax treatment.

- Simultaneously, Congress is holding hearings on crypto taxation, and the White House is pushing for broader reforms of digital asset tax regimes.

- For practitioners and investors, this development shifts the calculus for corporate treasury crypto strategy, but uncertainties remain about final rules, wash-sale rules, DeFi, and global coordination.

1. Background: CAMT and Crypto Tensions

In 2022, the U.S. Congress, under the Inflation Reduction Act, introduced a Corporate Alternative Minimum Tax (CAMT), which imposes a 15 % minimum tax on a corporation’s Adjusted Financial Statement Income (AFSI) for large firms (those with average financial statement income over $1 billion).

Separately, in December 2023 the Financial Accounting Standards Board (FASB) issued ASU 2023-08, which requires certain crypto assets held by entities to be measured at fair value, with changes in fair value flowing through net income each reporting period.

This accounting change meant that companies holding significant amounts of crypto—such as Bitcoin or Ethereum—must mark their holdings to market on each reporting date, even if they do not sell. Those “paper gains” now appear in net income under GAAP. Meanwhile, under prior tax practice, unrealized gains (i.e. gains on assets not yet sold) had generally not been taxed.

The tension was that under proposed CAMT regulations, firms might have to include those unrealized gains in their AFSI base and thereby incur a 15 % minimum tax on them—effectively taxing gains not yet realized. That possibility triggered strong backlash from companies (especially those heavily invested in crypto) and from industry lobbyists.

For example, Strategy Inc had publicly warned that under prior proposals, it might owe billions in CAMT from unrealized bitcoin gains.

Thus, the impending collision between accounting mark-to-market rules and tax policy created significant uncertainty for crypto-holding corporates.

2. The New Interim Guidance: What Changed

On September 30, 2025, the U.S. Treasury and IRS issued interim guidance (Notice 2025-27) clarifying that firms may exclude unrealized gains or losses on digital asset holdings when computing AFSI for CAMT purposes.

2.1 Key Provisions of Notice 2025-27

- The guidance introduces a simplified method (interim safe harbor) for determining whether a corporation is “applicable” for CAMT.

- Under this method, firms can exclude changes in unrealized gains/losses on crypto holdings from AFSI. In effect, the interim guidance ensures that such paper gains are not taxed until realized (i.e. when the crypto is sold).

- The IRS will waive penalties under Section 6655 (for underpayment of estimated tax) for CAMT liabilities for taxable years beginning after December 31, 2024, and before January 1, 2026.

- The guidance is interim: the Treasury and IRS intend to issue revised proposed regulations (and further interim guidance) that incorporate elements of the simplified method.

- Importantly, the guidance does not guarantee permanence: once final regulations are issued, treatment could change, though many believe the direction is favorable.

The upshot is that for now, the major looming threat of CAMT on unrealized crypto gains is removed, giving firms clarity and reducing a major tax overhang.

3. Immediate Market and Corporate Reactions

3.1 Strategy Inc and Other Crypto Companies

Following the guidance, Strategy Inc announced that it does not expect to incur CAMT liabilities from its unrealized Bitcoin holdings, given the ability to exclude such gains under the interim rules.

Its stock price reacted positively, and analysts hailed the change as removing a key source of uncertainty.

Other crypto-heavy corporates—like MicroStrategy—stand to benefit, as previously they risked sizable tax burdens once the CAMT regime took effect.

3.2 Analyst Views and Broader Ecosystem Effects

TD Securities analysts called the guidance a plus for both Strategy and the broader Bitcoin ecosystem, by eliminating a major cash tax uncertainty.

Industry commentators note that this change tilts the playing field in favor of companies holding crypto as a treasury asset, reinforcing the thesis of digital assets being held long-term rather than traded continuously.

Some cynics warn that since this is interim guidance, market participants must remain vigilant in case the final rules revert to a harsher posture.

3.3 Senate Hearing and Regulatory Pressure

On October 2–3, 2025, the U.S. Senate’s Finance Committee scheduled a hearing on crypto taxation, where IRS and Treasury officials are expected to defend the new guidance and take questions on the direction of crypto tax reform.

At that hearing, industry advocates are pushing for further relief: exemptions for de minimis transactions, lighter treatment for staking rewards and airdrops, and clarity on wash-sale rules applied to crypto.

Thus, the interim guidance is only part of a larger regulatory and legislative debate, and the final shape of crypto tax policy is still in flux.

