Main Points :

- Pakistan is considering a rupee-backed stablecoin alongside a central bank digital currency (CBDC) to enhance financial inclusion and modernise payments.

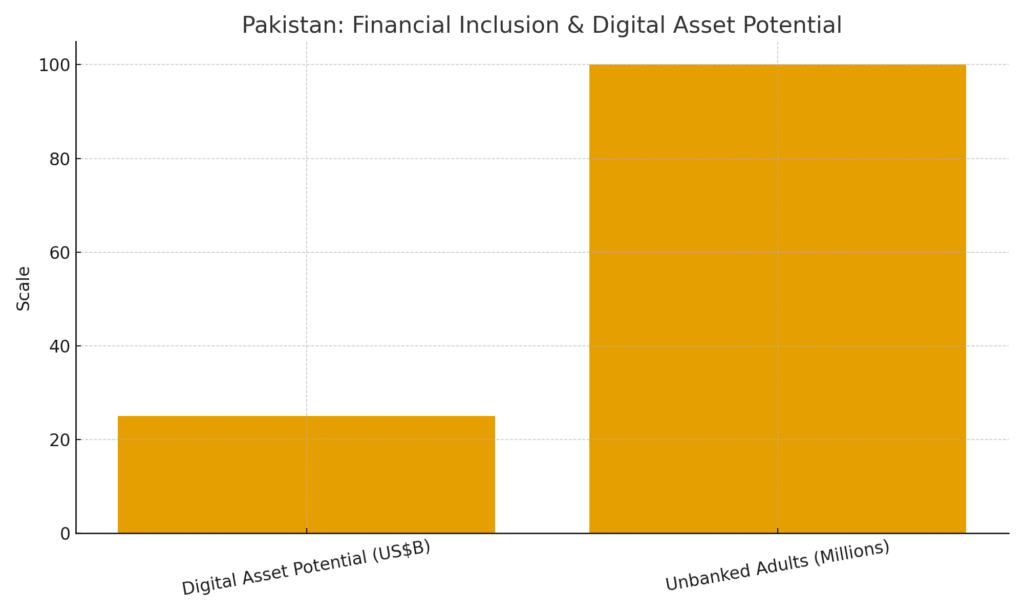

- The country has an estimated 100 million+ unbanked adults, and digital asset markets around US$20-25 billion growth potential are cited.

- The State Bank of Pakistan (SBP), with support from the International Monetary Fund (IMF) and World Bank, is piloting a CBDC prototype while regulatory frameworks are being developed.

- Private fintech involvement, e.g., ZAR raising US$12.9m to launch a dollar-backed stablecoin for Pakistani users, highlights active market innovation.

- For crypto-asset investors and ecosystem builders, Pakistan’s positioning as a ranked high adopter of crypto assets (third globally) underscores a potentially fertile environment for new digital-asset use cases.

1. The Inclusion Imperative: Why Pakistan Needs Digital Finance

Pakistan’s financial ecosystem continues to face significant access gaps. The latest figures suggest that over 100 million adults in Pakistan remain unbanked, meaning they lack access to formal banking services. This large unbanked population represents both a social challenge and an opportunity for digital finance.

