Main Takeaways :

- The CEOs of Bank of America, Citigroup, and Wells Fargo are meeting U.S. senators to influence the final shape of a bipartisan crypto market-structure bill (CLARITY Act) and its interaction with the GENIUS stablecoin law.

- U.S. banks are pushing hard to ban or strictly limit interest-paying stablecoins, arguing they could drain deposits and raise borrowing costs in the real economy.

- The GENIUS Act of 2025 already became the first federal digital-asset law, setting strict 1:1 reserve rules for payment stablecoins and prohibiting issuers from paying yield.

- A separate market-structure bill (CLARITY Act), which passed the House and is now in the Senate, will decide what counts as a “commodity” vs. a “security” token and which regulator—CFTC or SEC—gets oversight.

- A new political reality: pro-crypto super PACs have amassed about $263,000,000 to influence Congress ahead of the 2026 midterms, making digital-asset policy one of Washington’s most heavily funded issues.

- For builders and traders, the outcome will shape whether stablecoins stay “boring dollars on-chain” or evolve into regulated yield products, and which tokens can legally be listed on U.S. exchanges.

1. What Is Happening This Week in Washington?

According to Bloomberg and other outlets, the CEOs of Bank of America (Brian Moynihan), Citigroup (Jane Fraser), and Wells Fargo (Charlie Scharf) are scheduled to meet key U.S. senators in a closed-door session to discuss the crypto market-structure bill, sometimes referred to in Washington as the CLARITY Act or “digital asset market clarity” bill.

The meeting is organized by the Financial Services Forum, an alliance representing large U.S. banks. The agenda focuses on three core issues that matter directly to your portfolio and products:

- Interest on stablecoins – whether exchanges, fintechs, and DeFi protocols should be allowed to pay yield directly on tokenized dollars.

- Banks’ competitive position – whether the rules will let non-banks issue and distribute digital dollars at scale while banks remain constrained.

- Illegal-finance risk – how to ensure stablecoins and other tokens are not used for sanctions evasion, terrorism financing, or large-scale money laundering.

Behind this one meeting is a broader shift: for the first time, the U.S. already has a federal stablecoin law (GENIUS Act), and is now trying to build a full market-structure framework on top of it.

2. The GENIUS Act: Stablecoins Become “Regulated Dollars on Chain”

2.1 What the Law Does

The GENIUS Act of 2025—short for Guiding and Establishing National Innovation for U.S. Stablecoins—is now the backbone of U.S. stablecoin policy. It:

- Creates a federal licensing regime for payment stablecoin issuers, splitting oversight between bank regulators and the OCC for non-bank issuers.

- Requires 1:1 reserves in cash and short-dated U.S. Treasuries or insured bank deposits.

- Mandates segregated reserve accounts, AML/BSA compliance, and regular attestations and audits.

- Critically, bans stablecoin issuers themselves from paying interest or yield to holders, shutting the door on “bank account-like” products that directly compete with deposits.

In plain English: if you are Circle-like or Tether-like and want to operate legally in the U.S., your token must function like pure tokenized cash, not like a savings product.

2.2 The Loophole: Exchanges and DeFi

However, as the BIS and several compliance analysts note, this ban applies to issuers, not necessarily to third parties. That means exchanges, broker-dealers, DeFi protocols, and even banks could, in theory, wrap or rehypothecate stablecoins and offer yield on top.

The result has been the rapid growth of “yield-bearing stablecoins” and wrapper products, with the BIS estimating more than $19,000,000,000 worth of such tokens by September 2025.

Banks see this as a direct threat: every dollar moving from a demand deposit into a yield-bearing stablecoin is a dollar they cannot use to fund loans. The Banking Policy Institute has warned that allowing stablecoin yield at scale would raise borrowing costs and reduce credit availability to households and businesses.

3. The CLARITY Market-Structure Bill: Who Regulates What?

3.1 From House Victory to Senate Negotiations

On the market-structure side, Congress is working on the CLARITY Act, which passed the House earlier and is now the focus of intense debate in the Senate. The bill attempts to answer two critical questions:

- When is a token a “digital commodity” (CFTC) vs. a “digital security” (SEC)?

- Which platforms can legally list and intermediate those tokens?

The Senate Banking Committee and the Senate Agriculture Committee (which oversees the CFTC) are working on parallel drafts that must be reconciled. One approach focuses on whether an asset can be transferred without an intermediary, another on whether the token is intrinsically linked to a blockchain in a way that makes it commodity-like.

3.2 Why Bank CEOs Care About Market Structure

For large banks, the market-structure bill is not just about investor protection—it is about who gets to intermediate digital assets at scale:

- If more tokens end up classified as “digital commodities”, that opens paths for CFTC-regulated futures and spot markets, where banks are already active.

