Main Points :

- A new U.S. House bill would codify Trump’s executive order to allow crypto and private equity investments in 401(k) retirement plans

- The proposed legislation would make the policy permanent rather than relying on an executive order

- This shift follows prior changes: removal of restrictive guidance by the U.S. Department of Labor

- The potential inflow from 401(k) accounts—now totaling over $9 trillion—could channel significant capital into digital assets

- Risks include volatility, fiduciary liabilities, regulatory uncertainty, and investor protection challenges

- For crypto and blockchain professionals, this could open institutional pipelines, new product opportunities, and demand for compliance infrastructure

1. Background: From Executive Order to Legislative Proposal

In August 2025, former President Donald Trump signed an executive order titled “Democratizing Access to Alternative Assets for 401(k) Investors”, directing federal agencies to reexamine restrictions and open the door for alternative assets—such as private equity, real estate, commodities, infrastructure, and digital assets—to be included in 401(k) plans. The order mandates the Department of Labor, the SEC, and the Treasury to issue guidance, propose rules, and calibrate fiduciary safe harbors within 180 days.

However, executive orders do not carry the permanence of legislation. Recognizing this, Representative Troy Downing introduced a bill in the U.S. House of Representatives to codify (i.e. turn into law) Trump’s executive order. The bill has been submitted to the House Financial Services Committee.

Supporters argue that this legislation would give 401(k) investors permanent access to a broader universe of assets under recognized legal frameworks. Critics caution about risk, complexity, and responsibility for plan fiduciaries.

2. Why Now? Policy Shifts and Momentum

This proposed law did not arise from a vacuum. Several developments set the stage:

- DOL Guidance Repealed: In May 2025, the U.S. Department of Labor formally withdrew a 2022 compliance guidance that had strongly discouraged inclusion of crypto in 401(k) menus. That guidance had warned fiduciaries that offering crypto could be considered imprudent.

- Alternative Asset Lobbying: Private capital firms like Blackstone, Apollo, and BlackRock have long sought access to retirement funds as a capital source. The change enables them to tap into the multi-trillion dollar defined contribution market.

- Crypto Legitimization Trend: Institutional acceptance of crypto is rising. Morgan Stanley, for example, announced earlier this month that it will allow all clients—not just ultra-high-net-worth ones—to allocate portions of their portfolios to digital assets.

- Seizures & Reserves: Meanwhile, U.S. government bitcoin holdings surged to $36 billion after a record DOJ seizure, fueling press around the government’s role in digital assets.

Thus, the legislative push is part of a broader reorientation in U.S. policy—from cautious restriction toward optional openness.

3. What the Proposed Bill Does (and Doesn’t Do)

If passed, the bill would convert Trump’s Executive Order 14330 into statutory law. Key features:

- It would require that 401(k) plans be allowed to offer alternative assets (including digital assets) when deemed appropriate by fiduciaries.

- It does not mandate all 401(k) plans to include crypto; fiduciaries retain discretion based on duty of care and participant best interest.

- It directs federal agencies to issue rules, regulations, and safe harbor mechanisms to reduce litigation risk and clarify fiduciary duties under ERISA (Employee Retirement Income Security Act).

In short, this is an enabling law, not a compulsory mandate.

