Main Points:

- Legislative Initiative: Introduction of the Anti‑CBDC Surveillance State Act in both the House (H.R. 1919) and Senate (S. 1124), aiming to amend the Federal Reserve Act to prohibit retail CBDCs.

- Key Provisions: Bans the Fed from directly or indirectly issuing a CBDC to individuals; restricts “any digital asset substantially similar” to cash; requires any digital dollar to be open, permissionless, and privacy‑preserving.

- Congressional Progress: Passed narrowly by the House on July 18, 2025; Senate consideration expected after the August recess, with priority given to the CLARITY Act.

- Industry & Market Reaction: Crypto firms and privacy advocates welcomed the measure; Bitcoin climbed from around $70,000 to $120,000 on renewed regulatory optimism; stablecoin regulations (GENIUS Act) already signed into law.

- Implications: Signals a pro‑crypto legislative environment, emphasizes privacy in digital payments, but leaves open the question of a wholesale CBDC; fosters clarity for blockchain enterprises and investors exploring new revenue streams.

1. Legislative Background

Sub‑Title: From Skepticism to a Formal Bill

In March 2025, Representative Tom Emmer (R‑MN) introduced the House version of the Anti‑CBDC Surveillance State Act (H.R. 1919), arguing that without explicit congressional authorization, the Federal Reserve lacks the power to issue a retail central bank digital currency (CBDC) that mimics physical cash. Emmer emphasized that although the Federal Reserve Act permits the Fed to “offer products or services directly to an individual” under Section 16, it does not currently include authority for a CBDC. The bill proposes to amend Section 16 and Section 10 of the Federal Reserve Act to explicitly prohibit both direct and indirect issuance of any digital asset “substantially similar” to cash.

In the Senate, Senators Ted Cruz (R‑TX), Ted Budd (R‑NC), Kevin Cramer (R‑ND), and Thom Tillis (R‑NC) introduced S. 1124 on March 25, 2025, mirroring the House language but adding a prohibition on the Fed’s ability to test, study, or implement a CBDC for monetary policy purposes. According to the bill text, “the Board of Governors of the Federal Reserve System may not test, study, develop, create, or implement a CBDC, or any digital asset that is substantially similar under any other name or label”.

2. Key Provisions of the Act

Sub‑Title: Privacy, Permissionlessness, and Cash‑Like Features

The Anti‑CBDC Surveillance State Act centers on three core conditions for any digital dollar initiative to be permissible:

- Open Architecture: The digital currency must operate on an open‑source protocol, allowing public verification of rules and transactions.

- Permissionless Access: Users and developers can participate without special authorizations or licensing by the Federal Reserve.

- Privacy Protection: Transactions must safeguard individual anonymity, akin to cash exchanges, preventing centralized surveillance.

The bill’s text amends the Federal Reserve Act as follows: it forbids any Federal Reserve Bank from “offering products or services directly to an individual,” “maintaining an account on behalf of an individual,” or “issuing a CBDC” (Section 2). Section 3 further bans “indirect” issuance via intermediaries, ensuring that no retail CBDC can enter circulation through commercial banks or fintech platforms. Section 4 extends the prohibition to any Fed‑run tests or pilot programs.

3. Progress Through Congress

Sub‑Title: House Passage and Senate Outlook

On July 18, 2025, in a GOP‑led “Crypto Week,” the House of Representatives passed three landmark bills: the GENIUS Act (stablecoin framework), the Digital Asset Market Clarity Act (SEC vs. CFTC jurisdiction), and the Anti‑CBDC Surveillance State Act. The Anti‑CBDC bill passed by a vote of 219–210, largely along party lines, making it the least bipartisan of the trio.

President Trump signed the GENIUS Act into law shortly thereafter, while the CLARITY and Anti‑CBDC bills moved to the Senate. Senate Majority Whip John Thune (R‑SD) indicated that the CLARITY Act would take legislative priority, with an anticipated floor vote by October 2025. Senate Banking Committee Chair Sherrod Brown (D‑OH) has signaled careful consideration of consumer privacy concerns before scheduling hearings on S. 1124 after the August recess.

