Main Points:

- UAE’s Ministry of Finance has joined the CARF multilateral agreement and plans to implement it starting 2027, with first automatic exchanges in 2028

- CARF (Crypto-Asset Reporting Framework) is the OECD’s standardized framework for automatic exchange of tax-relevant crypto transaction data among jurisdictions

- The UAE is conducting public consultations between Sept–Nov 2025 to refine domestic rules and align with industry input

- The UAE’s crypto market has seen strong inflows (e.g. ≈ USD 34 billion over 2023–2024) and regulatory reforms to balance growth and integrity

- Implementation of CARF globally will push crypto service providers (exchanges, wallets, brokers) into more stringent KYC, data collection, reporting, and compliance operations

- The shift toward transparency may also challenge privacy, competitive positioning for smaller players, and operational burden — yet opens a path for institutional adoption and legitimacy

- For new crypto projects, understanding compliance costs, jurisdictional risks, and designing with transparency in mind will be essential going forward

1. UAE’s Decision to Embrace CARF: Timeline & Strategy

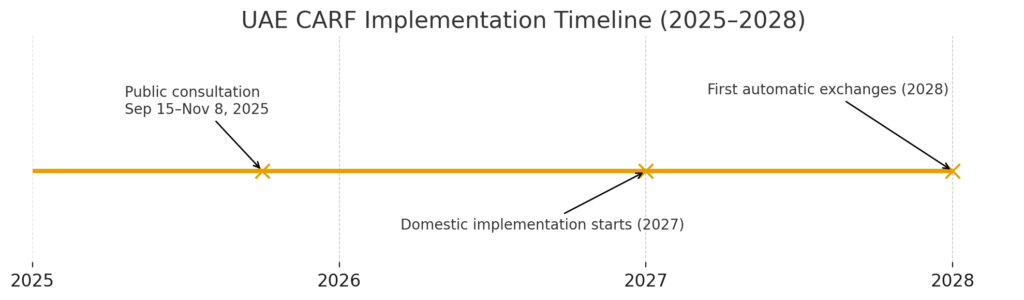

In September 2025, the UAE’s Ministry of Finance declared that the country would adopt the Crypto-Asset Reporting Framework (CARF), joining approximately 50 (or more) jurisdictions in agreeing to an international crypto tax data exchange regime. Under this plan, the UAE will begin domestic implementation in 2027, with the first automatic exchanges of tax-related digital asset data expected in 2028.

To prepare the ground, the ministry has opened public consultation from September 15 to November 8, 2025, inviting feedback from exchanges, custodians, financial institutions, traders, wallet providers, and advisory firms. This consultative process is meant to tailor the UAE’s domestic rules in a way that balances global obligations, local market realities, and industry competitiveness.

Strategically, UAE envisions CARF adoption as consistent with its broader ambition to be a leading regulated crypto hub: fostering investor confidence, lowering regulatory ambiguity, and positioning the nation as a mature jurisdiction for institutional flows.

2. What Is CARF (Crypto-Asset Reporting Framework)?

2.1 Origins & Relationship to CRS

CARF is a product of the OECD’s effort to extend the regime of automatic information exchange (AEOI) into the realm of crypto and digital assets. It complements the Common Reporting Standard (CRS), which was designed to exchange information about financial accounts. In effect, while CRS governs traditional financial accounts, CARF is its crypto counterpart—targeting transactions in crypto-assets that may fall outside traditional financial institutions.