- If they are classified as “securities”, Wall Street can leverage its existing broker-dealer, ATS, and custody infrastructure, but the SEC will control product design and disclosures.

Banks want to avoid a world where crypto-native exchanges and wallet providers dominate token markets while they are limited to narrow roles, especially if those non-banks can simultaneously offer attractive yield on stablecoins.

4. The Political Money Behind Crypto Policy

4.1 Crypto’s $263,000,000 War Chest

One reason this bill is moving at all: crypto has gone fully political.

Pro-crypto super PACs such as Fairshake and allied committees have built a combined war chest of roughly $263,000,000 for the 2026 midterm elections, according to Bloomberg reporting.

These funds are explicitly earmarked to support candidates seen as friendly to the digital-asset industry or to defeat those viewed as hostile—especially in swing districts or committee leadership races.

4.2 Banks vs. Crypto in the Lobbying Arena

Banks are countering with their own lobbying push. Groups like the Banking Policy Institute and Financial Services Forum are pushing Congress to:

- Close the interest loophole for stablecoins, so that not only issuers but also intermediaries effectively cannot offer on-chain dollar yield that competes with bank accounts.

- Ensure any market-structure framework does not privilege non-bank platforms at the expense of regulated banks.

- Maintain traditional safeguards against money laundering and sanctions evasion in DeFi and offshore stablecoins.

On the other side, crypto firms and exchanges are urging lawmakers to allow properly regulated stablecoin yield and keep room for DeFi and non-custodial models, arguing that prohibiting returns on tokenized dollars could push innovation offshore.

5. Why Stablecoin Yield Matters for Builders and Investors

5.1 From “Digital Cash” to “On-Chain Money Market”

If interest-bearing stablecoins or wrappers remain allowed under U.S. law, they can function like on-chain money market funds:

- Exchanges and DeFi protocols can pass on part of the yield from reserve Treasuries and repo to users.

- Treasury-backed tokens become a core building block for on-chain credit, structured products, and RWAs.

- For traders, yield-bearing stablecoins become the default “parked capital” asset between trades.

The BIS estimate of $19,000,000,000 in yield-bearing stablecoins is already material, but still small compared with the roughly $250,000,000,000+ global stablecoin market.

If the U.S. explicitly allows these products, that market could grow by an order of magnitude, especially if tokenized U.S. Treasuries continue to gain traction.

5.2 If Banks Get Their Way

If, however, the Senate and House ultimately agree to ban interest payments on stablecoins at the intermediary level, at least for U.S. residents, then:

- Pure payment stablecoins (no yield) will dominate the regulated U.S. market.

- Yield products will likely move to offshore venues or non-U.S. user segments, increasing jurisdictional fragmentation.

- Banks retain the privileged position as providers of deposit accounts and money-market access, while still potentially issuing their own tokenized dollars for payments and settlement.

For you as a builder, this would push innovation toward payment rails, settlement, and tokenized bank money, rather than consumer yield products.

6. Practical Implications for Traders, Builders, and New Projects

6.1 For Traders and Yield Seekers

- Expect greater clarity on which stablecoins are “safe” and U.S.-compliant under the GENIUS framework. Names that secure federal licenses and publish detailed reserve attestations will likely trade at a premium.

- Watch the interest debate closely. If Congress allows yield-bearing wrappers, you may see tiered dollar products: basic non-yield stablecoins and institutional-grade yield tokens.

- Political risk becomes a market risk: changes driven by elections or enforcement priorities can directly affect stablecoin yields, listings, and access.

6.2 For Startup Founders and Protocol Designers

If your target audience is users looking for new revenue sources and practical blockchain use, the key opportunity zones are:

- Tokenized real-world assets (RWA)

- Tokenized T-bills, credit, and receivables structured on top of compliant stablecoins.

- B2B products for SMEs seeking access to dollar yields via regulated wrappers.

- Compliance-aware DeFi

- Protocols that integrate KYC, sanctions screening, and travel-rule features while maintaining non-custodial design.

- White-listed pools restricted to known wallets, suitable for banks and registered brokers.

- Bank–Crypto Integration Layers

- Middleware that connects core banking systems with GENIUS-compliant stablecoins and CLARITY-defined tokens—FX, cross-border settlement, and instant treasury flows.

- Tools that let banks treat stablecoin rails as simply another payments network, with automated reporting and risk limits.

- On-chain political and compliance analytics

- With hundreds of millions of dollars flowing into political advocacy around crypto, there will be demand for transparent dashboards tracking lobbying, votes, and regulatory risk linked to token exposures.

