Main Points:

- President Trump signs an executive order directing the Department of Labor to reevaluate restrictions on alternative assets—including digital assets, private equity, and real estate—in 401(k) plans

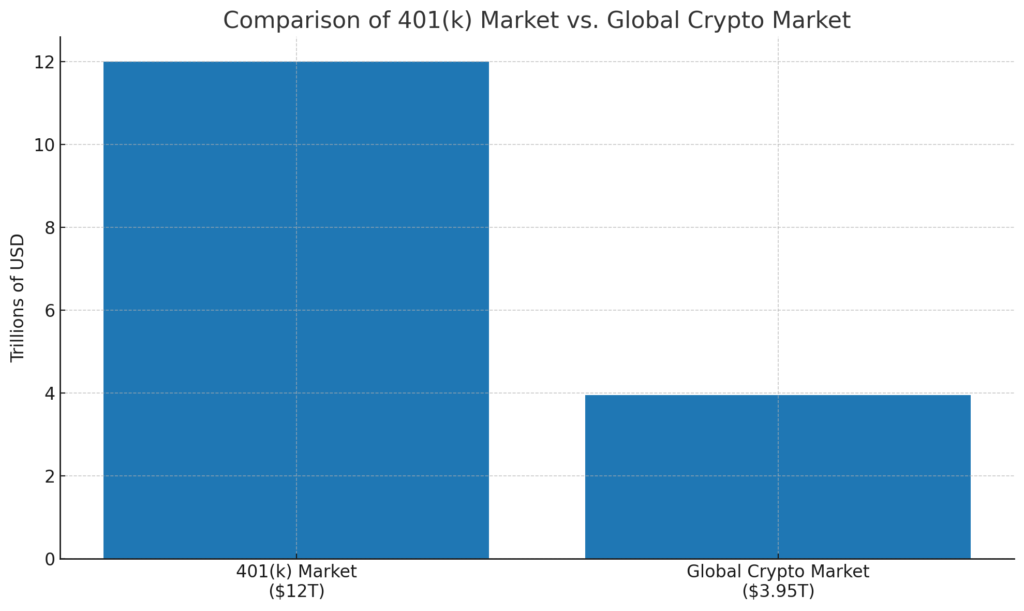

- The move potentially opens the $12 trillion defined contribution market to cryptocurrencies, a major opportunity for digital-asset firms

- Global cryptocurrency market cap stands at approximately $3.95 trillion, underscoring the scale of digital‐asset investment opportunities

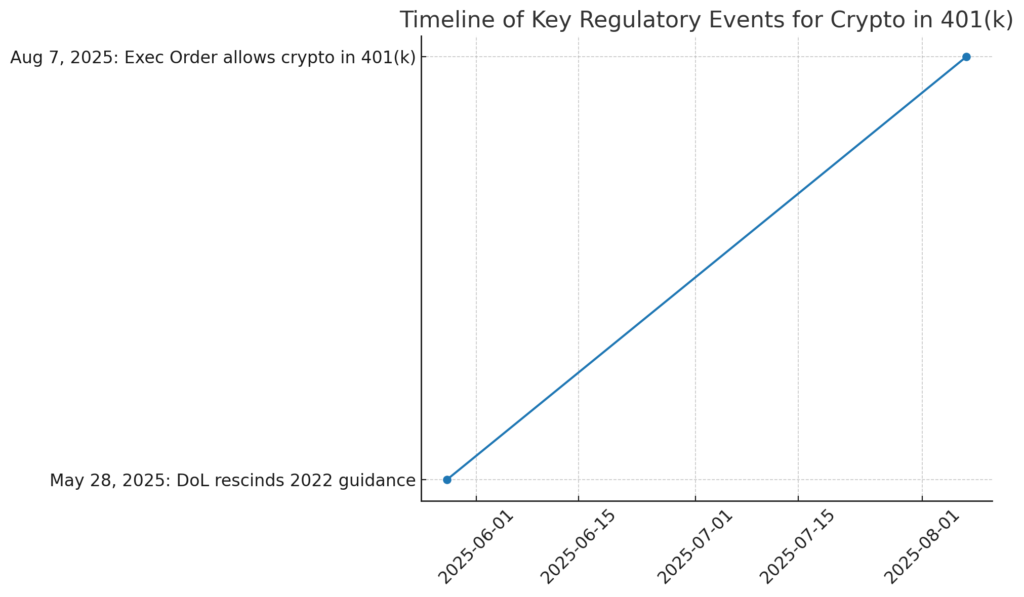

- The Department of Labor rescinded its cautious 2022 guidance on crypto in retirement accounts and will coordinate with the SEC and Treasury on new fiduciary rules

- Industry leaders like Fidelity have launched crypto ETPs for IRAs and retirement accounts, though widespread plan adoption may take up to 15 months

- Retail adoption remains moderate, with only 14 percent of U.S. adults owning cryptocurrency amid concerns about volatility and regulatory clarity