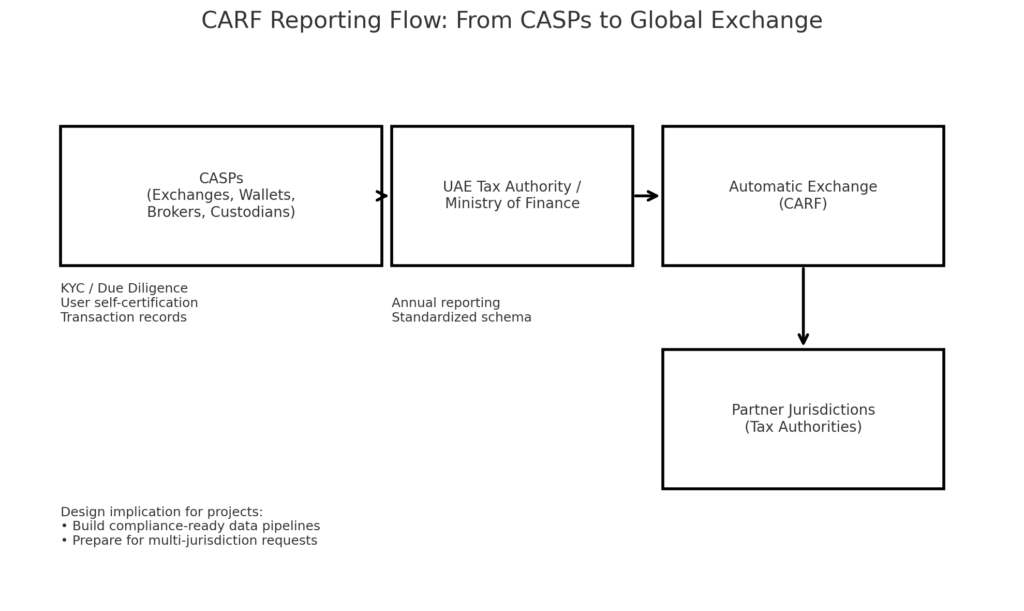

Under CARF, Crypto Asset Service Providers (CASPs)—such as exchanges, brokers, custodians, wallet providers, and platforms facilitating crypto trades—will be required to conduct due diligence on users, collect detailed information about user tax residency and identity, track users’ transaction histories (e.g. buys, sells, transfers), and report that to domestic tax authorities. That information is then exchanged automatically across relevant jurisdictions under multilateral or bilateral agreements.

The OECD’s 2024 update on CARF indicates that over 58 Global Forum member jurisdictions have already committed to exchanging CARF data starting 2027.

2.2 Key Components & Nexus Rules

CARF’s framework includes:

- Scope of Crypto-Assets: The design covers not only major cryptocurrencies (Bitcoin, Ethereum) but potentially also other tokens, NFTs (if used for investment or trading), derivatives, and other instruments tied to crypto value.

- Reporting Entities (CASPs): Entities that provide services enabling buying, selling, exchange, custody, or platform facilitation are generally in scope.

- Due Diligence & User Identification: CASPs must collect self-certification forms (or equivalent) to establish user tax residency, verify identities, and categorize users (individuals vs corporate).

- Transaction Reporting: For reportable users, detailed transactions—like transfers, swaps, sales, exchanges—must be captured and submitted.

- Exchange & Electronic Format: Reporting authorities will exchange in a standardized XML schema format under multilateral competent authority agreements (MCAAs).

A key novelty is the nexus rules: CARF determines which jurisdiction(s) a CASP must report to, based on a hierarchy including: tax residence of the entity or user, location of incorporation, place of management, or principal place of business.

In sum, CARF represents a globally coordinated push to extend tax oversight into crypto, making previously opaque or cross-jurisdictional transactions more transparent.

3. UAE’s Crypto Landscape: Growth, Risks & Incentives

3.1 Capital Inflows & Market Growth

Recent reports suggest the UAE has attracted approximately USD 34 billion (2023–2024) in crypto inflows as part of its push to become a digital finance center. Other sources report that over the past year, the UAE received about USD 34 billion in crypto investment—a reflection of a 42% year-over-year increase in inflows.

One driver is the UAE’s historically light or absent capital gains tax regime for individuals, which made it relatively attractive as a tax-friendly jurisdiction for crypto investors. Coupled with a growing ecosystem of licensed exchanges and custodians, the UAE has built a reputation as a competitive crypto hub.

3.2 Regulatory Coordination & Agency Alignment

In mid-2025, the UAE’s Securities & Commodities Authority (SCA) and Dubai’s Virtual Assets Regulatory Authority (VARA) established a strategic partnership aimed at consolidating oversight, harmonizing licensing, and enhancing investor protection across jurisdictions. Traditional banks are also making inroads: for example, Emirates NBD has partnered to enable crypto trading through its “Liv” digital banking app.

Part of the regulatory push aligns with anti-money laundering (AML) and counter-terrorist financing (CTF) goals. The UAE is reportedly tightening laws to curb illicit flows, freeze assets, and increase transparency of virtual-asset transfers.

3.3 Risks & Tensions

While the inflows and regulatory momentum are promising, the introduction of CARF also introduces adjustment risks:

- Operational burden: Smaller exchanges, wallet providers, or DeFi platforms may struggle with the compliance cost of KYC infrastructure, data storage, and reporting systems.