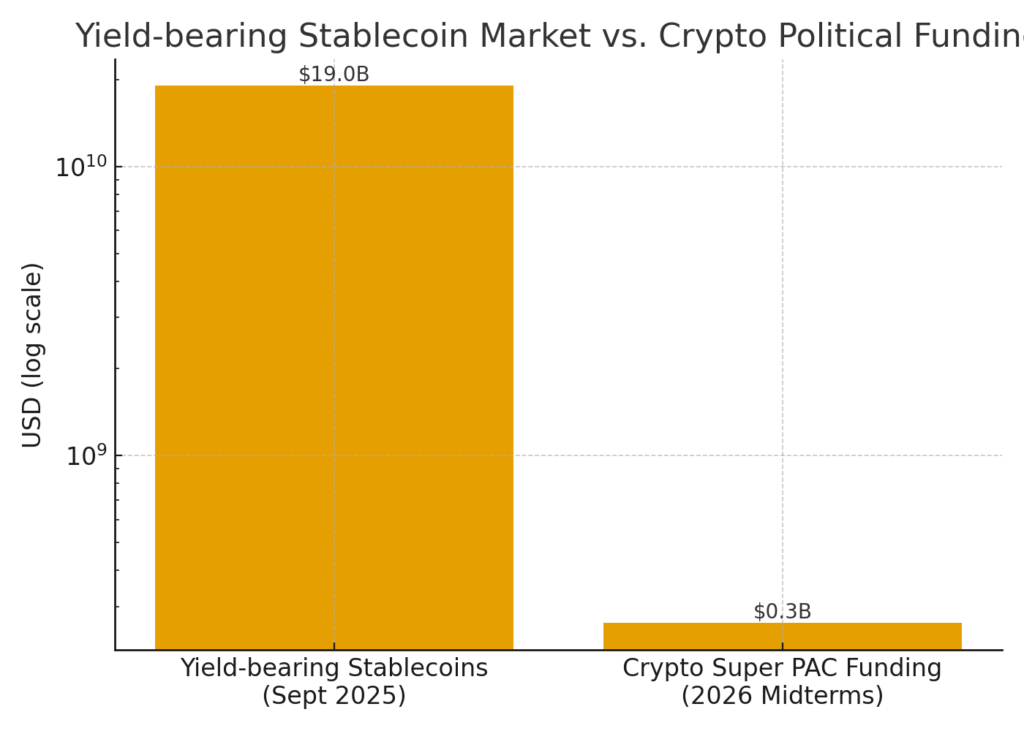

7. Visual Snapshot: Size vs. Politics

This chart compares:

- The approximate $19,000,000,000 market for yield-bearing stablecoins (as of September 2025).

- The roughly $263,000,000 war chest accumulated by crypto-focused super PACs for upcoming U.S. elections.

The scale difference is huge, but the political money is still large enough to reshape legislation that governs those billions in tokens—and potentially trillions in future tokenized assets.

8. How This Fits into the Global Stablecoin Landscape

The U.S. is not acting in a vacuum. The EU’s MiCA, the UK’s evolving rules, and regimes in Hong Kong, Singapore, and the UAE are all converging on a model where:

- Payment stablecoins must be fully reserved, transparent, and tightly supervised.

- Interest-bearing products are treated more like securities or money-market funds, with additional licensing and disclosure requirements.

GENIUS plus the CLARITY bill would place the U.S. firmly in this trend, but with a uniquely American twist: a fierce political battle over who controls the new rails for “dollar on chain” and who captures the yield.

For builders targeting cross-border flows or multi-jurisdiction platforms, aligning your design with the strictest common denominator—full reserves, clear segregation, audited disclosures, and conservative yield mechanics—will likely pay off.

9. Conclusion: Positioning for the Next Phase of Tokenized Finance

The scheduled meeting between U.S. bank CEOs and senators is more than just another D.C. photo-op. It signals that:

- Stablecoins are no longer a niche crypto toy; they are now central to debates over deposit funding, credit creation, and dollar dominance.

- The GENIUS Act has already locked in a baseline of “dollars on chain with no issuer yield”, while the CLARITY market-structure bill will decide how far tokenization can go into commodities, securities, and DeFi.

- Interest on stablecoins is the key battleground: whether the U.S. allows regulated yield products or forces them offshore will shape where capital, developers, and users concentrate over the next cycle.

For your audience—people hunting for new crypto assets, fresh income streams, and real-world blockchain applications—the message is clear:

- Watch which stablecoin and RWA projects position themselves as GENIUS-compliant, CLARITY-aligned, and politically savvy. Those are likely to become the “core infrastructure” of the next wave.

- Expect more convergence between banks and crypto, not less. Whether they like it or not, large banks are negotiating how to enter this space, not how to avoid it.

- The biggest opportunities will sit at the intersection of regulation and innovation: protocols and platforms that embrace the new rules while still delivering better UX, faster settlement, and new forms of programmable yield—within whatever limits Congress ultimately draws.

If you build or invest with this regulatory trajectory in mind, you are not just betting on the next token; you are positioning yourself for the long game of tokenized dollars and on-chain capital markets.