Main Points:

- President Trump to sign an executive order directing regulators to investigate alleged de-banking of crypto firms and conservatives

- Regulators to examine potential violations of the Equal Credit Opportunity Act, antitrust, and consumer protection laws

- Directive includes scrapping policies contributing to customer exclusions and mandating SBA loan‐practice reviews

- The move follows industry allegations of “Operation Choke Point 2.0” and a February 2025 Senate hearing on de-banking

- Federal banking agencies have recently removed “reputational risk” from examinations, aligning with the order’s intent

Executive Order Targets De-Banking Allegations

President Donald Trump is reportedly preparing to sign a presidential executive order within days that would direct banking regulators—namely the Federal Reserve Board (FRB), the Office of the Comptroller of the Currency (OCC), and the Federal Deposit Insurance Corporation (FDIC)—to investigate whether financial institutions have engaged in “de-banking”—the practice of closing or refusing services to clients—for political or crypto-related reasons. According to a draft obtained by The Wall Street Journal, regulators would look into possible breaches of the Equal Credit Opportunity Act, antitrust statutes, and consumer financial protection laws. Financial institutions found in violation could face monetary penalties, consent decrees, or other disciplinary actions. Trump may sign the order as early as this week, though details could still change before its final issuance.

Scope of the Investigation and Legal Framework

Under the proposed order, regulators would be instructed to probe whether banks have violated three core areas of U.S. law:

- Equal Credit Opportunity Act (ECOA): Prohibits discrimination in lending decisions.

- Antitrust Laws: Ensures that banks do not engage in exclusionary or monopolistic practices.

- Consumer Financial Protection Laws: Enforced by the Consumer Financial Protection Bureau (CFPB), covering unfair or deceptive practices.

This broad mandate empowers regulators to investigate any bank policy that may have led to the abrupt termination or refusal of services for certain political or digital-asset clients. Should violations be confirmed, the order authorizes civil fines, suspension of regulatory approvals, or legal actions in court.

Mandate to Review Internal Policies and SBA Practices

Beyond investigations, the draft order directs regulators to identify and eliminate internal policies or guidance that could have prompted banks to exclude specific customers—particularly crypto firms and conservative groups. It also instructs the U.S. Small Business Administration (SBA) to review the banking practices tied to its loan guarantees for small businesses. In effect, the SBA would reassess how banks administer loans backed by the agency, ensuring they do not use ideological or risk-averse rationales to deny credit to eligible borrowers.