- Privacy concerns: Users accustomed to anonymous or pseudonymous transactions may push back or seek jurisdictions with laxer rules.

- Competitive pressure: Regions that delay or resist CARF might temporarily attract “regime arbitrage,” though that may risk reputational isolation.

- Enforcement challenges: Ensuring accurate user self-certification, cross-jurisdictional audits, and preventing misreporting will stress regulatory capacity.

Nevertheless, over time, markets may bifurcate: those who comply (capturing institutional capital, credibility, cross-border flows) vs those operating in gray zones.

4. Global Trends: CARF & Crypto Tax Transparency

4.1 Growing Global Adoption

CARF’s adoption is accelerating worldwide. As of mid-2025, more than 58 jurisdictions have pledged to begin exchanges in 2027. Switzerland is advancing legislation to exchange crypto tax data with 74 partner countries. South Korea has finalized its CARF agreement in September 2025. Meanwhile, in the EU, the DAC8 (an implementation of CARF principles under the EU’s administrative cooperation rules) is to come into effect by January 2026.

4.2 Impacts on Providers & Users

- Crypto service providers must significantly upgrade their compliance, data pipelines, KYC/AML modules, and reporting systems.

- Institutions previously hesitant to engage in crypto may find more comfort in a regulated environment, leading to institutional coin flows, tokenization, and DeFi adoption under regulated rails.

- Some users, especially those in high-tax jurisdictions, may see increased tax scrutiny, less anonymity, but potentially more legitimacy in markets.

- Smaller or purely decentralized (non-custodial) protocols may be less directly impacted—but any interconnected front-end services (exchanges, bridges) may be pulled into compliance nets.

4.3 Strategic Themes & Opportunity Spaces

- Compliance-as-a-service: Building middleware or compliance tooling to help CASPs (especially startups) comply with CARF could be an emerging niche.

- Privacy layers / zero-knowledge reporting: Techniques that cryptographically prove compliance without revealing full transaction graphs may gain traction.

- Cross-chain / cross-jurisdiction coordination: Projects that integrate cross-chain data and tax-aware routing may become more valuable.

- Institutional-grade infrastructure: Custody, auditing, on-chain proof services, regulatory oracles, and compliance SDKs may see greater demand.

5. Implications & Recommendations for Crypto Innovators

Given this regulatory shift, what should those exploring new tokens, business models, or blockchain implementations keep in mind?

5.1 Design for Transparency & Compliance

From the outset, projects should assume that transactions will be subject to reporting obligations. Incorporate design patterns that allow auditors or compliance modules to verify legitimate flows without undermining user confidentiality (e.g. zero-knowledge proofs, cryptographic audit logs).

5.2 Choose Jurisdictions Carefully

While jurisdictions like UAE are becoming more regulation-forward, others may lag. But jurisdictional arbitrage (i.e. choosing lax jurisdictions) may carry reputational, banking, or partner risk. Being in a forward-looking but compliant jurisdiction may become a competitive advantage.

5.3 Build Modular Compliance Stacks

Rather than reinventing reporting engines, aim to build modular, API-based compliance stacks that can plug into exchanges, wallets, or custodial layers. This is especially valuable for new entrants or service providers that must adapt to evolving regimes.

5.4 Foster Regulatory Dialogue

Follow trends in public consultations (like UAE’s current one) and engage regulators early. That helps shape favorable rules, ensures smoother implementation, and builds trust.

5.5 Target Institutional Use Cases

The increased legitimacy and compliance regime will likely tilt capital toward infrastructure assets, tokenization platforms, real-world asset bridging, regulated DeFi, and institutional custody. Focus development on use cases with strong regulatory alignment.

6. Conclusion: The Coming Era of Regulated Crypto Growth

The UAE’s adoption of CARF marks a pivotal turning point in the crypto-asset regulatory landscape. Rather than resisting transparency, the UAE is doubling down on marrying regulatory rigor with a pro-growth stance. By 2027, its crypto space will be governed by a globally consistent tax reporting regime—with 2028 as the first full year of cross-border data exchange.

While the shift imposes operational burdens and raises privacy tensions, it also offers a pathway: markets built on trust, institutional capital inflows, and interoperable regulatory frameworks. For crypto innovators, the time to plan for compliance is now—not as a constraint, but as a foundation. Projects that internalize transparency will likely outcompete those that treat regulation as a threat.