Key Points :

- The USDe “depeg” on Binance (to ~$0.65) was localized to Binance’s internal pricing system, not a systemic collapse of Ethena’s protocol.

- Ethena asserts that minting/redemption functionality remained intact, and $2 billion in USDe was redeemed across platforms within 24 hours with minimal deviation (≤30 bps) on non-Binance venues.

- Binance’s use of its own orderbook-based oracle (rather than broader market data) created a vulnerability: under extreme volatility and shallow liquidity, the internal price feed became distorted.

- Traders propose a coordinated attack exploiting Binance’s “Unified Account” system and the timing window before its announced oracle transition.

- The crash induced large forced liquidations, amplifying contagion across crypto markets and triggering cascading losses (~$19–20 billion) in 24 hours.

- Binance responded with compensation (~$283 million) and pledged to shift to external oracle pricing.

- The event underscores broader risks in synthetic stablecoins, exchange oracle design, and systemic fragilities in CeFi/DeFi cross-interaction.

- In the wake of the incident, academic proposals on oracle-robust designs (e.g. SecPLF, dynamic truth discovery, depeg detection) gain renewed relevance.

1. Background: What Is USDe and What Happened

USDe is a synthetic, yield‐bearing “stable dollar” developed by Ethena Labs. Unlike classic fiat-backed stablecoins (e.g. USDC, USDT), USDe is overcollateralized with crypto and maintains stability via delta-neutral hedging and yield strategies rather than direct fiat reserves.

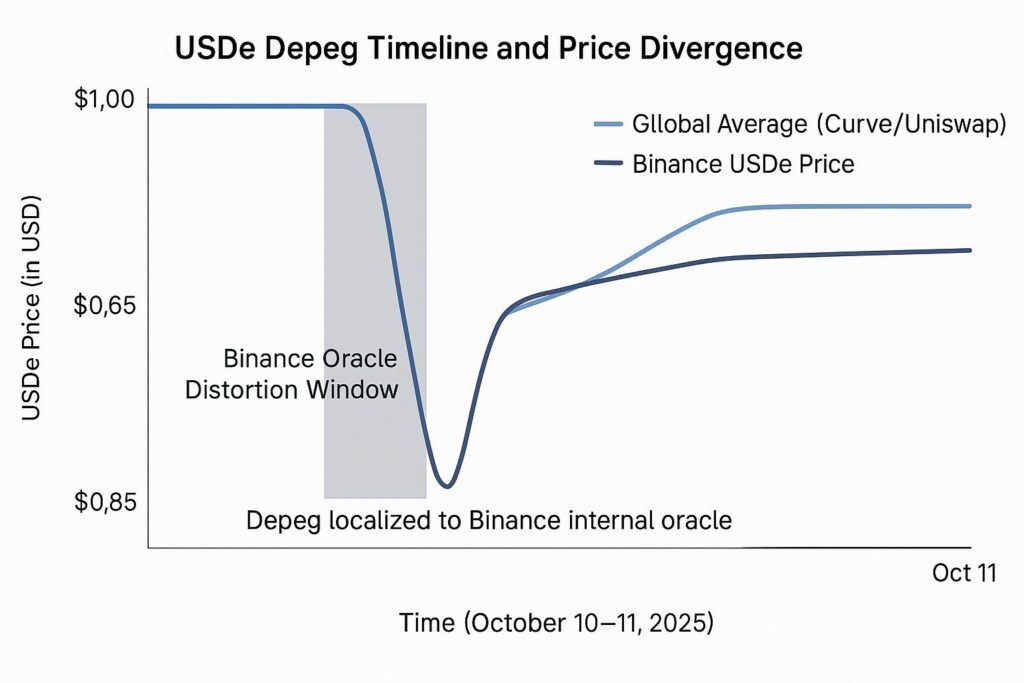

On October 10–11, during a severe market crash, USDe’s quoted price on Binance plunged to ~$0.65 before recovering. The crypto markets experienced one of the largest ever liquidation waves (~$19–20 billion in positions closed) in 24 hours.

At first glance, the incident looked like a “depeg”—i.e. loss of the $1 peg. But deeper investigation suggests the deviation was localized to Binance’s infrastructure, not intrinsic failure of USDe globally.

2. Binance’s Oracle Design Flaw: The Root Vulnerability

2.1 Internal Orderbook Oracle vs. External Aggregated Feeds

Guy Young, founder of Ethena, attributed the depeg to Binance’s reliance on its internal orderbook-based price feed (rather than referencing deeper liquidity sources or external oracles). In volatile conditions, the illiquid Binance orderbook was distorted, leading to mispricing of USDe far from its valuation on other exchanges.

He emphasized that minting and redemption of USDe remained operational during the crash, and that ~ $2 billion of USDe was redeemed across multiple venues (Curve, Fluid, Uniswap) within 24 hours, with price deviations of ≤30 basis points on those non-Binance venues.

Because Ethena’s protocol itself remained sound, the pricing discrepancy was not due to collateral failure or arbitrage breakdown across all venues—but rather an oracle weakness isolated to Binance.