[Insert Figure 1: Comparison of 401(k) Market vs. Global Crypto Market]

Executive Order Details

On August 7, 2025, President Donald J. Trump signed an executive order instructing the U.S. Department of Labor (DoL) to revisit and clarify its stance on alternative assets in defined contribution retirement plans such as 401(k)s. According to a White House official, the order directs the Secretary of Labor to outline a clear fiduciary process and provide guidance on how plan fiduciaries can evaluate digital assets—like Bitcoin and Ethereum—alongside private equity and real estate. The directive also calls for interagency collaboration with the Treasury Department and the Securities and Exchange Commission (SEC) to consider necessary regulatory changes that would facilitate the inclusion of these assets in retirement products.

This effort follows media reports earlier in the summer, including coverage by the Financial Times, suggesting that the administration was weighing options to diversify retirement portfolios beyond traditional stocks and bonds. Although the executive order itself does not immediately expand investment options, it marks the first formal step toward integrating crypto into the retirement ecosystem, which has historically restricted plan offerings to mutual funds, exchange-traded funds, and other broadly diversified vehicles.

Market Impact and Reactions

Cryptocurrency markets reacted positively to the news. On the day of the signing, Bitcoin prices rose by nearly 2 percent, trading above $117,000, while Ethereum surged over 5 percent past $3,870. These moves reflect short-term optimism about the potential for a new influx of long-term capital into digital assets. More broadly, the global cryptocurrency market cap currently stands at around $3.95 trillion, highlighting the substantial scale of digital assets relative to U.S. retirement savings.

Analysts note that opening access to even a fraction of the $12 trillion defined contribution market could channel hundreds of billions of dollars into crypto, private equity, and real estate products over time. However, some market observers caution that actual inflows will depend on the development of suitable investment vehicles and the willingness of plan sponsors to embrace higher-risk assets.

Fiduciary Guidelines and Regulatory Context

In late May 2025, the DoL rescinded its 2022 guidance that urged plan fiduciaries to exercise “extreme caution” when considering cryptocurrency for retirement plans. That guidance had been a significant barrier for many plan sponsors, who cited concerns over price volatility, regulatory ambiguity, and potential litigation risks. The new executive order mandates the DoL to clarify its position and, in coordination with the SEC and Treasury, formulate updated rules to protect retirement savers while allowing for alternative-asset diversification.

SEC Chair Paul Atkins emphasized in a Bloomberg interview that investor education and transparent disclosures are critical if crypto is to become a viable retirement option. He noted that ensuring participants fully understand the risks and fees associated with digital assets will be key to maintaining the integrity of retirement portfolios.

[Insert Figure 2: Timeline of Key Regulatory Events for Crypto in 401(k)]

Industry and Custodian Preparedness

Major financial institutions are already preparing for the potential rollout of crypto-based retirement products. Fidelity, which manages over $5.9 trillion in assets, has introduced two spot cryptocurrency exchange-traded products (ETPs)—one tracking Bitcoin and another tracking Ethereum—which can be held in brokerage, trust, and IRA accounts. Similarly, other custodians such as Charles Schwab and BlackRock have publicly discussed developing crypto offerings, though most providers warn it will take up to 15 months to adapt plan documents, evaluate fee structures, and conduct fiduciary reviews before adding such options to standard 401(k) lineups.

Plan sponsors may initially offer cryptocurrency through self-directed brokerage windows or standalone private equity vehicles before fully integrating digital-asset ETPs into core plan menus. Over time, evolution in plan design might include target-date and target-risk funds with dedicated allocations for alternative assets.

Retail Adoption and Investor Sentiment

Despite growing institutional interest, retail adoption of cryptocurrency remains moderate. A recent Gallup poll found that 14 percent of U.S. adults currently own Bitcoin or other digital assets, with most nonowners citing perceived risk and regulatory uncertainty as deterrents. Younger demographics, particularly those aged 18–49, show higher ownership rates, but widespread acceptance will likely hinge on clearer regulatory frameworks and lower transaction costs.

Industry surveys indicate that approximately 20 percent of plan sponsors are open to considering crypto in their retirement lineups in the next two years, especially as peer institutions pilot small-scale offerings through self-directed windows. Educational initiatives by the DoL and SEC, along with improved disclosure standards, are expected to play a pivotal role in shifting sentiment and enabling broader participation.

Conclusion

President Trump’s executive order represents a watershed moment for retirement-plan diversification, potentially unlocking a new channel for digital assets and other alternative investments in the $12 trillion defined contribution market. While regulatory frameworks and fiduciary guidelines must be refined, leading custodians are already laying the groundwork for crypto-enabled retirement products. For investors seeking new sources of return and practical blockchain applications, the path to integrating crypto into long-term savings has never been clearer—though adoption timelines will depend on plan-sponsor readiness, regulatory coordination, and continued emphasis on investor education.