Main Points :

- Ethereum and silver unexpectedly recorded the largest liquidations globally, surpassing both Bitcoin and gold.

- Over $292 million in leveraged positions were wiped out in just 24 hours across these two markets.

- The event reflects deep structural similarities between crypto derivatives and traditional commodity markets.

- Liquidity shifts during U.S. market hours and macroeconomic uncertainty amplified forced liquidations.

- For investors seeking new crypto assets and revenue models, the episode highlights where hidden systemic risks — and opportunities — actually lie.

1. A Rare Market Configuration: When Ethereum and Silver Lead Liquidations

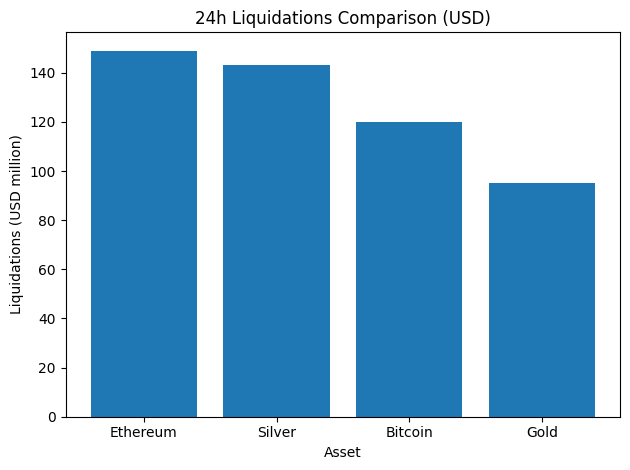

During periods of market stress, investors usually expect Bitcoin or gold to dominate headlines. However, the latest liquidation data revealed an unusual configuration: Ethereum and silver ranked first and second globally in forced liquidations over a 24-hour period.

Ethereum alone recorded approximately $149 million in liquidations, while silver followed closely with $143 million. These figures exceeded liquidation volumes in both Bitcoin and gold, marking a rare inversion of the usual risk hierarchy across asset classes.

This phenomenon occurred while markets were already experiencing heightened volatility driven by macroeconomic uncertainty, tightening financial conditions, and rapid shifts in risk appetite.

What makes this episode notable is not just the size of the liquidations, but where they occurred. Ethereum, often viewed as a technology-driven crypto asset, and silver, a centuries-old monetary metal, became the primary pressure points of leveraged speculation.

[“24h Liquidations Comparison (USD)”]

2. Ethereum: Structural Volatility Beneath a Mature Narrative

Ethereum’s liquidation surge highlights a contradiction in its market positioning. While Ethereum is often described as a “mature” crypto asset due to its institutional adoption, staking ecosystem, and role as settlement infrastructure for DeFi, its derivatives market tells a different story.

The sharp price decline triggered cascading liquidations across perpetual futures and margin positions. Compared to Bitcoin, Ethereum typically carries:

- Higher leverage ratios

- Thinner order-book depth

- Greater sensitivity to cross-asset risk-off movements

As a result, when prices move sharply, forced liquidations accelerate more rapidly than in Bitcoin markets.

Importantly, this volatility does not imply weakness in Ethereum’s long-term fundamentals. Instead, it reflects the reality that Ethereum functions simultaneously as:

- A programmable settlement layer

- A speculative growth asset

- A collateral base for DeFi leverage

This multi-role identity amplifies both opportunity and risk.

3. Silver’s Surprise: Why a Traditional Metal Imploded Like a Crypto Asset

Even more surprising than Ethereum’s liquidation dominance was silver’s behavior. Traditionally considered a defensive or industrial commodity, silver experienced liquidation volumes exceeding gold.

Several structural factors explain this:

First, silver’s futures and CFD markets are highly leveraged relative to market depth. Small price movements can therefore trigger outsized margin calls.

Second, silver occupies a hybrid role between industrial metal and monetary hedge. In times of uncertainty, this dual identity creates conflicting flows — industrial demand weakens while monetary speculation intensifies.

Third, algorithmic and macro-driven trading strategies often treat silver as a high-beta proxy for gold, meaning it absorbs volatility that gold itself avoids.

When U.S. market hours began and liquidity profiles shifted, these structural vulnerabilities were exposed, leading to rapid forced position closures.

4. Why Bitcoin and Gold Were Relatively Calm

The relative calm in Bitcoin and gold liquidation figures does not indicate a lack of volatility, but rather market maturity and liquidity resilience.

Bitcoin’s derivatives market has evolved significantly, with:

- Deeper institutional liquidity

- Better-distributed leverage

- More sophisticated risk management

Gold, meanwhile, benefits from its role as a core reserve asset, with large players typically employing lower leverage and longer time horizons.

Ironically, this stability pushed speculative pressure into adjacent markets — Ethereum and silver — where leverage was cheaper and perceived upside remained attractive.

5. Macro Triggers: Liquidity, U.S. Market Open, and Risk Repricing

The liquidation wave coincided with the opening of U.S. markets, a period often associated with sharp liquidity rebalancing. During these windows:

- Asian and European positions are reassessed

- Dollar liquidity conditions reset

- Macro hedges are recalibrated

Combined with persistent uncertainty around inflation, interest rates, and geopolitical risks, investors rapidly reduced leveraged exposure.

This was not a single-asset event, but rather a synchronized deleveraging across correlated markets.

6. Implications for Crypto Investors and Builders

For readers seeking new crypto assets, revenue opportunities, or practical blockchain use cases, the key lesson is not fear — but structural awareness.

Ethereum’s volatility underscores its importance as a financial infrastructure asset rather than merely a token. Silver’s behavior reveals how traditional markets increasingly resemble crypto in structure.

Opportunities emerge where volatility intersects with utility:

- Risk management tooling

- On-chain derivatives infrastructure

- Cross-asset collateral systems

- Real-time liquidation analytics

The boundary between “traditional finance” and “crypto” continues to dissolve.

7. Conclusion: A Market Signal Worth Understanding

This episode of massive liquidations in Ethereum and silver is not an anomaly to be dismissed. It is a signal.

It signals that leverage has migrated away from headline assets into structurally fragile markets. It signals that crypto and traditional assets are now part of the same liquidity ecosystem. And it signals that future opportunities will favor those who understand market plumbing, not just narratives.

For investors and builders alike, the question is no longer whether markets are connected — but where the next stress point will emerge.