Key Points :

- The 2025 GENIUS Act establishes the first federal stablecoin regulatory framework, enabling U.S. banks to issue payment stablecoins with clarity and oversight.

- Major banks such as JPMorgan Chase and Bank of America are gearing up to launch proprietary stablecoin offerings, leveraging new law and seeking competitive positioning.

- Stablecoin issuance promises high-yield, low-risk returns by deploying reserves into U.S. Treasuries, inspired by Tether’s remarkable 2024 net profit.

- GENIUS Act includes unprecedented consumer protections, like 1:1 asset backing, priority for holders in bankruptcy, and strict AML measures.

- Policy and financial trends suggest growing demand for U.S. Treasuries through stablecoin issuance, potentially reshaping debt markets and liquidity dynamics.

1. GENIUS Act: A Landmark Regulatory Framework

In July 2025, the U.S. Congress passed the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act), which was swiftly signed into law by President Trump on July 18. This legislation marks the first comprehensive federal framework for “payment stablecoins,” providing legal clarity and encouraging mainstream adoption.

Under GENIUS, only “permitted payment stablecoin issuers”—subsidiaries of insured banks or credit unions, federally approved non-bank firms, or state-authorized entities—can issue stablecoins in the U.S. These issuers must back each coin one-to-one with high-quality assets such as U.S. dollars, short-term Treasuries, or equivalent instruments, and publish monthly reserve disclosures audited by independent accountants.

Critically, the law:

- Enforces compliance with the Bank Secrecy Act (AML/KYC standards).

- Grants stablecoin holders super-priority in bankruptcy, shielding their claim to reserves and limiting issuer recourse.

- Prohibits foreign stablecoin issuers from offering products in the U.S. unless regulated under a comparable oversight regime and registered with the OCC.

- Exempts payment stablecoins from being classified as securities under SEC or commodities under CFTC, delegating authority to banking regulators.

- Allows tokenized deposits by banks to continue outside of the GENIUS regime, preserving innovation flexibility.

- Creates a public comment process for assessing cybersecurity, privacy, and illicit finance risks.

The GENIUS Act is expected to take effect either 120 days after final regulation or 18 months post-enactment—whichever comes first.

2. Major Banks Mobilize: JPMorgan, BofA, and Beyond

Following the law’s passage, leading U.S. banks have begun planning stablecoin entries:

- JPMorgan Chase: CEO Jamie Dimon, previously skeptical of crypto, embraced the idea, calling himself “a believer in stablecoins and blockchain.” JPMorgan is advancing its institutional-focused “JPM Coin” (processing ~$2 billion daily), has filed the trademark “JPMD,” and formed partnerships to strengthen its offering.

- Bank of America: CEO Brian Moynihan emphasized the importance of regulatory clarity and announced plans for a cautious, phased stablecoin rollout integrated with existing banking infrastructure.

- Additional major firms—including Wells Fargo, Citi, and others—are reportedly considering joint stablecoin issuance via Early Warning Services (EWS), the operator behind Zelle, enabling shared risk, lower costs, and inter-bank interoperability.

This movement marks a historic pivot in traditional banking strategy, with banks aiming to harness blockchain-backed digital assets to maintain relevance in evolving payment ecosystems.

3. Attractiveness of the Stablecoin Business Model

The financial appeal of stablecoin issuance is undeniable:

- Tether’s 2024 performance: With a reported net profit of $13 billion, largely from interest on about $113 billion in U.S. Treasuries, Tether exemplified the income potential of this model.

- A simplified yield structure—issuers collect U.S. dollar deposits (“1 coin = $1”), deploy them into ~4–5% yielding Treasuries, and retain the interest—yields high margins with relatively low risk.