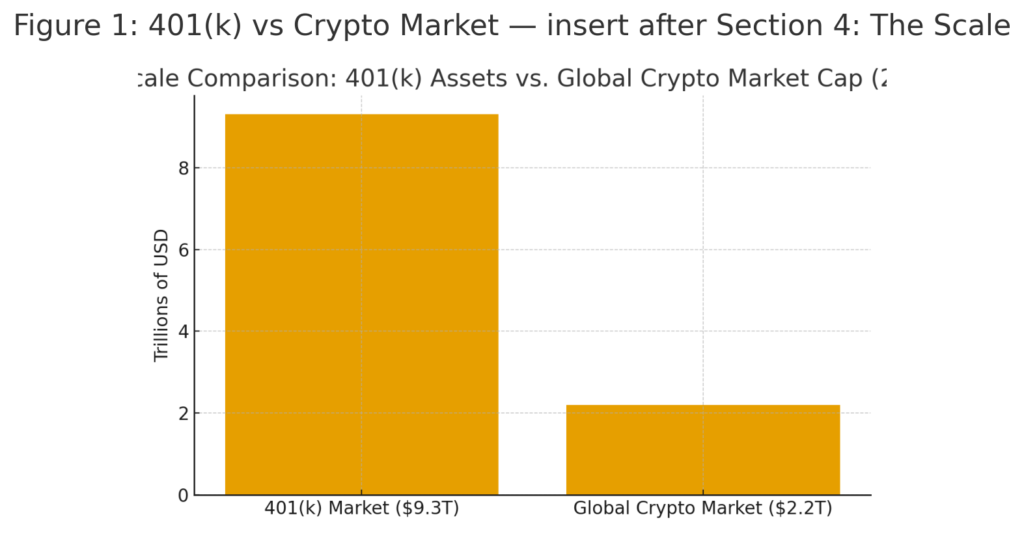

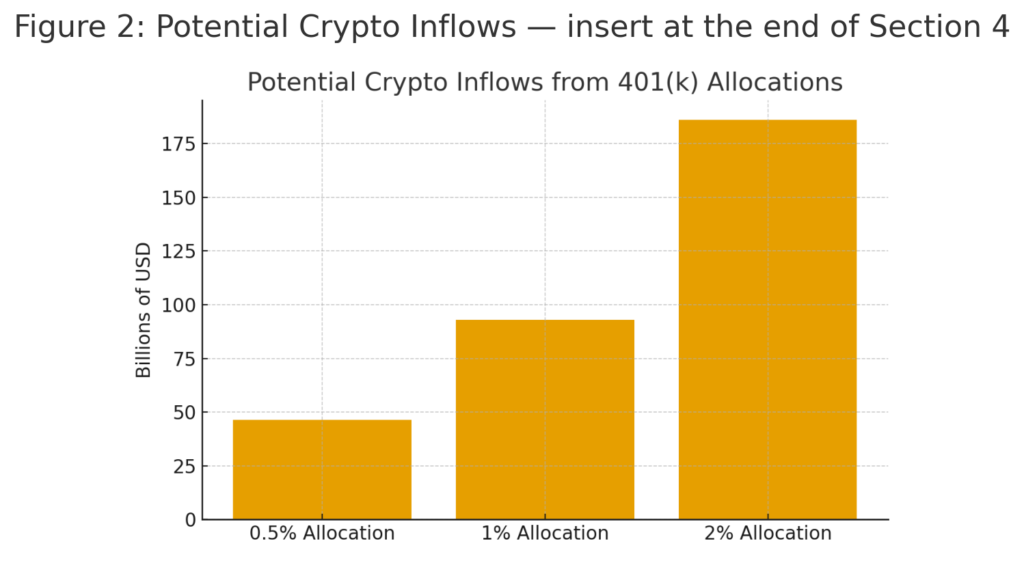

4. The Scale: $9 Trillion in 401(k) Assets and Potential Crypto Flows

As of mid-2025, Americans hold approximately $9.3 trillion in 401(k) retirement accounts. Even if a modest percentage of this sum were allocated to digital assets, that could mean tens to hundreds of billions of dollars flowing into the crypto space.

Analysts see this as a potential watershed moment for crypto adoption. André Dragosch, head of European research at Bitwise, remarked that opening retirement accounts to crypto could unleash billions in new capital to digital assets.

The size of the 401(k) market gives it leverage: even a 1% allocation shift would translate to $93 billion. That is the kind of scale that can dramatically influence liquidity, market depth, and product demand.

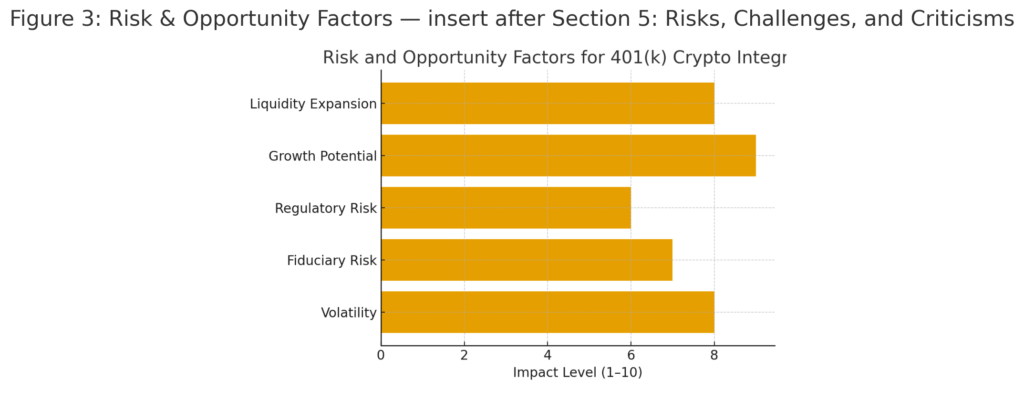

5. Risks, Challenges, and Criticisms

While the opportunity is alluring, the shift is laden with complexity and risk.