4. Broader Context: Crypto Taxation and Regulatory Trends

4.1 Working Group and White House Crypto Report

The White House earlier released a comprehensive digital asset tax and regulatory report, urging parity, modernized guidance, and clarity.

That report specifically flagged the inconsistency that existing CAMT rules do not address “unrealized gains and losses on cryptocurrency” in accounting.

It pushed for updated IRS guidance, better reporting frameworks, and stepping away from forcing crypto into ill-fitting tax code buckets (e.g., treating them like traditional securities or commodities).

Notice 2025-27 can be seen as a partial execution of that vision, although the full policy architecture is yet to come.

4.2 Other Tax Issues in Crypto

While the Unrealized Gains / CAMT issue is urgent and high-profile, there remain several unresolved tax frontiers:

- Wash-Sale Rules: The current IRS position does not apply wash-sale rules (which restrict claiming a loss if you repurchase the same asset within 30 days) to digital assets.

- Airdrops & Staking Rewards: The IRS treats staking and airdrops as taxable income at the time of receipt (based on fair market value). Critics argue this penalizes holders if value declines after receipt.

- Lending and Borrowing of Crypto: Debates remain whether crypto lending should trigger gain or loss recognition. The Working Group has urged clarifications, potentially exempting actively traded crypto lending under rules analogous to securities lending.

- Classifying Crypto under Tax Law: Whether crypto is a security, commodity, or a separate new class matters for rules like safe harbors, straddles, and wash sales.

- International Taxation & Reporting (CARF / OECD): The Crypto-Asset Reporting Framework (CARF), part of OECD global tax transparency efforts, will impose new cross-border reporting obligations.

- DeFi & Broker Definitions: The classification of decentralized exchanges as “brokers” was nullified by Congress in April 2025, relieving DeFi platforms from some tax reporting burdens.

Hence, while the new interim guidance eases a major pressure point, many unresolved design questions remain.

4.3 Global and Regulatory Alignment

Given the borderless nature of crypto, U.S. tax moves influence global norms. Europe’s MiCA regime (Markets in Crypto Assets) came fully into force around end-2024, and the EU is preparing to adopt CARF by 2026.

Meanwhile, regulators in Asia, the Middle East, and other regions are actively adjusting crypto tax rules to strike a balance between encouraging innovation and preserving fairness. (If you like, I can pull together a comparative chart of global crypto tax regimes.)

Additionally, novel proposals in blockchain and tax tech—like using zero-knowledge proofs for selective tax disclosures (e.g. zkTax) or designing tax-aware CBDC systems—point to next-generation fiscal architectures.

d regulatory infrastructure.

5. Implications for Crypto Investors, Projects, and Corporations

5.1 Corporate Treasury Strategy

With the risk of CAMT on unrealized gains temporarily off the table, corporations may feel more confident holding crypto long term rather than liquidating to avoid tax. This strengthens the thesis of Bitcoin or large-cap crypto as a treasury reserve instrument.

However, because this relief is interim and subject to future regulatory changes, firms should model multiple tax scenarios.

Also, companies should monitor whether final regulations maintain this carve-out or introduce thresholds, phase-outs, or restrictions.

5.2 Impact on Capital Flows and Institutional Participation

Greater clarity and reduced tax risk may encourage more institutional capital deployment into crypto-backed corporates, funds, and projects. The “tax drag” argument for holding digital assets becomes less severe in U.S. contexts.

This may accelerate capital rotation into infrastructure, protocols, or balance-sheet crypto holdings rather than pure trading.

5.3 Considerations for Crypto Projects and Token Issuers

For crypto protocol teams, this change may modestly raise demand for tokens held or issued by public companies or sponsoring entities.

But token projects should remain mindful of compliance, tax structuring, and jurisdictional risk. The uncertainty around airdrops, staking rewards, wash rules, and classification means token economics need to be designed with tax resilience.

5.4 Risks and Caveats

- Because the guidance is interim, final rules may differ (including narrower carve-outs or limits).

- The relief only addresses unrealized gains/losses in the context of CAMT; it doesn’t resolve all crypto tax questions (e.g. wash sales, staking, lending).

- Firms must maintain excellent recordkeeping and basis tracking to ensure that when gains are realized, they can support correct tax treatment.

- Global compliance and cross-border reporting (e.g. under CARF) will still impose obligations unrelated to CAMT.

- Lawmakers or future administrations may seek to revisit or override favorable guidance, particularly if crypto tax revenue becomes politically salient.