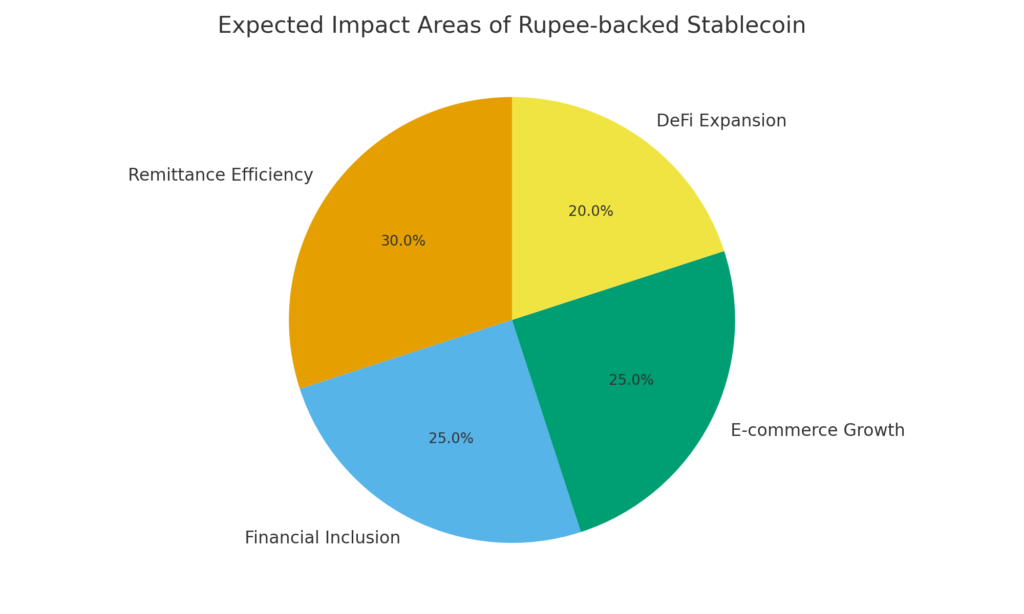

By introducing a rupee-backed stablecoin and a CBDC, Pakistan’s authorities aim to reduce the reliance on cash, lower transaction and remittance costs, and bring financial services to the under-served. A stablecoin denominated in the Pakistani rupee could enable users to send, receive and store value in digital form using mobile wallets or similar fintech interfaces—even without holding a traditional bank account. It is in this context that the SBP and banking sector in Pakistan are advancing digital payments infrastructures and considering the role of both public and private digital-asset tools.

From a blockchain practitioner’s perspective, this scenario is rich in implications: stablecoins issued or supported by a currency like the Pakistani rupee bring new rails for payments, expand the user-base of digital assets, and create infrastructure opportunities (wallets, KYC/AML flows, remittance networks) that align with real-world utility.

In short: the inclusion drive is the backdrop. For a reader hunting new crypto-asset opportunities, the development of a local stable-coin and CBDC in Pakistan gives signals of both infrastructure expansion and user-adoption potential.

2. Rupee-Backed Stablecoin: Mechanism and Strategic Significance

The proposal to issue a stablecoin backed by the Pakistani rupee—rather than a foreign currency like USD—marks a strategic shift. The benefits are multifold: first, value stability relative to the domestic currency; second, facilitation of cross-border remittances denominated in rupees; third, an on-chain instrument that mirrors the domestic unit of account and potentially avoids some conversion frictions. According to industry commentary, the Pakistani banking sector estimates that the country could unlock US$20–25 billion in digital-asset related growth.

From a design and implementation viewpoint, a rupee-backed stablecoin must address: reserve backing or collateral mechanisms, regulatory compliance (especially around issuance and redemption), technological infrastructure (on-chain ledger, wallet and custody flows), and interoperability with legacy systems (banks, remittances). For the project of building a wallet, fintech platform or service layer in Pakistan, these elements point to meaningful growth potential.

The stablecoin also serves as an on-ramp to other blockchain-based services: once wallets hold a stablecoin tied to rupees, it becomes easier to integrate lending, staking, tokenised assets, payments in e-commerce, and cross-border transfers—all of which may open secondary revenue streams. For a token-builder or wallet-developer, such a stablecoin ecosystem can become a gateway into a broader DeFi or payments infrastructure.