Background: Industry Claims and Operation Choke Point 2.0

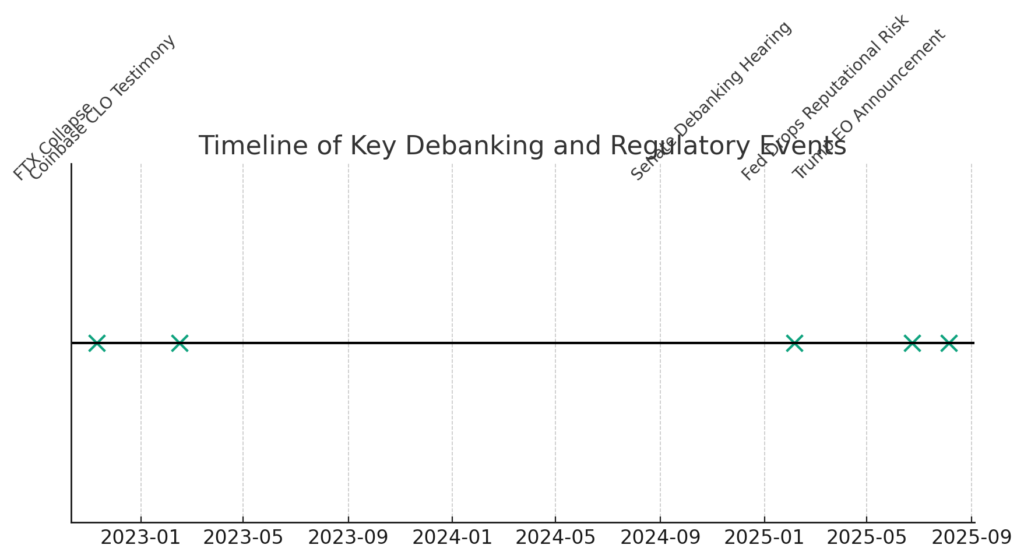

Crypto executives have long alleged that regulators under the prior administration unofficially pressured banks to sever ties with digital-asset firms after the FTX collapse in November 2022. Coinbase’s Chief Legal Officer, Paul Grewal, testified in February 2024 that the FDIC had “bludgeoned banks” with inquiries about crypto and stablecoins until they “relented under pressure.” A Freedom of Information Act (FOIA) lawsuit later revealed FDIC letters requesting banks suspend crypto services, fueling claims that these actions were more than coincidental. Venture investor Nick Carter dubbed this alleged conspiracy “Operation Choke Point 2.0,” referencing a 2010s Justice Department program that targeted lawful yet controversial industries through banking scrutiny.

Senate Scrutiny and Crypto Executives’ Testimonies

Concerns over de-banking entered the halls of Congress on February 5, 2025, when the Senate Banking Committee held a hearing titled “Investigating the Real Impacts of Debanking in America.” Witnesses included Nathan McCauley, co-founder and CEO of Anchorage Digital, who testified that his firm sought banking services at roughly 40 banks only to be rebuffed under “no-crypto” policies. Senator Tim Scott (R-SC) spearheaded the inquiry, accusing the Biden administration of abusing regulatory power to exclude crypto and conservative clients. Ranking Member Elizabeth Warren (D-MA) countered that banks themselves, not regulators, often opt to delist risky customers, citing overdrafts or compliance concerns.

Regulatory Shift: Dropping Reputational Risk from Bank Exams

In parallel, federal banking regulators have moved to eliminate “reputational risk”—a once-subjective examination criterion—from their supervisory materials. On June 23, 2025, the Federal Reserve Board announced it would remove all references to reputational risk and replace them with concrete measures of credit, market, and operational risk. The OCC and FDIC have undertaken similar actions since March 2025, with each agency committing to expunge reputational-risk language from handbooks and guidance. These shifts aim to prevent banks from citing vague “reputation” concerns when deciding to close or refuse accounts, a practice critics say facilitated de-banking of lawful industries and political viewpoints.

Reactions from Banks and Lawmakers

Major banks have swiftly denied any politically motivated de-banking. Spokespersons for JPMorgan Chase and Bank of America maintain that their decisions are driven solely by risk management and regulatory compliance. In interviews, Trump cited his personal disputes with banks—including claims that JPMorgan gave him 20 days to close his account—but neither bank corroborated a politically motivated action. Meanwhile, some lawmakers, including Senate Banking Chair Tim Scott, have expressed strong support for Trump’s order, viewing it as necessary to safeguard free-market access for all Americans. Critics caution that the executive order could politicize bank supervision further, potentially hampering legitimate risk assessments.

Implications for Crypto Firms and Political Groups

If implemented, the executive order could reshape how banks interface with emerging industries. Crypto firms may find renewed confidence in accessing financial services, potentially unlocking new funding channels and operational stability. Conservative organizations that allege they were unfairly delisted may also see redress. However, banks could respond with tighter internal compliance frameworks or raise fees to offset perceived regulatory risks. Legal challenges are likely, especially if banks interpret the order as infringing on their statutory discretion to manage client risk profiles. Observers will closely watch how the DOJ and CFPB, once referrals are made, choose to pursue allegations of unlawful discrimination.

Timeline of Key Events

Below is a visual timeline of major milestones in the unfolding de-banking saga:

[Figure 1: Timeline of Key Debanking and Regulatory Events]

Conclusion

President Trump’s forthcoming executive order represents a critical juncture in the ongoing debate over banking access for crypto firms and politically aligned entities. By formally directing regulators to investigate potential legal violations and dismantle exclusionary policies, the order seeks to codify safeguards against ideologically driven de-banking. Coupled with the recent removal of reputational risk from examiner handbooks, these developments may recalibrate risk management practices across the banking sector. The ultimate impact will depend on how agencies enforce the new directives, how banks adjust compliance and credit decisions, and whether affected parties pursue legal or legislative remedies. For an industry that thrives on open financial rails, the outcome could determine the future landscape of blockchain adoption and ideological neutrality in U.S. banking.