Volatility & Illiquidity

Cryptocurrencies are known for extreme price swings. For ordinary retirement investors, sudden drawdowns could be damaging. Illiquid private markets (especially private equity or some crypto funds) may conflict with the expectations of liquidity in retirement accounts.

Fiduciary Liability

Even with safe harbors, fiduciaries may face lawsuits if allocations underperform. Determining what is in participants’ interest is far more complex when digital assets are involved. This is especially acute in defined contribution plans where participants choose allocations.

Regulatory & Legal Uncertainty

Though the bill aims to clarify regulation, much remains undefined: which crypto products qualify, custody rules, taxation, disclosure, and qualified custodians. How the SEC, CFTC, IRS, and state regulators interact will matter greatly.

Investor Protection & Education

Many 401(k) participants may lack understanding of crypto. Without robust disclosures, there is risk of mis-selling or participants making inappropriate allocations.

Market Disruption & Systemic Risk

Large flows into crypto could amplify price swings, increase correlation with traditional markets, and raise concerns about systemic impacts. Critics warn that opening retirement accounts to crypto could be akin to embedding speculation in mainstream portfolios.

6. Implications for Blockchain & Crypto Industry

This development would catalyze a new axis of opportunity.

Product Innovation & Retirement-Focused Crypto Funds

We can expect the rise of crypto ETFs or managed vehicles specially tailored for retirement accounts, with compliance, fiduciary oversight, and diversified baskets. Custodial infrastructure, audit, risk tools, and compliance layers will be in high demand.

Institutional & Capital Inflows

Greater legitimacy may attract traditional asset managers and institutional capital into crypto firms, bridging the gap between DeFi projects and traditional finance (TradFi).

Compliance, Governance & Reporting Services

Firms specializing in regulatory compliance, onchain audits, custodial proof-of-reserves, and KYC/AML infrastructure will benefit, especially as retirement flows demand auditability and transparency.

Ecosystem Expansion

Broader adoption by mainstream investors may hasten development of blockchain bridges, liquidity, interchain composability, and stable infrastructure to support large fiat-crypto interactions.

7. Comparisons & Global Context

The U.S. is not alone in exploring retirement-crypto integration. Some jurisdictions allow pension funds partial allocations to alternative assets, including crypto, under strict rules. In contrast, others remain cautious, citing risk.

Morgan Stanley’s recent decision to open crypto access to all clients (not just high-net-worth ones) signals the growing overlap between retail, advisory, and institutional adoption.

This move also complements Trump’s earlier 2025 executive order to establish a Strategic Bitcoin Reserve, leveraging seized government holdings as national digital reserves.

8. What Entrepreneurs, Developers & Investors Should Watch

- Legislative progress: Which U.S. Senate committees and amendments emerge

- Fiduciary rule proposals: How safe harbors define allowable crypto exposure

- Custody & auditing standards: Demand for third-party verifiable custody grows

- Product launches: Expect crypto retirement ETFs, multi-asset alternatives, and turnkey 401(k) wrappers

- Education & robo-advisors: Tools to help participants navigate digital asset allocations

- Litigation trends: Early lawsuits may shape the practical limits of fiduciary exposure

Conclusion

The proposed bill to enshrine crypto and private equity access in 401(k) plans represents a potentially paradigm-shifting move in how Americans save for retirement—and how capital flows into the crypto economy. By converting Trump’s executive order into law, it seeks to offer permanence, clarify fiduciary responsibilities, and open up trillions in retirement assets to alternative investments.

Yet the move is far from risk-free. Volatility, legal uncertainty, and fiduciary obligations demand careful rulemaking, oversight, and participant protection. For those in the blockchain and crypto field, this moment presents a rare opening: to build the infrastructure, products, and compliance frameworks that bridge institutional capital with decentralized technology. If executed prudently, this could mark the beginning of retirement-grade crypto allocation—and a new frontier of adoption and scale in digital asset markets.