3. CBDC and the Regulatory Framework: Public Infrastructure in Motion

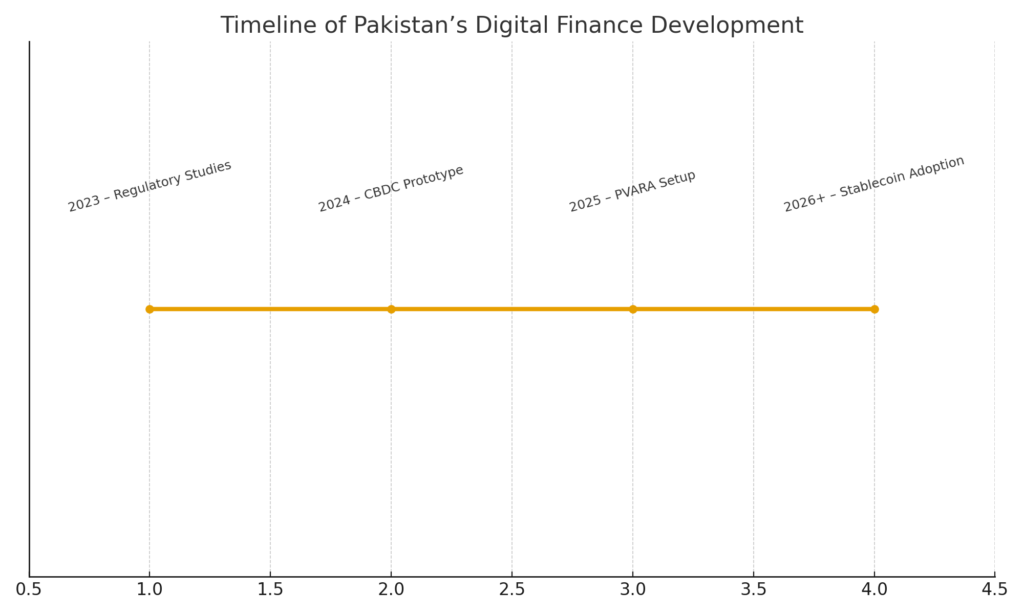

In parallel with the private stablecoin discussions, the State Bank of Pakistan is advancing development of a CBDC prototype. Faisal Mazhar, Deputy Director of Payments at the SBP, confirmed that the prototype is being developed with World Bank and IMF assistance, and that a pilot trial is planned.

Legally, Pakistan has introduced the Pakistan Virtual Assets Regulatory Authority (PVARA) under the Virtual Assets Ordinance 2025 to supervise virtual asset service providers (VASPs) and issue licences.

From the viewpoint of blockchain-based projects, a CBDC rollout signals maturation of the national payments infrastructure—likely leading to standards (digital identity, KYC/AML flows, ledger access, interoperability) that private sector platforms must adhere to. For wallet providers, stablecoin issuers or blockchain-based payments solutions, understanding this evolving regulatory architecture is critical. If the CBDC and stablecoin infrastructure are built in a compatible way, ecosystems that plug into these rails may benefit from early-mover advantages.

Moreover, the government’s focus on remittances and cost reduction means incentives may be aligned for digital-asset enabled flows (especially cross-border). For projects that facilitate inward remittances to Pakistan via blockchain, this regulatory shift is a red-flag opportunity.

4. Private Sector Innovation: Fintech, Stablecoin Startups, and Market Readiness

The involvement of private firms amplifies the signal. For example, ZAR (a fintech startup) raised US$12.9 million in a funding round led by top tier crypto investors such as Andreessen Horowitz (a16z), Dragonfly Capital, Coinbase Ventures and others. Their aim: deliver a dollar-backed stablecoin to Pakistani users and thus bridge the unbanked gap.

This private sector momentum matters for several reasons: it lowers the time-to-market for stablecoin adoption, suggests venture-capital appetite in the region, and indicates that infrastructure (wallets, KYC, user-interface) is already forming. For blockchain developers or token issuers, this indicates a fertile environment for collaboration or deployment in Pakistan. Rather than starting from scratch, the infrastructure components (wallet apps, remittance flows, local fiat-on ramps) are beginning to emerge.

It also signals that Pakistan is not just “regulation talk” but sees real market opportunity: the combination of inclusion needs, remittance flows, large unbanked population, and an entrepreneurial fintech ecosystem creates a favourable setting for digital-asset adoption.

5. Opportunity for Investors and Builders: What This Means for New Crypto Assets and Applications

For your audience—those seeking new crypto assets, income streams, and practical blockchain use-cases—the Pakistan scenario offers several lines of opportunity:

- Stablecoin-related services and infrastructure: With a rupee-backed stablecoin in view, there is opportunity for wallets, remittance-apps, merchant payments, and tokenised services denominated in the stablecoin.

- Remittances to Pakistan: Given the focus on lowering cross-border cost, blockchain platforms that enable inbound remittance flows into the stablecoin or CBDC rails could capture value.

- DeFi and tokenised assets built on local rails: Once the tokens circulate in a regulated framework, additional services such as lending, savings, collateralised loans, and localised DeFi can follow—particularly aimed at the under-banked.

- Partnerships with regulatory-approved frameworks: Projects that engage early with PVARA licensing, or build in compliance with SBP protocols, may establish strategic advantages.

- Regional spill-over potential: If Pakistan becomes a model for digital-asset adoption in South Asia, neighbouring markets may follow—giving first-mover advantage to platforms already operating in Pakistan.