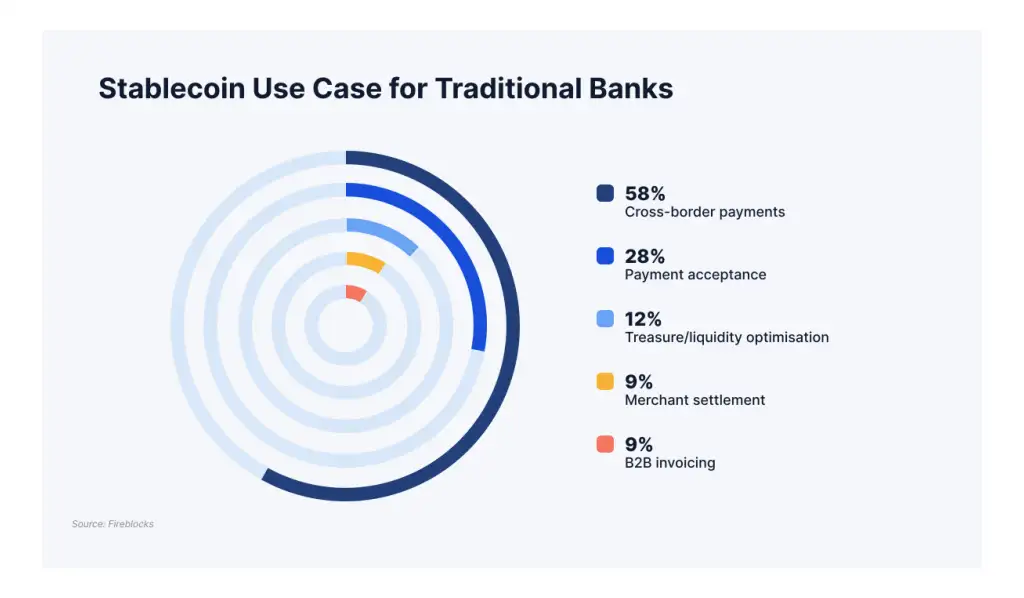

- According to a 2025 Fireblocks survey, 49% of institutions, including Tier-1 banks, already use stablecoins for payments, attracted by faster settlements (48%), transparency (36%), integrated payment flows, and improved liquidity—not just cost savings.

Insert Image Here (after above section):

Caption: Institutional motivations for stablecoin adoption—speed, transparency, liquidity, and more (source: Fireblocks “State of Stablecoins 2025” survey).

4. Macro Effects – Treasury Demand & Financial Implications

The GENIUS Act may have far-reaching macroeconomic consequences:

- U.S. Treasury Secretary Scott Bessent has begun dialogues with major stablecoin issuers, positioning them as strategic buyers of Treasury bills amid rising federal debt issuance.

- Analysts project stablecoin holdings could swell to $2 trillion, potentially injecting significant demand pressure into short-term Treasury markets.

- The act’s requirement of 1:1 backing and reserve transparency may drive Treasury demand but also poses concerns over the displacement of credit creation within the banking sector—critics liken stablecoins to a modern form of 19th-century private money, with liquidity but not credit expansion.

- Fed Governor Michelle Bowman urged regulators to abandon an “overly cautious mindset” and integrate crypto innovations proactively to sustain financial system relevance.

5. Consumer and Risk Considerations

Despite promises, the stablecoin transition raises concerns:

- Consumer groups caution there remain redemption complexities, hidden fees, and a lack of FDIC protections, distinguishing stablecoins from insured bank deposits.

- Legal changes in bankruptcy laws may unpredictably affect issuers: while holders are protected, issuers may face immediate insolvency risks due to inability to use reserve assets to fund legal proceedings.

- Critics also warn of regulatory capture, suggesting the legislation may disproportionately benefit big tech or banks and insufficiently shield consumers.

6. Emerging Trends & Broader Implications

A new academic white paper describes this shift as “Banking 2.0”, positing stablecoins as a transformative force akin to artificial intelligence in finance—uniting crypto innovation with traditional systems to resolve systemic inefficiencies.

As implementation progresses over the next 12–18 months, wide adoption by retailers, remitters, B2B payers, and government disbursements seems increasingly likely. However, balancing innovation with consumer safety and systemic stability will be essential.

Conclusion

The GENIUS Act represents a bold turning point in digital finance, opening the floodgates for regulated stablecoin issuance by U.S. banks under unprecedented legal and operational clarity. With major institutions mobilizing to monetize stablecoin revenue models, we may witness a new era of “Banking 2.0,” where fast, transparent, asset-backed digital payments become integral—not peripheral—to modern financial infrastructure.

Key watch-points for our reader community—those seeking new crypto opportunities, revenue sources, or real-world blockchain applications—include:

- Which banks or consortia will be first to launch law-compliant stablecoins?

- How this will affect yield dynamics in Treasuries and cross-border payments?

- What consumer protections or platforms will emerge to bridge stablecoins and everyday users?

This is fertile ground for innovation—and profit—for those ready to engage strategically.