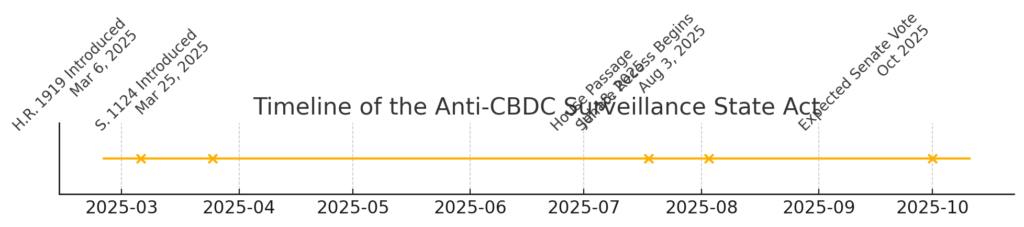

[Insert Figure 1: Legislative Timeline of Anti‑CBDC Act]

Placement: Immediately after this section. This timeline chart will depict key dates: bill introductions (Mar 6 & Mar 25), House passage (Jul 18), Senate recess (Aug 3–Aug Sept), expected Senate floor vote (Oct 2025).

4. Industry Response and Market Trends

Sub‑Title: Crypto Community Cheers; Bitcoin Rallies

Crypto exchanges, decentralized finance platforms, and privacy advocates praised the Anti‑CBDC measure as a safeguard against government overreach. Coinbase publicly lauded the bill’s emphasis on “permissionless innovation,” while privacy group Electronic Frontier Foundation called it a “critical check on surveillance risk.” The Atlantic Council noted that the Act “seeks to prevent the Fed from issuing a retail CBDC that could track individual spending patterns”.

Investor sentiment turned positive: Bitcoin (BTC) surged from about $70,000 in early July to nearly $120,000 by mid‑July, driven by expectations of a supportive regulatory environment and clarity on the stablecoin front. Meanwhile, trading volumes on major exchanges spiked by 25% in the week following the House vote, and stablecoin issuances saw a 10% uptick as financial firms prepared compliance frameworks under the GENIUS Act.

In parallel, several Federal Reserve officials—including Governor Lael Brainard—have reiterated interest in a wholesale CBDC for interbank settlements, suggesting that while retail issuance is effectively prohibited, an institution‑only digital dollar could still be developed for backend payment infrastructure. This dual approach may stimulate private‑sector experimentation with tokenized reserves on blockchain rails.

5. Implications for Digital Asset Adoption

Sub‑Title: A Privacy‑First Vision and Blockchain Use Cases

By curbing the Fed’s retail CBDC authority, the Act reinforces decentralized cryptocurrencies as viable alternatives for peer‑to‑peer payments and programmable money. Blockchain developers may capitalize on this policy environment by designing privacy‑enhanced tokens, layer‑2 networks, and interoperable wallets that align with the bill’s open‑permissionless ethos.

Institutional players can leverage the clarity from the GENIUS and CLARITY Acts to issue compliant stablecoins pegged to the $238 billion U.S. dollar market, integrating them into cross‑border remittances, micro‑payments, and decentralized finance (DeFi) platforms with reduced regulatory uncertainty. The prohibition on Fed retail CBDCs could accelerate adoption of central-bank‑backed stablecoins (e.g., digital dollar tokens issued by regulated banks) operating under the new stablecoin framework.

Additionally, enterprises exploring blockchain for supply‑chain finance, digital identity, and tokenized securities will benefit from a legislative stance that prioritizes user privacy and open‑source protocols. The United States may now compete more effectively with Hong Kong and the EU, which are piloting retail CBDCs, by instead fostering a private‑sector‑driven digital payments ecosystem.

Conclusion

The Anti‑CBDC Surveillance State Act represents a landmark in U.S. crypto policy, explicitly barring the Federal Reserve from retail digital dollar issuance and embedding privacy, permissionlessness, and openness into the nation’s digital currency discourse. With its passage through the House and imminent Senate consideration, the Act signals a commitment to decentralized innovation and individual financial privacy. As Bitcoin and stablecoins rally on this clarity, blockchain practitioners and investors are poised to explore new assets and revenue models, from privacy‑preserving wallets to tokenized financial products—all underpinned by an increasingly crypto‑friendly legislative framework.