Main Points:

- CARF Launch: The UK will implement the Cryptoasset Reporting Framework (CARF) on January 1, 2026, mandating KYC and transaction reporting for crypto users and service providers.

- Mandatory Data Collection: Exchanges, wallets, and NFT marketplaces must collect real-name, date-of-birth, address, residency and tax ID details from every user.

- Penalties: Failure to comply carries fines up to £300 ($381) per user and additional penalties on non-compliant service providers.

- Revenue Projection: HMRC expects to capture £315 million ($392 million) in unpaid gains by April 2030, funding vital public services.

- Global Context: CARF aligns with the OECD’s AEOI standard and parallels the US’s upcoming Form 1099-DA reporting from January 2025, as well as India’s stringent 30% flat tax, 1% TDS and mandatory KYC rules.

Understanding CARF and Its Objectives

The Cryptoasset Reporting Framework (CARF) is an OECD-backed initiative designed to extend automatic exchange of financial information—similar to the Common Reporting Standard (CRS)—to cryptocurrency transactions. Adopted by the UK in its Autumn Budget 2024, CARF aims to close tax gaps by illuminating previously opaque trading activities, making it harder for individuals to shelter gains in decentralized assets and ensuring a level playing field across jurisdictions.

Key Requirements for Crypto Service Providers and Users

From January 1, 2026, Reporting Cryptoasset Service Providers (RCASPs)—including centralized exchanges, custodial wallets, NFT platforms, and hybrid DeFi services—must:

- Register with HMRC as an RCASP.

- Collect and verify user data: full name, date of birth, residential address, country of residence (for non-UK users), and taxpayer identification number.

- Report annual transaction summaries to HMRC by May 31, 2027, covering all trades, transfers, swaps, and token exchanges.

This mirrors the US shift toward IRS Form 1099-DA, which from January 2025 will require brokers to report gross proceeds—and from 2026 onward cost basis and gains—for every digital asset sale.

Penalties and Enforcement Mechanisms

Non-compliance is costly: individual traders who withhold required information face fines of up to £300 ($381) per offense, while platforms risk additional sanctions, including higher daily penalties until compliance is achieved. James Murray, Exchequer Secretary to the Treasury, emphasized these rules will “close the tax gap” and ensure revenue for crucial services like healthcare and policing.

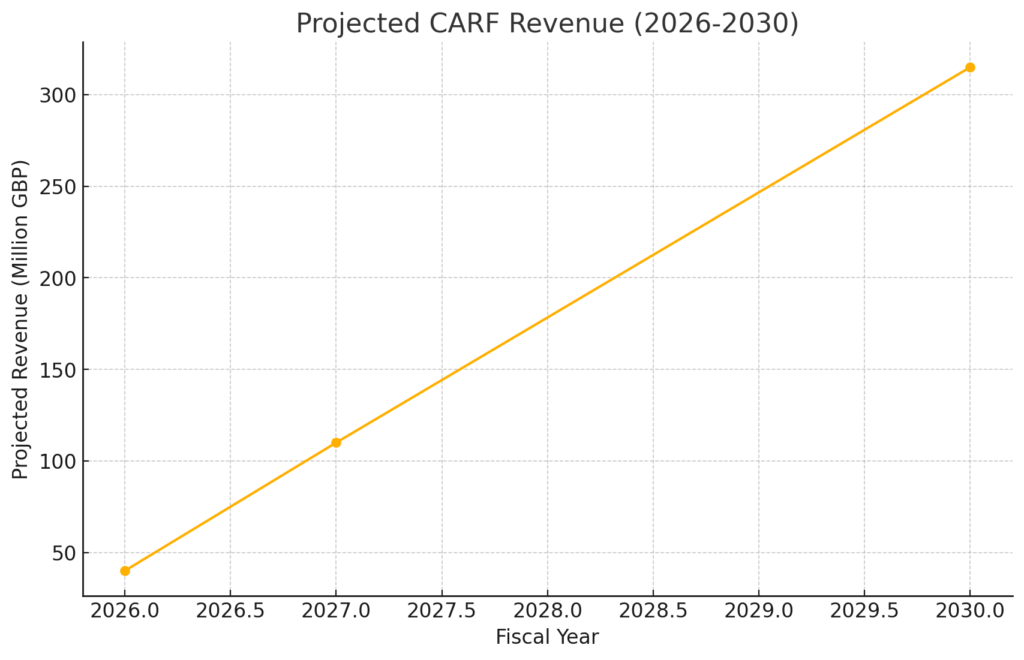

Figure 1: Projected CARF Revenue (2026–2030)

Source: HMRC impact assessment, projections by Law360 and Ainvest

(Chart generated above)

Revenue Projections and Funding Public Services

The government estimates:

- £40 million in revenue for FY 2026–27

- £110 million for FY 2027–28

- Scaling to £315 million by April 2030

This influx will bolster NHS funding, law enforcement, and other public services, effectively redirecting funds that previously escaped tax scrutiny.

Global Adoption and Comparable Measures in the US and India

- United States: The IRS launches Form 1099-DA on January 1, 2025, obligating brokers to report digital asset proceeds and, eventually, cost-basis data. This mirrors CARF’s objectives and hints at future US participation in cross-border data exchange.

- India: Under Finance Act 2022, India applies a flat 30% tax on crypto gains and 1% TDS on sales above ₹10,000, alongside strict KYC under the Prevention of Money Laundering Act. Major exchanges must register with the FIU-IND and enforce user due diligence.

Opportunities for Investors and Service Providers

These compliance regimes generate new markets for:

- KYC/AML Solutions: Automated identity verification and transaction monitoring.

- Tax Reporting Tools: Platforms that aggregate on-chain data and generate jurisdiction-compatible reports.

- Privacy-Focused Coins & Protocols: Projects emphasizing on-chain privacy may see increased demand.

- Blockchain Analytics Firms: Services offering enriched on-chain analytics to spot irregularities and optimize tax positions.

By proactively integrating compliance modules and developing user-friendly tax-reporting APIs, startups and service providers can capture a share of this evolving ecosystem.

Conclusion

The UK’s CARF marks a pivotal shift: the era of anonymous crypto trading is ending, replaced by robust tax transparency. While this tightens compliance burdens, it also opens avenues for innovative compliance technologies, advanced analytics, and privacy-enhanced solutions. For investors, understanding these regulations is essential to spot undervalued assets and emerging compliance service providers. As global regimes converge—UK’s CARF, US Form 1099-DA, and India’s flat-tax model—the next wave of blockchain applications will emphasize trust, transparency, and pragmatic utility over unchecked anonymity.