The ranking of Pakistan as the third highest country in the global crypto adoption index underscores the momentum. For an asset-seeker, connecting your project or token to a high-adoption jurisdiction with fresh regulatory and infrastructure momentum can enhance both technology-reach and market potential.

6. Risks and Considerations: What Could Go Wrong?

While the opportunity is attractive, there are several risk vectors:

- Regulatory ambiguity or delay: Although frameworks are being drafted, full legal clarity is not yet in place. Delays could obstruct deployment or invite uncertainties.

- Technical and infrastructural readiness: Launching a CBDC or stablecoin entails high-demand infrastructure: scalability, security, interoperability with legacy banking and fintech systems. Any mis-step could delay impact.

- Adoption barriers: Even with high crypto-adoption rankings, converting that to stablecoin usage or wallet uptake requires strong user experience, trust, local merchant acceptance, and regulatory clarity.

- Currency risk and macro conditions: Since the stablecoin is rupee-backed, macro-economic risks (rupee devaluation, inflation, monetary instability) could affect confidence in the stable-value promise.

- Competition and cannibalisation: If private stablecoins, foreign currency stablecoins, or parallel systems proliferate, fragmentation may limit scale or regulatory favourability.

- Exit or monetisation model: For any project in this ecosystem, monetising wallet usage, remittance flows, or DeFi services in a low-income market may require creative business models and localisation.

For developers and investors, the need is to balance the early-mover advantage with robust risk-mitigation strategy: define compliance pathways, align with regulators, build local partnerships, and adopt a flexible architecture.

7. Roadmap: What to Watch and When to Act

If you are tracking Pakistan as a blockchain-asset or platform opportunity, here is a suggested timeline of milestones:

- Short-term (0-6 months): Watch for official announcements from the SBP on the rupee-stablecoin issuance framework, pilot results of the CBDC prototype, and licensing rounds from PVARA for VASPs.

- Mid-term (6-18 months): Expect rollout of pilot wallet/stablecoin services, partnerships between fintech firms and local banks/merchants, and initial remittance integrations. Adoption metrics (number of wallets, transaction volume) will be key signals.

- Long-term (18 + months): Potential large-scale adoption, expansion of tokenised financial products built on stablecoin rails, cross-border flows into regional markets, and increasing orthogonal DeFi innovation in Pakistan.

- Trigger points for action:

- Licensing approvals for private stablecoin issuers in Pakistan.

- Merchant-acceptance programmes for stablecoin payments.

- Partnerships between international blockchain firms and Pakistani fintech entities.

- Official data on wallet usage, remittance cost reductions, or transaction volume growth.

For wallet-builders, token issuers or remittance platforms, aligning launch or go-to-market strategy around these milestone windows may yield strategic advantage.

8. Conclusion: Bridging the Two Extremes of Finance via Pakistan’s Digital Leap

In the context of your “Two-Extremes Model” (Asset-Backed Representation versus Autonomous Trust Tender), Pakistan’s nascent digital finance initiative embodies a convergence of both extremes:

- The rupee-backed stablecoin is an example of Asset-Backed Representation — a tokenisation of a national currency, linking traditional fiat to blockchain rails, providing value anchoring and regulatory backing.

- The emerging CBDC and stablecoin ecosystem also opens the door to Autonomous Trust Tender — decentralised and digital-first financial access for previously unbanked populations, remittance flows, and blockchain-native applications.

For practitioners building wallets, swaps, remittance flows, or DeFi platforms, Pakistan offers a live test-bed: a large unbanked market, regulatory signals moving forward, and public-private collaboration actively forming. The stablecoin and CBDC rails could become foundational infrastructure on which novel use-cases are built—whether it is wallet to wallet transfers, tokenised savings, remittance pipelines, or blockchain-enabled merchant payments.

Ultimately, the question becomes: will Pakistan move quickly enough to capture its estimated US$20-25 billion digital-asset growth opportunity before regulatory or infrastructural delays set in? For builders and investors, the answer hinges on timing, regulatory alignment, and technology execution.

As you explore new crypto assets and blockchain use-cases, keeping an eye on Pakistan may yield early-mover advantages—not just for standalone tokens, but for platforms that enable stablecoin rails, wallet adoption and cross-border value flows in a major emerging economy.