2.2 Unified Account System & Amplification of Liquidations

Binance’s Unified Account structure allows multiple assets (including USDe, wrapped staking tokens like wBETH or BNSOL) to be used as collateral across margin and futures positions. The pricing of these assets for liquidation is tied to Binance’s internal price feed.

In the crash, the distorted internal pricing sharply depressed the valuation of those collateral assets, triggering forced liquidations. Because the price feed was used to calculate margin thresholds, the devaluation of USDe and other tokens cascaded into broader collateral shortfalls and massive “auto‐unwinds.”

2.3 Timing and Attack Window

Importantly, Binance had announced a plan to switch to external oracle pricing by October 14, indicating it was aware of the vulnerability.

The USDe plunge happened on October 10—right in the window where the old system was still active but flagged for transition. This timing has fueled speculation that attackers exploited the vulnerability before the upgrade took effect.

3. Coordinated Attack vs. Market Stress

3.1 Hypothesis: Deliberate Exploitation

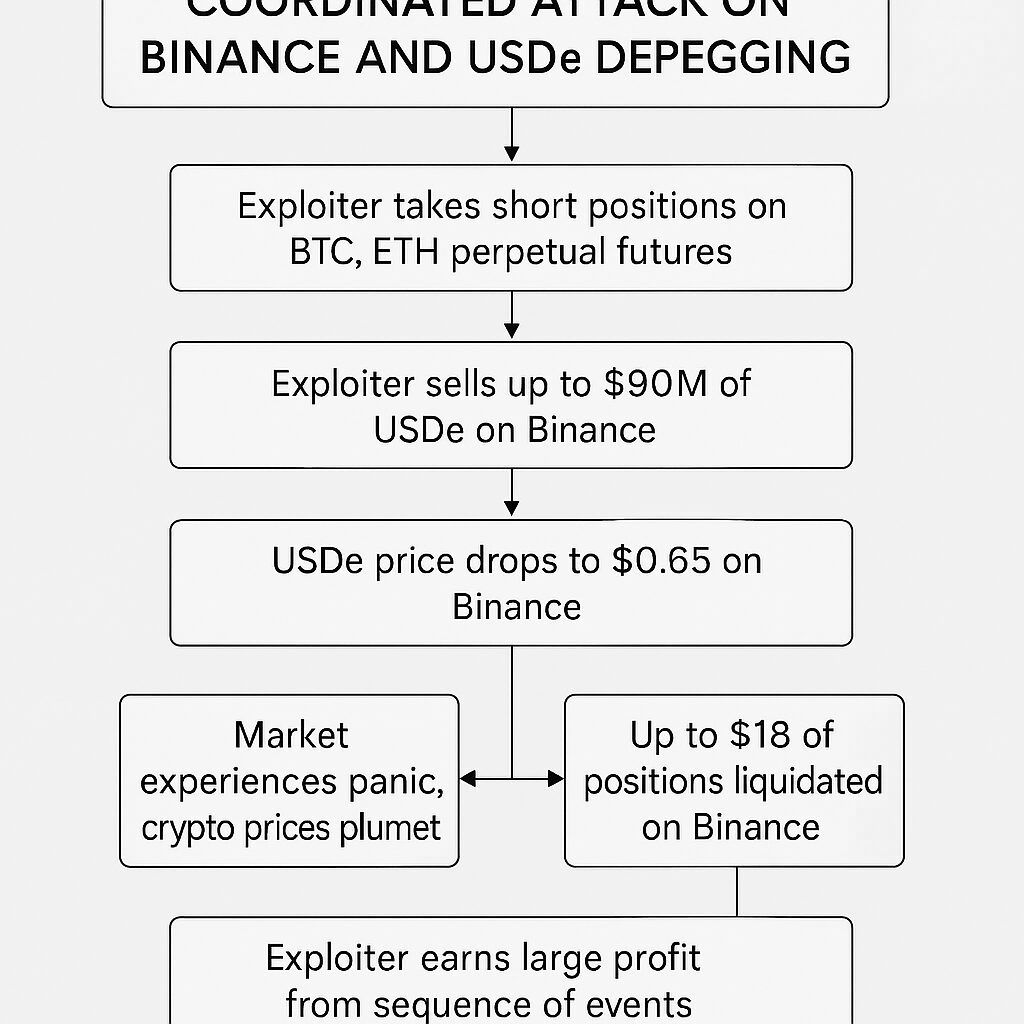

Some traders (e.g. ElonTrades) argue this was not merely a breakdown but a coordinated attack. The speculative narrative:

- Attackers sold $60–90 million of USDe on Binance, forcing its internal price down to ~$0.65, despite it trading near $1 elsewhere.

- The depressed price triggered mass liquidations (estimated up to $1 billion) on Binance via the Unified Account system.

- Simultaneously, the attackers opened shorts on Bitcoin (BTC) and Ether (ETH) in the Hyperliquid DEX perpetual markets just minutes before a tariff news headline. That news incited a broader crypto panic, magnifying contagion.