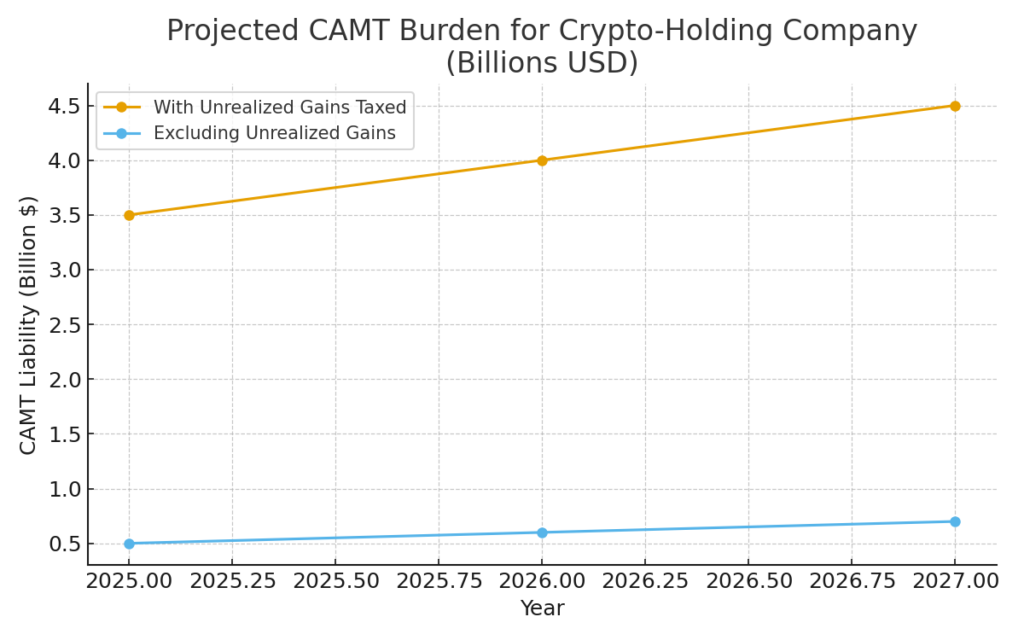

6. Graph / Chart Concept

- Line chart showing expected CAMT liability (in billions USD) for a hypothetical crypto-holding company under two scenarios: with unrealized gains taxed vs excluding unrealized gains (i.e. under the new guidance).

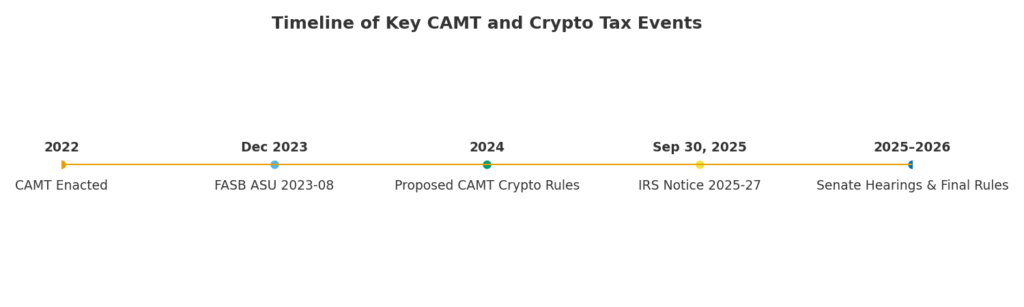

- Timeline infographic illustrating key milestones:

– 2022: CAMT enacted

– Dec 2023: FASB ASU 2023-08

– Proposed CAMT regs (pre-guidance)

– Sep 30, 2025: Notice 2025-27 issued

– Q4 2025 / 2026: Senate hearings and final rule expected

7. Conclusion

In summary, the recent interim guidance from the U.S. Treasury and IRS represents a major win for crypto-holding companies, effectively excluding unrealized gains and losses on digital assets from the AFSI base used for CAMT, thereby defusing a key tax risk. While the guidance is not yet final, it signals a pragmatic step by regulators to reconcile accounting mandates with tax fairness for crypto.

For investors, protocol teams, and corporations exploring new revenue sources or balance-sheet deployment of crypto, this relaxation shifts the risk landscape in favor of longer-term holding strategies. Nevertheless, numerous other tax and regulatory uncertainties remain—from wash-sale rules to staking and international reporting.

Over the coming months and years, the final form of crypto tax rules will be shaped by congressional hearings, stakeholder feedback, and shifting policy priorities. But for now, this development offers breathing room and clarity in a domain long plagued by tax overhang.