- Net profit from the shorts is estimated at ~$192 million.

- The chain reaction culminated in ~$19–20 billion of leverage liquidations across the crypto ecosystem.

This version portrays the crash as “Luna 2.0”—a systemic exploit, not mere market volatility.

3.2 Alternative View: Volatility + Design Fault

Other analyses take a more conservative stance: the depeg was not an orchestrated attack, but rather a manifestation of structural fragility meeting market stress. Key points:

- The broader macro trigger—U.S. tariff announcement—led to cross-asset risk-off and massive deleveraging. The external shock initiated price moves.

- Binance’s internal oracle and margin mechanics exacerbated the move by amplifying volatility through forced liquidations.

- The fact that USDe held peg elsewhere indicates the “depeg” was not systemic but confined to the flawed exchange pricing context.

- Some argue the timing alignment (before oracle switch) was coincidental, not proof of malicious intent.

In sum, while design flaws were real, the line between “coordinated attack” and “market stress exploitation” is blurred. The truth likely lies somewhere in between.

4. Broader Implications & Systemic Lessons

4.1 Fragility of Synthetic Stablecoins & Oracle Risk

This incident spotlights a key tension in synthetic stablecoin models: they depend heavily on precise and resilient oracle systems. When oracles misprice assets, the consequences can cascade. The USDe crash is a live stress test of those dynamics.

In response, academic research is pushing forward:

- SecPLF: A design that imposes temporal constraints on oracle updates to resist manipulation in loanable fund settings.

- Dynamic Truth Discovery Methods: Approaches that dynamically adjust credibility of data sources in high-value oracle tasks, limiting manipulation impact.

- Detecting Depegs Algorithms: Bayesian or change-point detection models that alert liquidity providers to impending depegs in Curve pools.

- AiRacleX: An LLM-driven framework to detect oracle manipulations by mining domain knowledge and generating structured detection prompts.

These lines of research become increasingly relevant as synthetic and algorithmic assets grow.

4.2 Exchange Infrastructure & Cross-Venue Risk

The USDe event underscores that exchanges are not neutral plumbing—they are active agents in price formation and risk propagation. Centralized exchanges that rely on internal oracles, isolated liquidity, or monolithic collateral systems can amplify systemic fragility.

It also shows how DeFi protocols and CeFi exchanges interact: DeFi platforms continued normal USDe operations, essentially “ignoring” the Binance distortion because they referenced robust on-chain liquidity or fixed pegs. That contrast highlights the importance of cross-venue integrity and liquidity connectivity.

4.3 Regulatory & Market Governance Pressure

Following the shock, Binance announced a $283 million compensation plan for affected users and committed to reworking its oracle logic.

But beyond one exchange, this may raise questions from regulators, auditors, and institutional participants about systemic risk controls, oracle transparency, and accountability in the world of algorithmic assets.

4.4 Strategic Takeaways for Liquidity Providers & Traders

- Never assume a depeg on one venue reflects global reality—check across venues.

- Watch for protocol or exchange transitions (e.g. oracle migrations).

- Be cautious with collateral assets that rely on internal pricing structures.

- Use detection models or alerts for early signs of depeg or price divergence. (E.g. change-point detection)

- Understand how margin/unified systems may create feedback loops in distress.

5. Recent Developments & Reinforcing Evidence

Since the original article:

- Analyses confirm that the USDe depeg was isolated to Binance while Curve and other venues showed stable pricing.

- Uphold’s research head, Dr. Martin Hiesboeck, labeled the crash a likely targeted exploit on Binance’s margin system, calling it potentially a “Luna 2.”

- News outlets place the total crypto market loss ~ $19–20 billion, confirming the scale of the contagion.

- Commentators like Miles Deutscher traced the crash to oracle disruptions, thin liquidity post-US session, and headline timing manipulation.

These developments generally support the narrative of exchange pricing failure amplified by leveraged structures and potentially opportunistic exploitation.

Conclusion

The USDe “depeg” incident marks a defining moment in the evolution of synthetic stablecoins and crypto infrastructure risk. Far from a collapse of Ethena’s model, the event more likely reflects a fragility in exchange-level oracle design — exacerbated by volatility, leveraged collateral mechanics, and a narrow time window between system announcement and implementation.

For those seeking new crypto opportunities or building blockchain-based finance systems, the lessons are stark:

- Oracle design integrity is mission-critical—the “last mile” of price inputs can make or break stability.

- Exchange-level systems (especially collateral, margin, and pricing logics) must be stress-tested—the ripple effects transcend a single token.

- Cross-venue liquidity and arbitrage paths are vital—localized distortions become systemic risks when arbitrage fails.

- Proactive detection and defense (oracle anomaly detection, dynamic truth aggregation) must be baked in, not bolted on.

Looking ahead, a combination of robust oracle frameworks, cross-venue liquidity architectures, and rigorous stress testing may define which synthetic stablecoin and DeFi designs survive future market shocks. This event is a case study for how innovation and fragility coexist—and how careful design, transparency, and risk governance will differentiate winners in the next chapter of crypto finance.